SBI Funds IPO Valuation: Scale vs. Revenue Yield

By ThePip Desk

SBI Funds Management’s IPO prices at a discount, revealing how asset mix and revenue yield, not just scale, dictate valuation in the AMC sector.

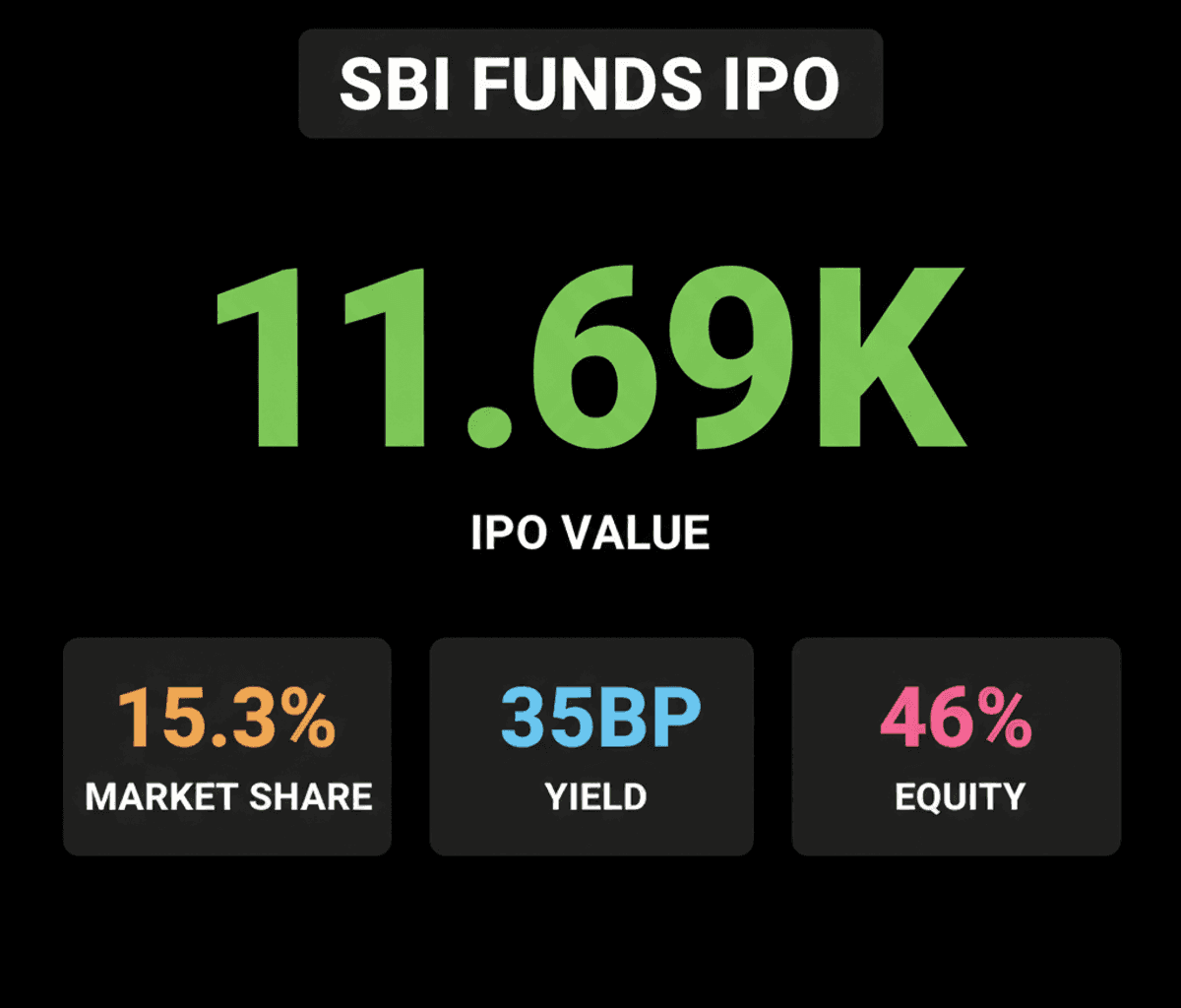

India’s largest asset manager, SBI Funds Management, is poised to launch its ₹11,692 crore Initial Public Offering on July 14. This event presents a compelling case study in asset management valuation, as the IPO is priced at a notable discount compared to its publicly listed peers, such as HDFC AMC and ICICI Prudential AMC, despite SBI Funds’ market-leading scale.

From a first-principles perspective, this valuation disparity underscores that sheer asset size, while impressive, does not automatically translate to a premium multiple. The underlying mechanism here is the structural composition of the asset base and its direct impact on revenue yield. SBI Funds Management oversees ₹12.51 lakh crore in mutual fund assets, commanding a substantial 15.3% market share by mutual fund quarterly average assets under management (QAAUM), solidifying its position as India’s largest AMC.

However, this vast scale is paired with a revenue yield of approximately 35 basis points. This figure stands notably below ICICI Prudential AMC’s 52 basis points and HDFC AMC’s 44 basis points. The primary driver for this lower monetization is the significant allocation of its mutual fund assets—32.4%—to passive products like exchange-traded funds (ETFs) and index funds. These products inherently feature lower expense ratios, resulting in reduced fee income. Furthermore, over 90% of the ₹16.9 lakh crore managed under its portfolio management and advisory mandates originates from provident and pension funds, which also operate on substantially lower fee structures compared to active retail mutual funds.

This structural characteristic of SBI Funds’ asset mix creates a discernible drag on its overall revenue generation capabilities per unit of asset, thereby influencing its valuation. The market, in essence, is pricing in the current reality of a lower blended fee income, irrespective of the company’s dominant market share in terms of AUM.

Nevertheless, a counter-thesis emerges from the company’s evolving asset dynamics. Management anticipates a narrowing of this valuation gap over time, citing a steady increase in equity assets, which now constitute nearly 46% of mutual fund assets, up from 36% in FY23. This shift towards higher-margin active equity products, coupled with a robust monthly Systematic Investment Plan (SIP) book exceeding ₹4,000 crore, suggests a potential for future revenue yield improvement.

A significant, yet currently under-leveraged, structural advantage for SBI Funds lies in its vast distribution network. Only about 55 lakh of State Bank of India’s 35 crore KYC-compliant customers currently invest through SBI Funds. This represents an enormous untapped potential to convert a captive customer base into higher-margin active equity assets, which could structurally enhance the company’s earnings profile over the long term. The IPO, structured as an Offer for Sale by State Bank of India and Amundi, does not raise new capital for the company itself.

Ultimately, the SBI Funds IPO illustrates a critical principle in financial markets: while scale offers a competitive moat, the specific structural composition of an asset manager’s product mix and its associated revenue yield are fundamental determinants of its valuation. The current discount reflects the present reality of its asset allocation, but the company’s ability to strategically shift its mix towards higher-margin active equity products and effectively leverage its unparalleled distribution network will dictate its future re-rating potential, providing a valuable lesson in how structural economics trump simple size.