Celltrion’s Q2 Blowout Fuels Investor Confidence & Bullish Forecasts

By ThePip Desk

Celltrion reported record Q2 2026 revenue and operating profit, exceeding market expectations for the second straight quarter, sparking strong analyst endorsements and increased foreign investment in its stock.

🔥 Main Takeaway

Celltrion’s Q2 2026 financial results significantly outperformed market expectations for the second consecutive quarter, demonstrating robust growth in its core biosimilar business. This strong performance has solidified investor confidence, leading to bullish outlooks from major securities firms and increased foreign investment.

📌 What Happened?

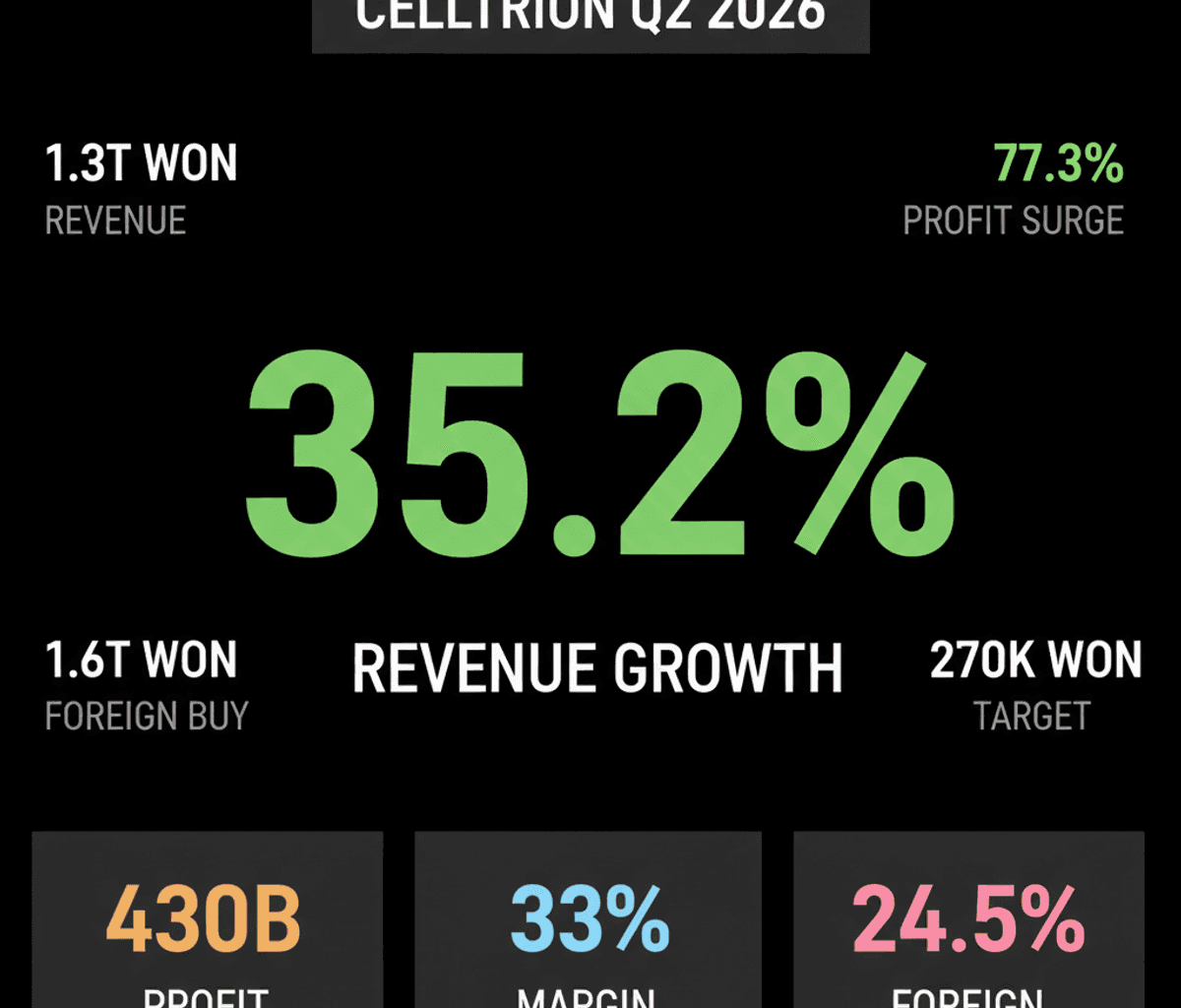

The company reported preliminary consolidated revenue of 1.3 trillion won ($940 million) for Q2 2026, alongside an operating profit of 430 billion won. These figures surpassed analyst estimates, marking a substantial 35.2% year-on-year increase in revenue and a 77.3% surge in operating profit.

This period represents Celltrion’s highest-ever second-quarter revenue and operating profit, with its operating margin improving from 25% to 33%. Growth was primarily driven by strong sales of key biosimilars such as Remsima SC, Yuflyma, and Steqeyma globally.

Newly launched products, including Avtozma, Stoboclo, and Osenvelt, also began contributing to revenue during the quarter. This diversified product portfolio is now expected to provide additional growth momentum for the second half of the year.

💰 Why It Matters

Celltrion’s consistent earnings beat across two quarters signals strong operational execution and a validating trend for its growth strategy. This performance is likely to expand investor interest in the broader healthcare sector, positioning Celltrion as a leading beneficiary.

Foreign ownership in Celltrion rose by 3.4 percentage points during the first half of the year, reaching 24.5% of total shares. This translates to foreign investors purchasing approximately 1.6 trillion won worth of the company’s stock, underscoring international confidence.

Major securities firms like Nomura and Daiwa have issued positive assessments and buy ratings for Celltrion. Nomura maintained its 270,000 won target price and named Celltrion its top pick in Korea’s healthcare sector, forecasting significant annual revenue and operating profit increases.

The company’s established direct sales platforms in Europe and the U.S. are crucial assets, enabling it to effectively capitalize on the expanding global biosimilar and contract development and manufacturing markets. This structural advantage enhances its competitive edge and future growth prospects.

👀 What to Watch Next

Investors should closely monitor Celltrion’s accelerated development in novel drugs, particularly its innovative pipeline in antibody-drug conjugates (ADCs) and multispecific antibodies. This strategic shift could unlock new value and diversify its revenue streams beyond biosimilars.

Initial clinical results for ADC candidates CT-P70 and CT-P71 are highly anticipated, as they will provide tangible evidence of pipeline progress. Furthermore, the U.S. FDA has cleared CT-P72/ABP-102, a next-generation multispecific antibody candidate, to begin Phase 1 clinical trials.

Celltrion plans to apply for FDA Fast Track designation for CT-P72/ABP-102 within the year. This designation could significantly streamline the development and approval process, potentially bringing this promising novel drug to market faster.