SEBI Buyback Reversal: New Rules for Capital Allocation

By Sivam

SEBI reintroduces open-market share buybacks from Aug 1, 2026. Learn about the new safeguards and structural shift in capital allocation.

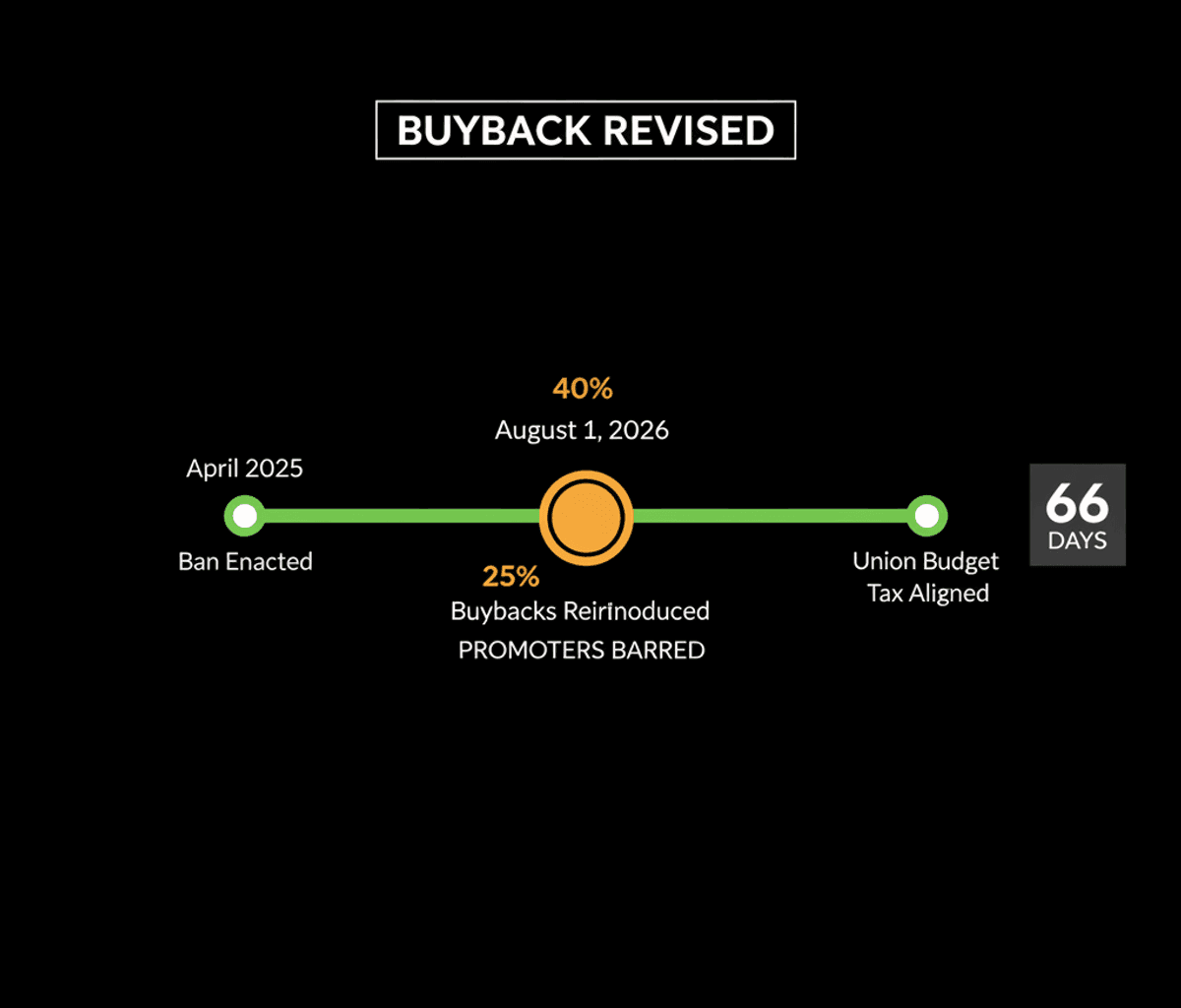

The Securities and Exchange Board of India (SEBI) is set to reintroduce open-market share buybacks through stock exchanges, effective August 1, 2026. This decision marks a significant structural recalibration in India’s capital markets, reversing a prohibition enacted in April 2025. The initial ban stemmed from critical concerns over tax distortions and institutional imbalances within the buyback mechanism. The present reintroduction is made possible by the recent Union Budget’s alignment of buyback taxation with capital gains, thereby neutralizing the primary fiscal rationale for the previous ban.

A share buyback, or stock repurchase, fundamentally involves a company acquiring its own outstanding shares from the open market, consequently reducing the total number of shares in circulation. Companies typically engage in buybacks to signal perceived undervaluation, enhance key financial ratios such as Earnings Per Share (EPS) and Return on Equity (RoE), and optimize their capital structure. Historically, buybacks also served as a tax-efficient mechanism for returning capital to shareholders compared to dividends, a factor that previously distorted market behavior.

The prohibition enacted in April 2025 was a direct result of recommendations from the Keki Mistry-led Primary Market Advisory Committee (PMAC) and SEBI’s own internal assessments. This ban specifically addressed structural loopholes, investor inequality, and tax arbitrage. Key issues included the anonymity inherent in open-market buybacks, which often facilitated front-running by institutional brokers or insiders. Furthermore, it tackled situations where high-net-worth individuals and promoters could withdraw substantial sums tax-free, circumventing higher dividend tax rates.

The Revised Regulatory Architecture

The new framework, slated for implementation on August 1, 2026, introduces several stringent safeguards designed to prevent the abuses observed previously. The entire buyback operation must now be completed within a maximum of 66 working days. Companies are mandated to deploy at least 40% of the earmarked funds during the first half of this buyback period, ensuring committed capital usage rather than speculative announcements. A crucial change is the explicit bar on promoters and their associates from participating in the buyback, with their existing shareholdings locked in for the duration of the buyback period.

Additional provisions ensure that the buyback adheres to the statutory minimum 25% public shareholding requirement. The process also streamlines compliance by making the appointment of a merchant banker optional, which can reduce overheads for companies. These rules collectively aim to enhance transparency and level the playing field, mitigating the institutional imbalances that plagued the previous open-market buyback mechanism and fostering a more equitable market environment.

For corporations, this revised framework offers renewed capital allocation flexibility and potentially lower compliance costs, alongside the capacity for market stabilization during volatile periods. However, the strict 40% fund deployment mandate introduces a degree of inflexibility, potentially limiting tactical responses. Promoters also face operational restraints due to the lock-in of their shares during the 66-day window, a clear trade-off for broader market integrity.

Shareholders, conversely, stand to gain immediate liquidity and price support in the secondary market, as the company acts as a consistent buyer. The structural shift ensures that the benefits of buybacks are more equitably distributed, rather than concentrated among a few sophisticated players exploiting informational asymmetries. This regulatory evolution underscores a commitment to fostering a more transparent and fair market environment, addressing past concerns about investor inequality.

This reintroduction of open-market buybacks by SEBI is more than a mere policy reversal; it represents a refined understanding of capital market dynamics and regulatory efficacy. By addressing the core structural issues of tax distortion and unequal access that led to the previous ban, SEBI is attempting to create a mechanism that supports corporate capital management while upholding investor protection. The success of this updated framework will hinge on its ability to withstand real-world market pressures, offering a valuable case study in adaptive financial regulation.