Poland’s 60% Windfall Tax: Energy Crisis Response

By Sivam

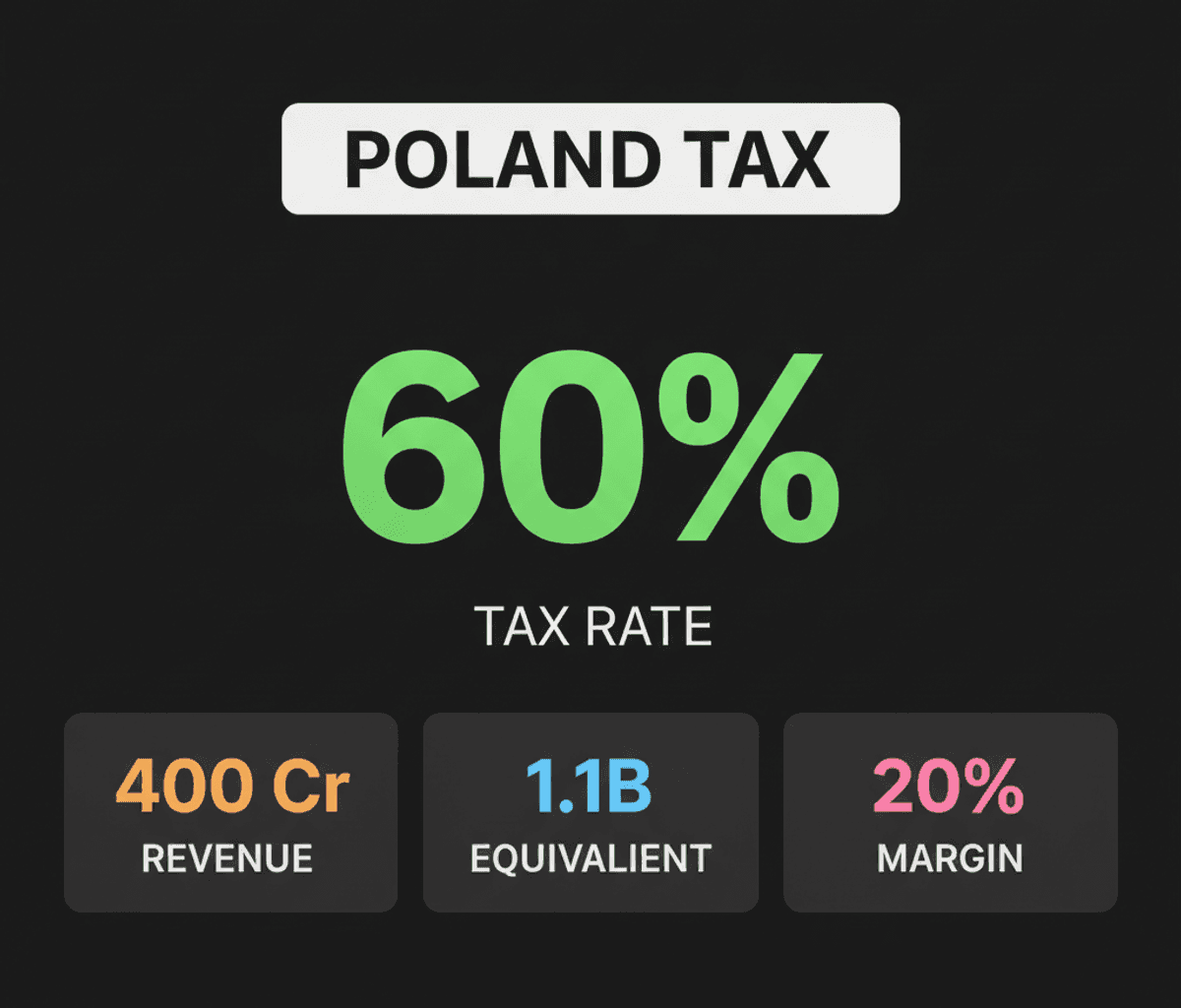

Poland imposes a 60% windfall tax on fuel companies’ 2026 excess profits to recover $1.1B in energy crisis subsidies. Learn about the economic impact.

The Polish government has approved a 60% windfall tax targeting excess profits generated by fuel companies between March and December 2026. This legislative action seeks to recoup approximately 4 billion zloty, equivalent to about $1.1 billion USD, which the state expended on consumer fuel subsidies. The core rationale behind this measure stems from the extraordinary market conditions created by the U.S.-Iran-Israel war and the subsequent closure of the Strait of Hormuz, events that precipitated a sharp surge in global energy prices.

This policy represents a direct governmental response to the structural shifts in market dynamics during periods of acute geopolitical instability. Rather than merely observing the market, the state intervened with subsidies to shield consumers, and is now seeking to rebalance its fiscal position by taxing the incremental profits reaped by a specific sector from these very same exogenous shocks. The mechanism defines excess profits as fuel sales margins that exceed a company’s average 2025 margin by more than 20%, explicitly distinguishing between profits from genuine operational improvements and those derived from unprecedented external factors.

The Polish Finance Ministry underscored that exceptional economic and geopolitical circumstances led to unusually high profitability within the fuel sector, simultaneously imposing substantial costs on the national budget. This move follows a series of emergency interventions by Warsaw, including temporary reductions in VAT and excise duties on fuels, alongside price controls, which collectively burdened Poland’s treasury by an estimated $435 million USD each month.

However, the implementation of such a structural policy is not without its challenges. The legislation, despite gaining parliamentary approval, requires the signature of President Karol Nawrocki, an opposition ally known for obstructing government fiscal initiatives. Furthermore, the approved 60% tax rate itself is a concession, reduced from an initial proposal of 75% after industry consultations warned that the higher rate could lead to an effective tax burden nearing 94% for some companies. This illustrates the tension between a government’s imperative to stabilize its finances and the need to maintain a viable operational environment for critical industries.

The Polish case offers a clear lens into the evolving role of governments in managing market outcomes during global crises. It highlights a recurring pattern where states, faced with the fiscal strain of consumer protection measures, turn to sector-specific levies on profits deemed