Meta’s Cloud Plan Sparks AI Chip Fears: History Repeats?

By ThePip Desk

Meta’s cloud capacity commercialization sparks AI semiconductor stock fears. Historical parallels suggest market overreaction, not an AI infrastructure bubble.

A recent announcement from Meta regarding its intention to commercialize surplus computing capacity as a new cloud service has ignited a significant selloff across semiconductor stocks. Investors quickly interpreted this move as a potential signal that major technology companies might have overinvested in AI infrastructure, sparking widespread concern about a future deceleration in demand for advanced semiconductors.

This market reaction, which also impacted neo-cloud providers like CoreWeave and Nebius, reflects a recurring pattern of fear where perceived oversupply triggers rapid divestment. We understand the immediate pull to connect a potential surplus with a market bubble, especially in a sector like AI that has seen explosive growth.

However, the narrative of a sudden, widespread AI infrastructure surplus often overlooks deeper historical parallels. Consider the genesis of Amazon Web Services (AWS), which began by leasing out Amazon’s own surplus server capacity. Global investment bank Jefferies explicitly characterized Meta’s approach as a normal business model, drawing a direct line to AWS’s origins, which evolved from internal efficiencies into a foundational cloud provider.

A closer look at the data reveals several nuances that challenge the ‘excess capacity’ theory. Meta, until very recently, faced significant computing power constraints, even engaging in new contracts with neo-cloud providers. Reports indicated Google declined Meta’s request for increased Gemini computing capacity due to its own limitations, and Meta’s management instructed employees to reduce AI token consumption—all suggesting persistent resource scarcity.

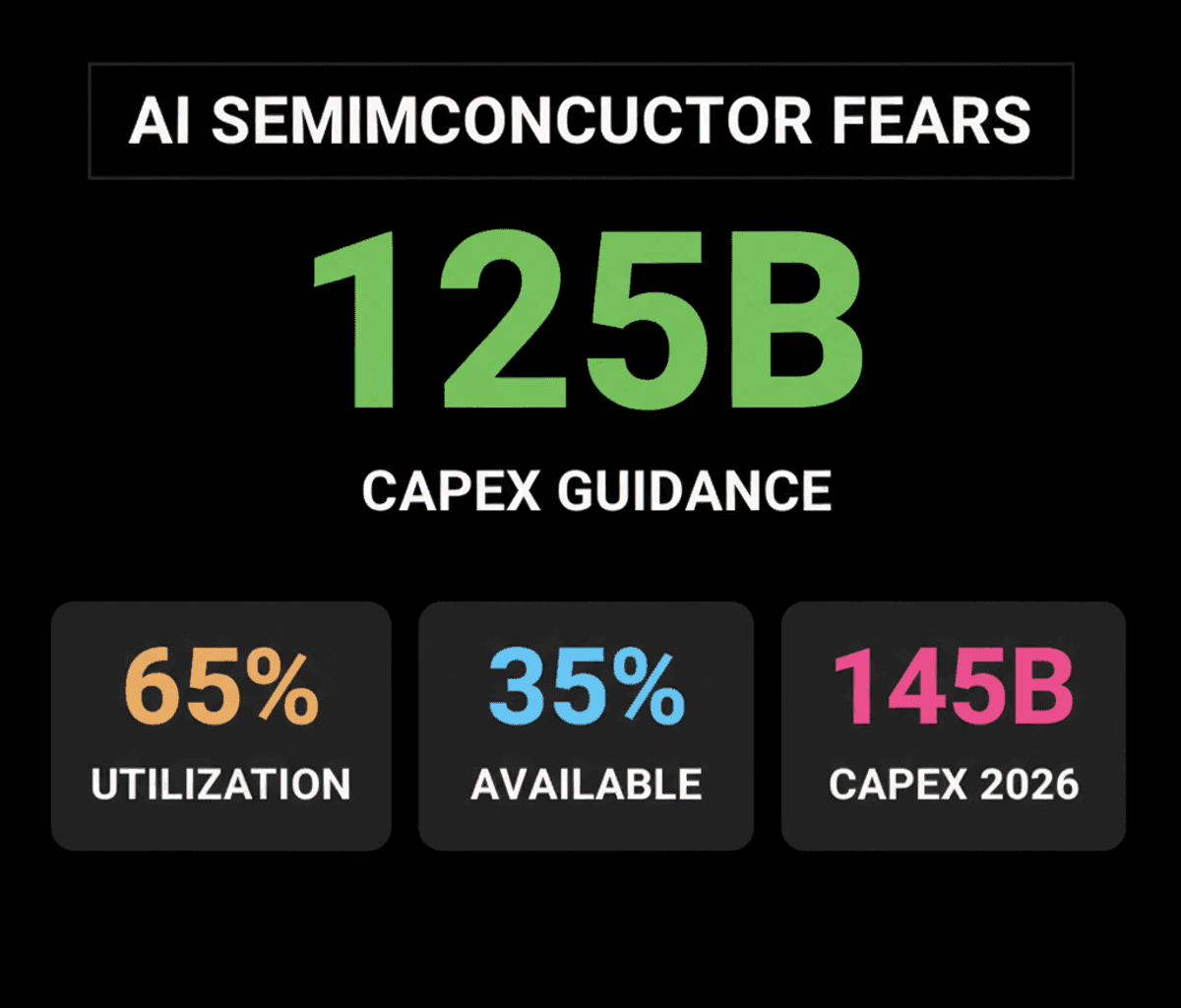

Furthermore, Meta has maintained its substantial capital expenditure (CAPEX) guidance of $125 billion to $145 billion for 2026. Analysts argue that a rapid shift from severe shortage to a surplus within mere months is highly improbable, given the extensive manufacturing, delivery, installation, and deployment timelines for critical components like GPUs, HBM, and AI servers. Jefferies also noted Meta’s internal infrastructure utilization is currently around 65%, leaving approximately 35% available for commercialization, a strategic business decision rather than a sign of industry saturation.

What many often misunderstand in these cycles is the difference between a strategic business evolution and an industry-wide oversupply. The market’s swift reaction often fails to account for the long lead times required for next-generation platforms, necessitating early procurement. The limited decline in Nvidia’s shares, compared to other semiconductor stocks, further hints at a more complex market assessment.

Ultimately, the recent selloff in AI semiconductor stocks may not be the definitive harbinger of weakening demand that some fear. Instead, it could represent a natural valuation correction and profit-taking by institutional investors at the close of the first half of the year, a common occurrence in fast-growing sectors. These market movements, while unsettling, often reflect a cyclical re-evaluation rather than a fundamental shift in long-term technological demand.