Turtlemint Fintech: Digital Dreams vs. Market Reality

By ThePip Desk

Turtlemint Fintech shows weak financial metrics and market performance despite its digital insurance focus. A cautionary tale for young investors in the fintech space.

🔥 Main Takeaway

Turtlemint Fintech Solutions Ltd, a player in the booming digital insurance sector, is currently showing weak financial metrics and unimpressive market performance. This raises significant red flags for young investors looking for growth opportunities in the fintech space.

📌 What Happened?

The company’s stock is trading at INR 138.62, experiencing a minor 0.43% decrease. Turtlemint Fintech operates within the NSE-Insurance-Brokers sector, offering digital insurance, investment, mutual fund, loan, and embedded insurance solutions.

MarketSmith India’s evaluation assigned an ‘N/A’ Master Score, indicating it failed to meet their criteria for a ‘B’ or better rating. This proprietary score combines EPS, Price Strength, Buyer Demand, and Group Rank.

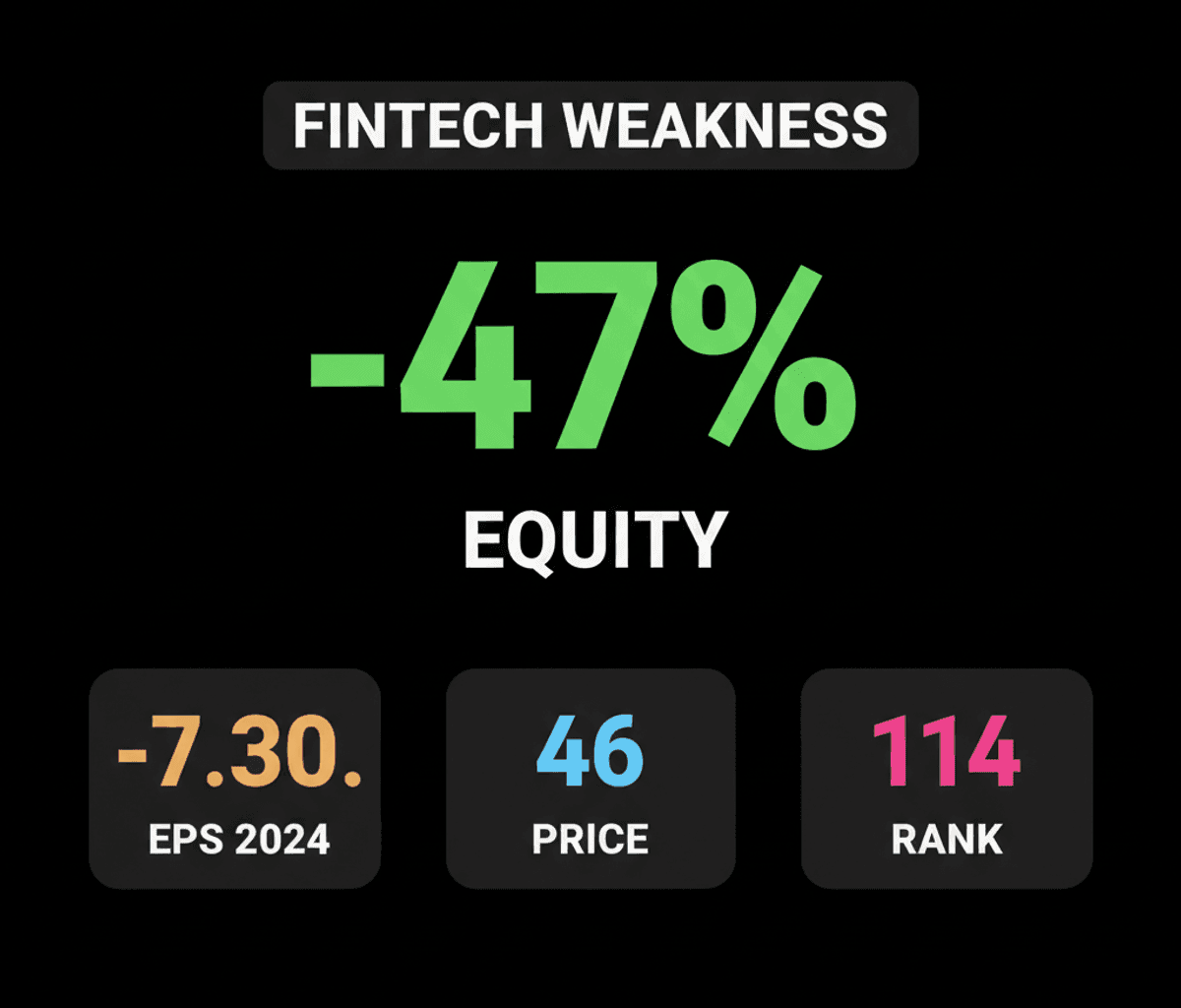

Specific ratings reveal underlying weakness: EPS Strength stands at a low 17, far below the recommended 80, suggesting poor earnings growth. Price Strength is also weak at 46, signaling underperformance over the last 12 months, compared to a recommended 80 or more.

Furthermore, Buyer Demand is ‘N/A’ due to insufficient price-volume data, and the Insurance-Brokers industry group itself ranks a low 114 out of 197, indicating broader sector struggles.

💰 Why It Matters

The consistently negative EPS, reported as -7.30 for 2024 and -7.33 for 2025, highlights significant profitability challenges. This trend is a critical concern for investors seeking companies with strong growth potential and healthy bottom lines.

A dismal Return on Equity of -47% coupled with negative cash flow of -20705.38 INR points to severe financial inefficiency. This suggests the company is struggling to generate value from its assets and manage its liquidity effectively.

The weak Price Strength (46) signals a lack of investor confidence and a stock that has underperformed the market. This makes it a less attractive option for those seeking robust capital appreciation.

The low Group Rank for the Insurance-Brokers sector suggests that even within its industry, Turtlemint isn’t operating in a high-performing segment. This adds another layer of caution for potential investors.

👀 What to Watch Next

Future earnings reports will be crucial to see if Turtlemint can reverse its negative EPS trend and demonstrate a path to profitability. Any significant improvement in financial health could be a catalyst for change.

Keep an eye on the broader digital insurance and fintech landscape for signs of increased competition or new market opportunities. Turtlemint’s ability to innovate and capture market share will be key.

Investors should also monitor for any strategic announcements, such as new funding rounds or partnerships, which could provide the capital and strategic direction needed to improve its market position and financial standing.