Upstart’s UMI Reporting Change: Impact on Default Risk & Investors

By ThePip Desk

Upstart refines UMI reporting, revealing a 2% rise in default risk. Learn how this impacts loan pricing and investor sentiment in the AI lending market.

Upstart just revamped its UMI reporting, and the latest data reveals a 2% spike in macroeconomic default risk since early June, a key signal for how the AI lending market is shaping up for investors.

📌 What Happened?

Upstart Holdings Inc. (NASDAQ: UPST), known for its AI lending marketplace, has officially announced changes to how it names and publishes its Upstart Macro Index (UMI).

The goal is crystal clear: enhance transparency. The UMI will now be identified by its specific publication date and will no longer receive weekly updates, ensuring that each reading represents a fixed, current snapshot of risk.

This new system directly links the data’s recency to Upstart’s underwriting decisions, providing a clearer picture of when the associated risk level truly impacts their loan approvals and pricing.

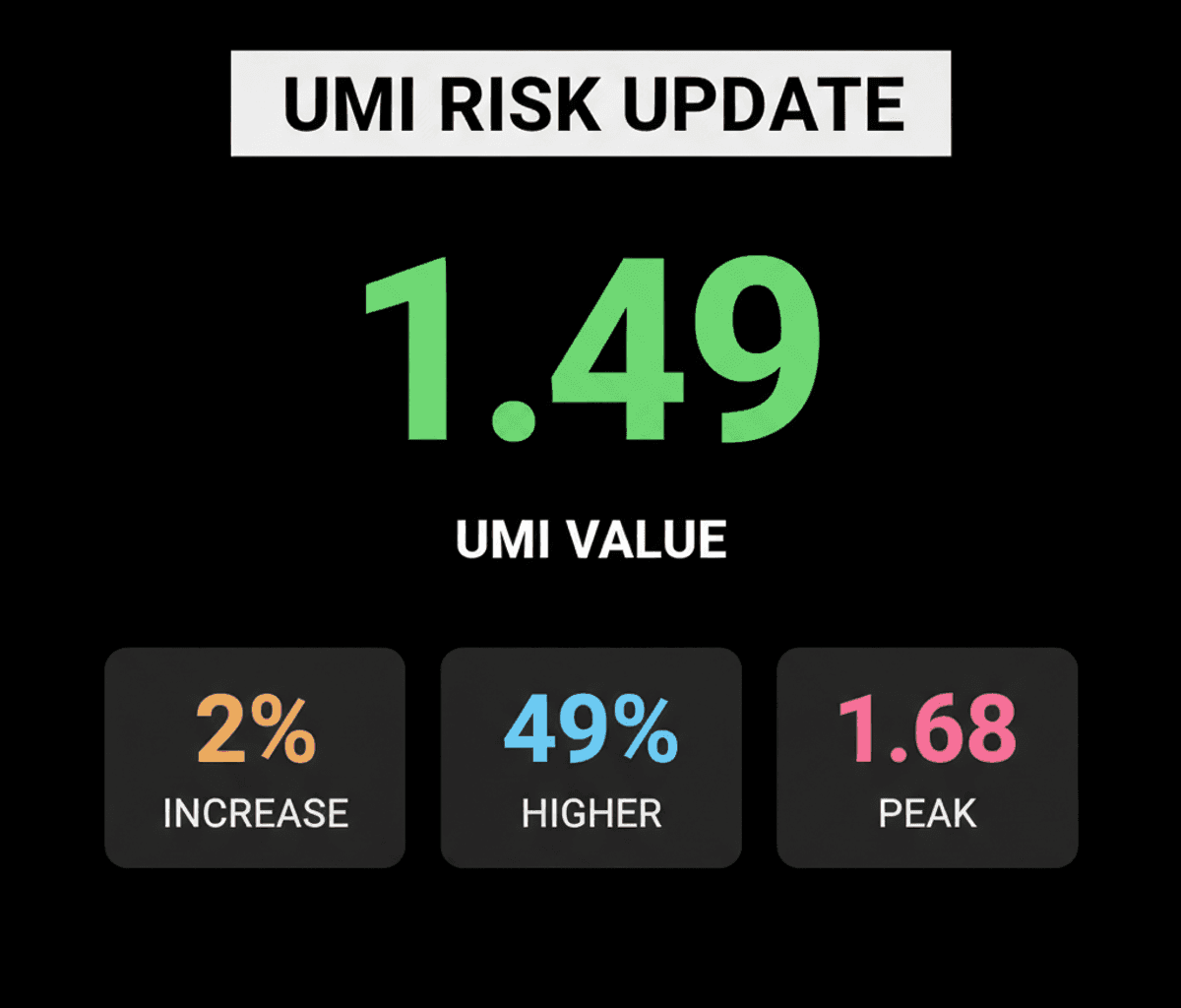

The most recent UMI, published on July 8, 2026, stands at 1.49, based on payment data collected up to July 2, 2026. This figure marks a 2% increase in macroeconomic default risk compared to what was observed in early June.

To put that in perspective, a UMI of 1.49 is approximately 49% higher than the expected baseline of 1.0 for a truly normal economic environment, indicating continued elevated risk.

💰 Why It Matters

For investors, this shift means more consistent and reliable data points for assessing the macroeconomic factors Upstart integrates into its AI-driven lending models, even though the core calculation method remains unchanged.

The UMI has consistently stayed above 1.0 since February 2022, signaling a persistent environment of heightened default risk, which directly influences Upstart’s loan pricing and the performance of existing loan portfolios.

While the current 1.49 reading shows an uptick from early June, it’s crucial to note it remains below its January 2024 peak of 1.68, suggesting that while risk is high, it hasn’t reached its recent historical maximum.

This elevated risk environment impacts both new loan pricing and the overall health of Upstart’s loan book, making UMI movements a critical metric for anyone tracking the company’s financial stability and growth prospects.

👀 What to Watch Next

Mark your calendars: Paul Gu, Upstart’s Co-Founder and CEO, is set to host a live Q&A session on X (formerly Twitter) on July 9. This is a prime opportunity to get direct insights into these UMI changes and their broader implications.

Future UMI publications, now fixed by their release date, will offer clearer, static snapshots of risk assumptions, providing a more stable and transparent metric for investors to gauge the economic headwinds facing Upstart’s business.

Keep a close watch on how these updated risk indicators are reflected in Upstart’s upcoming earnings reports, specifically in their loan origination volumes, approval rates, and delinquency trends, as they will directly show the real-world impact of these macro signals.