Vedanta Demerger: Unlocking Value & Sectoral Focus

By ThePip Desk

Vedanta Group’s strategic demerger into five entities aims to unlock shareholder value through specialized business focus and fairer valuations. Explore the impact.

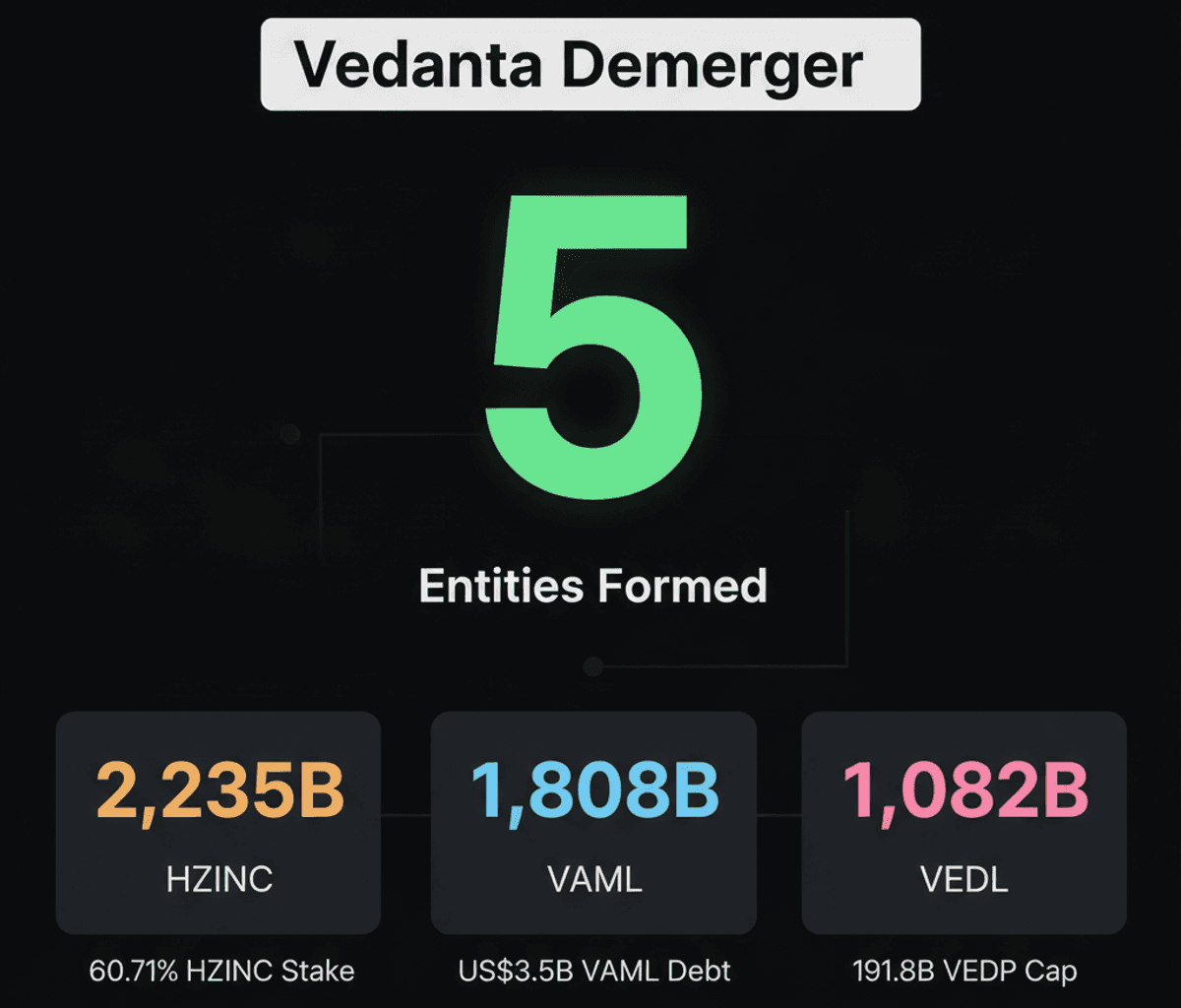

Anil Agarwal’s Vedanta Group has initiated a significant strategic demerger, splitting its diverse operations into five distinct entities. This structural reorganization aims to unlock greater shareholder value by allowing each specialized business to attract a more focused investor base, thereby potentially achieving fairer valuations than previously possible under a single conglomerate structure. The move underscores a fundamental principle in capital markets: clarity of business operations often leads to more efficient capital allocation and clearer investment theses.

The rationale behind such demergers is rooted in the concept of pure-play valuation. By segmenting operations like zinc, aluminium, power, and other minerals into independent units, the market can assess each business on its specific merits, growth prospects, and risk profile, rather than applying a conglomerate discount. This strategy intends to provide a clearer pathway for investors to engage with specific industrial segments.

Among these newly independent companies, Hindustan Zinc stands out with a robust market capitalization of Rs 2,235 billion. It maintains its position as the world’s largest integrated zinc-lead-silver producer, a status unaffected by the demerger. Vedanta Limited retains a 60.71% stake in this entity. For the year ending March 2026, Hindustan Zinc reported a 20% increase in revenue to Rs 408 billion and a 34% rise in net profit to Rs 138 billion, significantly benefiting from prevailing silver prices. Its substantial ore reserves, projected to last over 25 years, highlight its long-term operational stability within the group’s portfolio.

Next in line is Vedanta Aluminium Metal Limited (VAML), boasting a market capitalization of Rs 1,808 billion. VAML is a dominant player in India’s aluminium sector, contributing nearly half of the nation’s total output. It operates the world’s largest single-location smelter in Jharsuguda, Odisha, alongside Bharat Aluminium Company (BALCO) in Chhattisgarh, achieving a combined capacity of 2.88 million tonnes by March 2026. The company has ambitious plans to double this capacity to 6 million tonnes annually and is recognized for its top-quartile position on the global cost curve. However, a notable structural challenge for VAML is its significant net debt, estimated at approximately US$3.5 billion at the time of its listing, which will be a key financial metric to monitor.

The residual entity, Vedanta Limited, now holds a market capitalization of Rs 1,082 billion. This entity focuses on core operations including zinc, silver, copper, and essential minerals, primarily through its majority holding in Hindustan Zinc. It has divested its aluminium, power, oil and gas, and iron and steel businesses to the newly formed entities. Historically, the combined group recorded a strong performance for the year ending March 2026, with revenue up 15% to Rs 1,741 billion and net profit increasing 22% to Rs 251 billion. The independent financial trajectory of this streamlined Vedanta entity will be closely watched in subsequent quarters.

Finally, Vedanta Power Ltd, with a market capitalization around Rs 191.8 billion, represents the group’s thermal power division. Formerly known as Talwandi Sabo Power Limited, it operates the 1,980 MW Talwandi Sabo plant in Punjab, contributing to the group’s total power capacity of nearly 5 GW. While India’s increasing power demand, driven by industrial growth and data centers, presents a favorable market, the company contends with persistent challenges related to timely collections from state utilities. This issue is a common structural impediment across the Indian thermal power sector, impacting cash flows and operational efficiency.

The demerger strategy, while promising enhanced clarity and potentially higher valuations for distinct business units, also introduces a period of adjustment for each entity to establish its independent operational and financial track record. Investors will be evaluating how these specialized companies navigate their respective sectoral dynamics, particularly concerning capital structure, operational efficiency, and the resolution of industry-specific challenges like debt servicing for VAML or collection delays for Vedanta Power. This structural shift highlights a broader trend among diversified conglomerates to unbundle assets for optimized shareholder returns.