India’s Wavelength Meter Market: Growth Amidst Import Reliance

By ThePip Desk

Explore India’s wavelength meter market dynamics: high import dependence, projected 9-12% CAGR, and key drivers like R&D and semiconductor manufacturing.

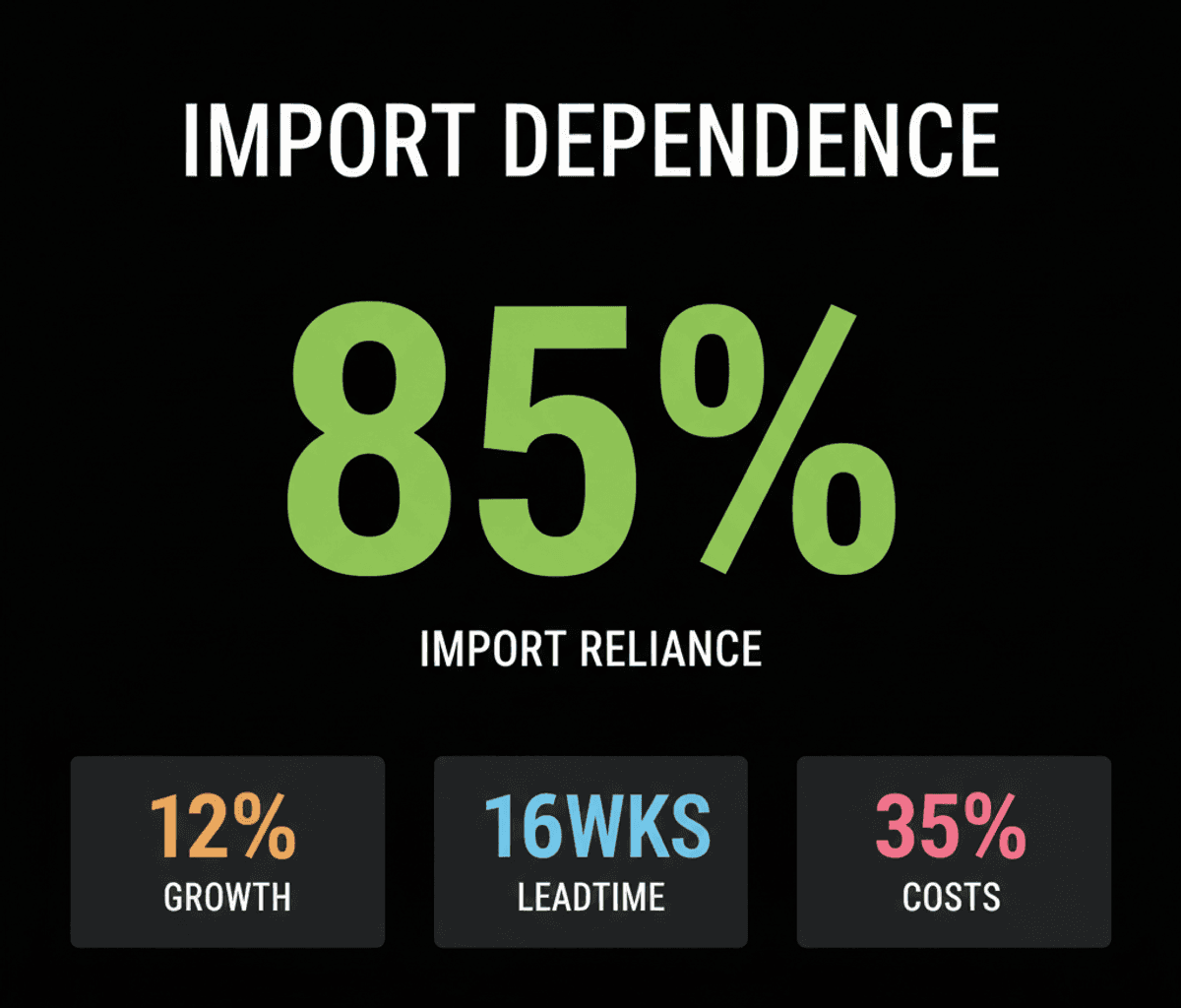

India’s wavelength meter market exemplifies a niche segment with profound structural import dependence, with an estimated 80-85% of units sourced from global leaders in Germany, Japan, and the United States. These precision instruments, essential for picometer-level laser wavelength accuracy, underpin critical functions in government research, emerging semiconductor fabrication, defense, and commercial laser integration.

The underlying mechanism driving this market is a confluence of expanding photonics R&D and advanced manufacturing needs. Demand primarily originates from R&D and metrology labs, accounting for 40-45% of uptake, followed by semiconductor and precision manufacturing at 25-30%, and telecommunications/optical network testing contributing 15-20%.

From a structural perspective, the market is poised for robust expansion, with unit demand projected to grow at a Compound Annual Growth Rate (CAGR) of 9-12% through 2035. The value segment is anticipated to outpace this slightly, forecast at a CAGR of 10-13%, signaling a shift towards premium-tier models offering sub-0.1 picometer accuracy and multi-channel capabilities.

Key market trends reinforce this growth trajectory, notably a pronounced shift towards multi-wavelength and high-speed measurement systems. This is particularly evident as Indian semiconductor fabs and laser system integrators upgrade their production lines to integrated solutions. Furthermore, the increasing adoption of compact, portable wavelength meters serves field-service teams in telecom and defense, while calibration-as-a-service and rental models gain traction among smaller R&D labs, mitigating upfront capital expenditure.

However, the market faces structural headwinds. Long lead times of 8-16 weeks for imported precision components, coupled with significant additional costs of 25-35% due to import duties and freight volatility, present ongoing challenges. A critical shortage of trained metrologists and service engineers exacerbates these issues, increasing reliance on expensive overseas annual maintenance contracts. The absence of a dedicated Indian standards certification for wavelength-measurement instrumentation further complicates import clearance and periodic re-validation.

The competitive landscape remains dominated by global specialist manufacturers such as Keysight Technologies, Bristol Instruments, Toptica Photonics, HighFinesse, and Yokogawa. These entities compete primarily on accuracy, wavelength range, and software integration. The top three global OEMs collectively command an estimated 55-65% of unit sales through their Indian channel partners, who primarily provide local support and recalibration services rather than manufacturing key optical components.

The enduring lesson here is that while India’s technological ambitions drive demand for advanced instrumentation, the foundational reliance on highly specialized global manufacturing creates distinct market dynamics. Opportunities for domestic players lie not in direct component manufacturing, but in establishing robust, NABL-accredited local calibration and service centers, or supplying wavelength-meter modules to emerging Indian photonics integrators, thereby addressing crucial service gaps in the value chain.