SEBI Buyback Rules: Tax-Efficient Capital Returns for Indian Firms

By Varun Mittal

SEBI’s new buyback rules make market repurchases a more tax-efficient way for Indian companies to return capital than dividends, boosting shareholder value.

A recent regulatory overhaul by the Securities and Exchange Board of India (SEBI) is fundamentally reshaping the landscape of corporate capital allocation in India, particularly for cash-rich companies. This strategic shift, as highlighted by Deepak Shenoy, founder and CEO of Capitalmind Mutual Fund PMS, positions market buybacks as a significantly more appealing and tax-efficient mechanism for returning capital to shareholders compared to traditional dividends.

The core argument for buybacks over dividends rests on two primary mechanisms: earnings per share (EPS) accretion and a more favorable tax structure. While dividends distribute profits across all outstanding shares, buybacks reduce the total share count. This reduction, assuming stable net income, inherently increases earnings per share, often leading to a positive market re-rating.

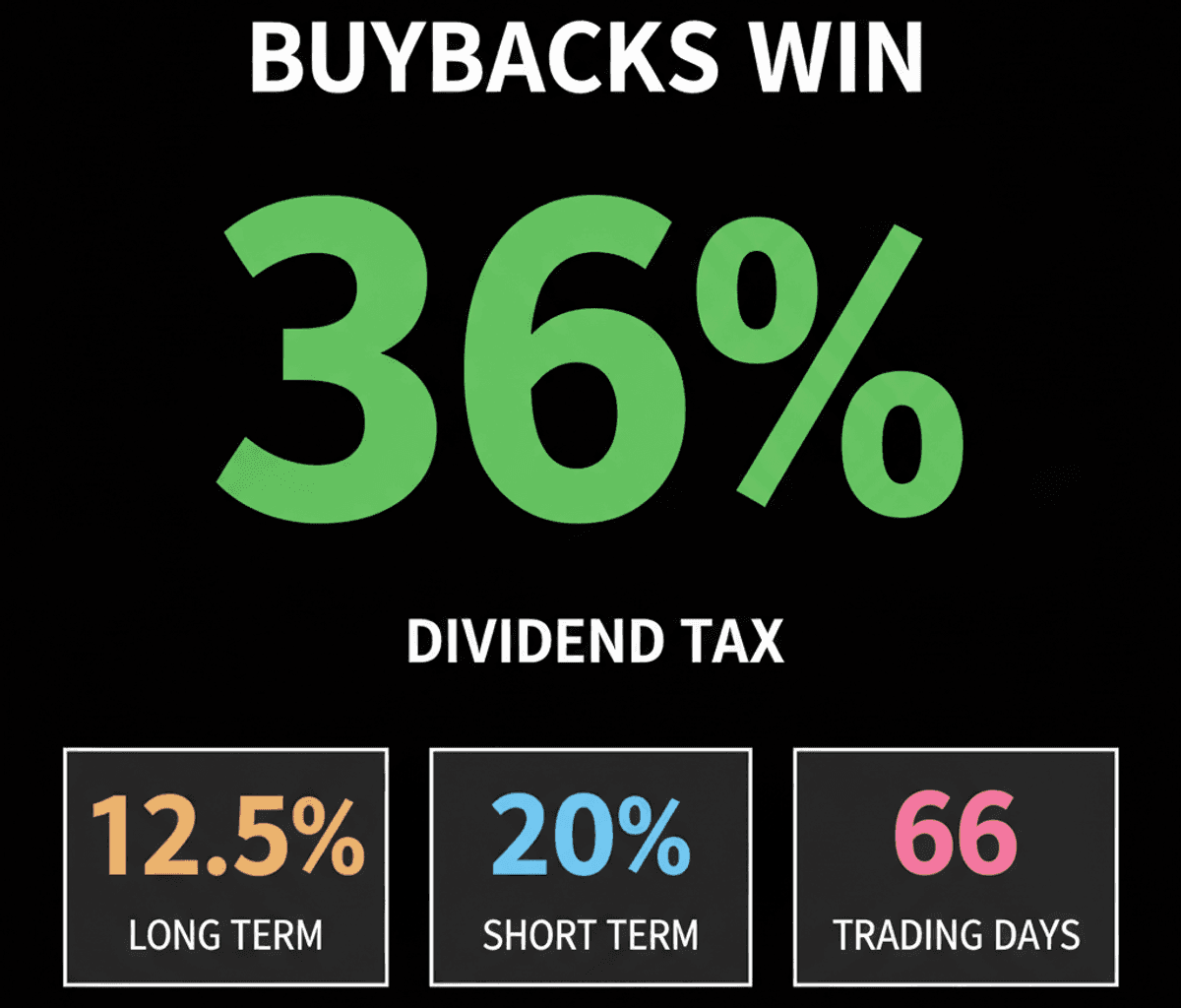

Crucially, the tax implications for shareholders have swung decisively in favor of buybacks. Dividends are subject to an individual’s income tax bracket, potentially reaching effective rates of up to 36% for some investors. In stark contrast, gains realized from selling shares back to the company in the open market are treated as capital gains, taxed at 12.5% for long-term holdings and 20% for short-term holdings. This significant tax arbitrage creates a powerful incentive for companies and shareholders alike.

Historically, market buybacks were encumbered by complex operational hurdles. The previous framework necessitated separate trading windows, the mandatory engagement of merchant bankers, and extensive monitoring by stock exchanges to differentiate between shares sold to the company and those traded among other market participants. This administrative burden often deterred companies from utilizing the mechanism.

SEBI’s updated framework has systematically dismantled these complexities. Companies no longer require dedicated buyback trading windows, and the need for merchant bankers to execute purchases has been eliminated. Firms can now conduct buybacks directly through their own trading accounts, streamlining the process considerably and reducing associated costs.

Further enhancing the integrity and efficiency of the process, SEBI has implemented clear safeguards. Promoters are now explicitly prohibited from selling their shares during the buyback period, removing a potential conflict of interest and the need for separate exchange monitoring. Companies are also mandated to finalize the buyback program within 66 trading days, with a minimum of 40% of the proposed buyback value to be completed within the first half of this period, ensuring commitment and execution.

For companies with substantial cash reserves, these changes represent a structural re-evaluation of capital return strategies. The regulatory simplification, coupled with the clear tax efficiency, positions market buybacks as a compelling, value-enhancing alternative to dividends. This shift encourages a more dynamic and economically rational approach to capital deployment, aligning corporate actions more closely with shareholder interests in a tax-optimized manner.