Polycab India Stock Dips 5% Despite Record Q1 Earnings

By ThePip Desk

Polycab India’s stock fell 5% despite record Q1 FY27 profit and revenue. Investors weigh strong performance against high valuations. Learn more.

Polycab India’s stock saw a 5% dip over two trading sessions, including a 4% drop on Friday. This happened even as the company delivered its highest-ever Profit After Tax (PAT), revenue, and EBITDA for Q1 FY27.

The stock fell to ₹8,861 on the NSE, marking an 11% decline in July after an impressive 48% rally in the preceding three months. Investors are clearly weighing strong performance against existing valuations.

What Happened?

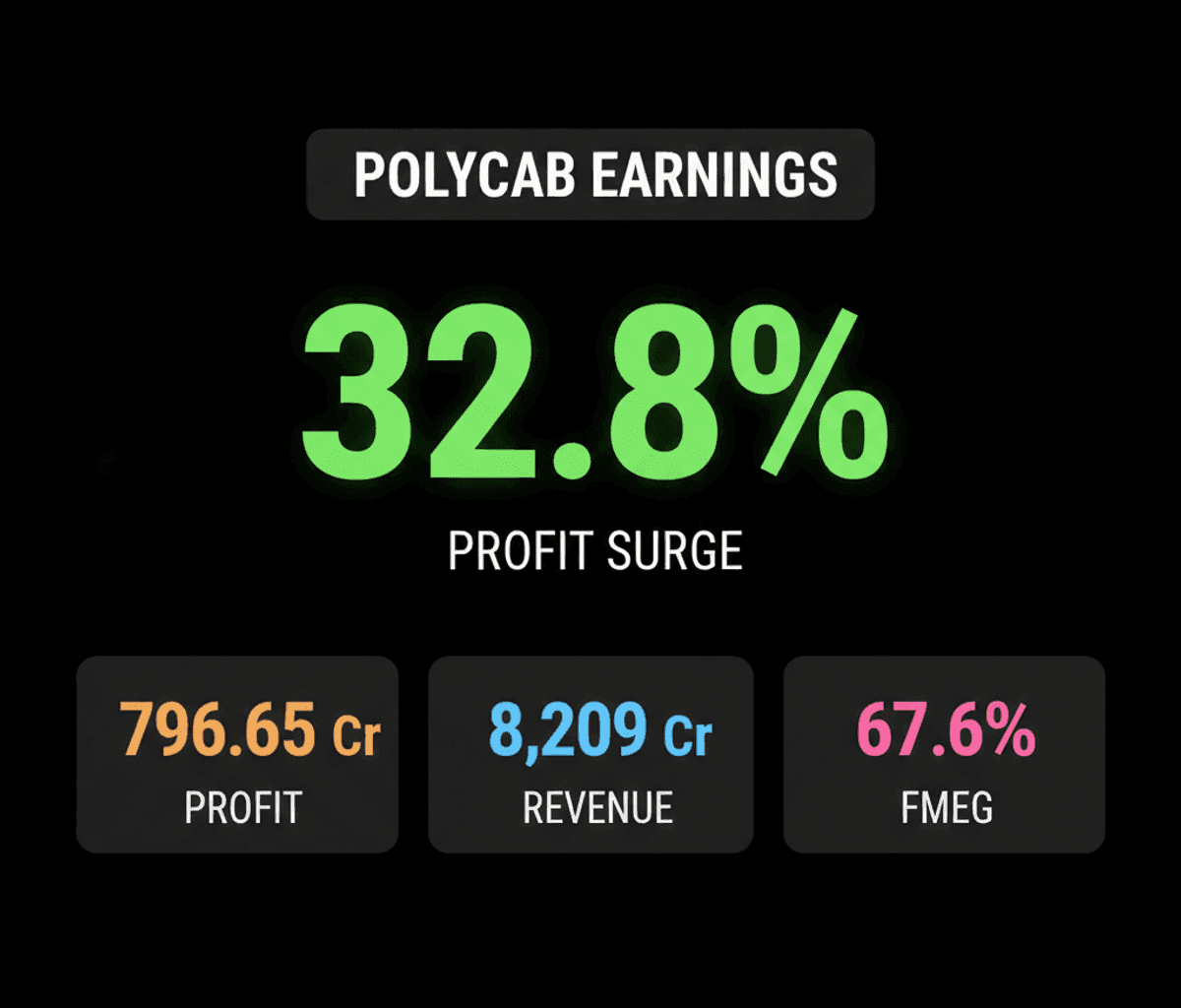

Polycab India reported a 32.8% year-on-year surge in consolidated net profit, reaching ₹796.65 crore for the quarter ended June 30, 2026. Revenue also jumped significantly, increasing 39% year-on-year to ₹8,209.70 crore.

The company’s largest business, wires and cables, recorded a 37.7% revenue increase. Fast-moving electrical goods (FMEG) revenue also soared by 67.6%.

However, the engineering, procurement, and construction (EPC) segment experienced an 11.4% year-on-year revenue decline. Polycab also announced a final dividend of ₹47 per equity share for its shareholders.

Why It Matters

The stock’s post-earnings dip suggests that investors might perceive Polycab’s current valuation as already pricing in its strong growth. Even record financial results are not enough to drive further immediate stock appreciation.

Brokerages like JM Financial and Equirus maintained their ‘Buy’ and ‘Add’ ratings respectively, citing robust Q1 performance and positive industry tailwinds. These include growth in power T&D, infrastructure, and data centers, confirming the company’s fundamental strength.

The significant revenue growth in wires, cables, and FMEG points to healthy consumer and industrial demand. This signals a positive underlying economic trend in these key sectors, which young investors should note.

Equirus specifically highlighted that current valuations likely factor in most positives, indicating limited potential for major earnings surprises in FY27E to trigger a re-rating. This suggests a cautious outlook on immediate upside.

What to Watch Next

Investors should closely monitor Polycab’s performance in upcoming quarters to see if it can sustain its exceptional growth. Continued outperformance could challenge current market perceptions about its valuation ceiling.

Keep an eye on broader economic developments and sector-specific tailwinds in power, infrastructure, and data centers. These external factors remain crucial drivers for Polycab’s future expansion.

Any new catalysts or unexpected growth vectors will be essential for the stock to achieve a significant re-rating. Without them, the market may remain cautious on further immediate price appreciation.