India’s Affordable Housing Finance Boom: Vridhi’s Success

By Sivam

Discover how Vridhi Home Finance’s success highlights the booming affordable housing finance sector in underserved India, driven by demand in smaller towns and innovative lending.

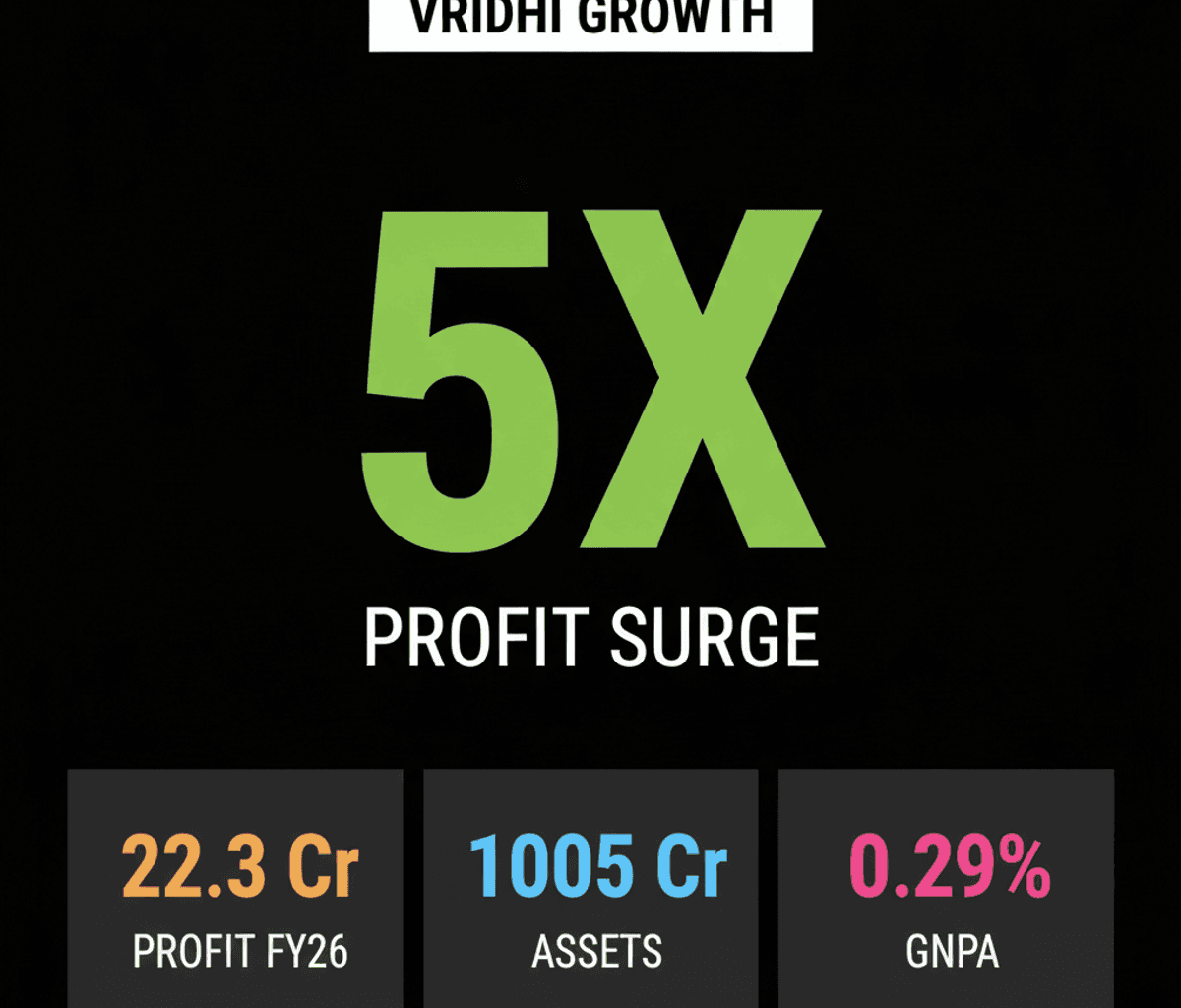

The robust financial performance of non-banking financial companies (NBFCs) focused on affordable housing finance, as exemplified by Vridhi Home Finance, underscores a powerful structural trend within India’s credit landscape. This Bengaluru-based lender recently reported a nearly five-fold surge in net profit to ₹22.3 crore in FY26, a significant increase from ₹4.6 crore in the preceding fiscal year, driven by strategic focus on underserved markets.

This growth is not an isolated incident but a direct consequence of a fundamental market mechanism: the persistent demand for credit in India’s smaller towns and among underserved borrowers. These segments, often overlooked by larger financial institutions, represent a vast and largely untapped market for specialized lenders. Vridhi Home Finance, founded in 2022, has strategically positioned itself to address this gap, offering home loans ranging from ₹3 lakh to ₹45 lakh.

The company’s operational strength directly reflects this market capture, with total income more than doubling to ₹103.4 crore in FY26 from ₹47.9 crore in FY25. Total managed assets expanded by 65% year-on-year, reaching ₹1,005.3 crore, primarily fueled by the expansion of its housing loan and loans against property portfolios. Such growth metrics illustrate the scalability inherent in addressing a well-defined, under-penetrated market segment.

A critical aspect of this model is maintaining asset quality, even while serving riskier profiles. Vridhi Home Finance reported gross non-performing assets (GNPA) at approximately 0.29% and net non-performing assets (NNPA) at 0.22% as of March 2026. This indicates effective underwriting and risk management strategies, which are paramount for NBFCs operating in this space. The return on managed assets improved from 1.1% to 2.8% over the year, signaling enhanced operational efficiency and profitability.

This sector’s appeal extends beyond individual company performance, resonating with a broader investment thesis in India’s lending technology market. The projected $1.3 trillion opportunity by 2030 in Indian lending tech, driven by advancements in digital underwriting and the escalating credit demand from underserved segments, provides a macro-framework for understanding these micro-level successes. Vridhi Home Finance has successfully capitalized on this, raising over ₹515 crore since its inception, including a ₹310 crore Series B funding round in 2024 led by Norwest Venture Partners, which bolstered its net worth to ₹533.9 crore as of March 2026.

The expansion of Vridhi’s physical footprint, now operating 92 branches across six states with plans for continued asset growth exceeding 60% annually, further illustrates the hybrid approach often required in these markets. While digital underwriting plays a crucial role in efficiency and outreach, a physical presence often remains vital for trust-building and last-mile service delivery in smaller towns.

Ultimately, the trajectory of entities like Vridhi Home Finance serves as a case study for the structural advantages enjoyed by agile NBFCs targeting specific, underserved credit markets. Their ability to deliver strong financial results while maintaining asset quality highlights the enduring viability of a model centered on deep market understanding and tailored product offerings. This pattern suggests that the growth narrative for specialized lenders in India’s evolving financial landscape remains robust, driven by fundamental shifts in credit access and demand.