India: Undeclared Cash, Gold & Investments Face Up to 78% Tax

By Sivam

Discover India’s strict income tax rules. Undeclared cash, gold, and investments can attract penalties up to 78%. Learn how to avoid hefty taxes and penalties.

Understanding the Tax Implications of Undeclared Assets

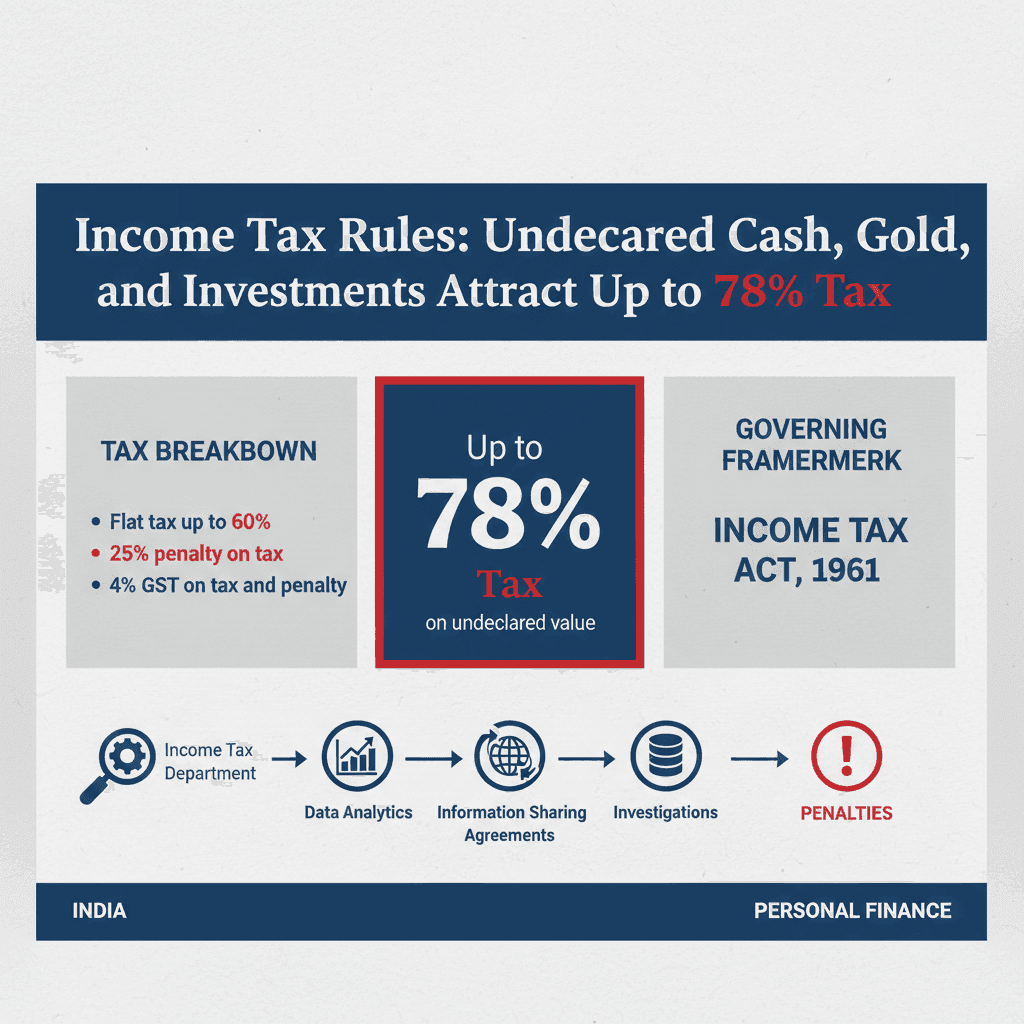

In India, while there is no legal restriction on the amount of cash an individual can possess at home, the crucial aspect lies in being able to explain its origin through legitimate and documented means. The Income Tax Department has stringent rules in place to deal with undisclosed income and assets, including cash, gold, and investments. Failure to provide a satisfactory explanation for the source of these assets can lead to significant tax liabilities, potentially reaching up to 78% of the undeclared value.

Penalties and Tax Rates for Undisclosed Income

The Income Tax Act, 1961, provides a framework for taxation of undisclosed income. When the Income Tax Department discovers unaccounted assets during an assessment, it levies taxes and penalties. The highest tax bracket for undisclosed income can reach 60% as a flat tax. In addition to this, a penalty of 25% of the tax amount is imposed, along with a 4% Goods and Services Tax (GST) on the total tax and penalty. This cumulative burden can effectively push the total tax and penalty to approximately 78% of the declared undeclared income. This aggressive taxation strategy is designed to deter tax evasion and encourage voluntary disclosure of income.

The Importance of Declaring All Assets

Possessing undeclared cash, gold, or investments, even if acquired through legal means, poses a risk if the source cannot be adequately substantiated. For instance, if an individual receives a significant amount of cash as a gift or loan, it is essential to have proper documentation, such as gift deeds or loan agreements, to prove its legality. Similarly, if gold or other investments were purchased with cash, the transaction details, including receipts and proof of payment, must be retained. Without such evidence, the Income Tax Department may treat these assets as undisclosed income, subjecting them to the high tax and penalty rates.

Navigating Income Tax Scrutiny

The Income Tax Department employs various methods to detect undisclosed assets, including information sharing agreements, data analytics, and surveys. It is therefore imperative for taxpayers to maintain accurate records of all their financial transactions and assets. This includes keeping a clear trail of income earned, investments made, and significant expenditures. In cases where substantial cash or assets are found without a clear source, individuals are advised to consult with tax professionals. A tax expert can guide on the best course of action, which might include making a voluntary disclosure to mitigate potential penalties, or preparing a robust defense with existing documentation.

Voluntary Disclosure and Compliance

The Indian tax system encourages voluntary compliance. While the penalties for non-disclosure are severe, the tax authorities also provide avenues for taxpayers to regularize their financial affairs. Understanding the nuances of income tax laws and proactively disclosing all income and assets is the most prudent approach to avoid severe financial repercussions. The threat of a 78% tax rate underscores the importance of transparency and meticulous record-keeping in managing personal finances and investments in India.