India’s Power Sector: Capex Cycle & Leverage Until FY30

By ThePip Desk

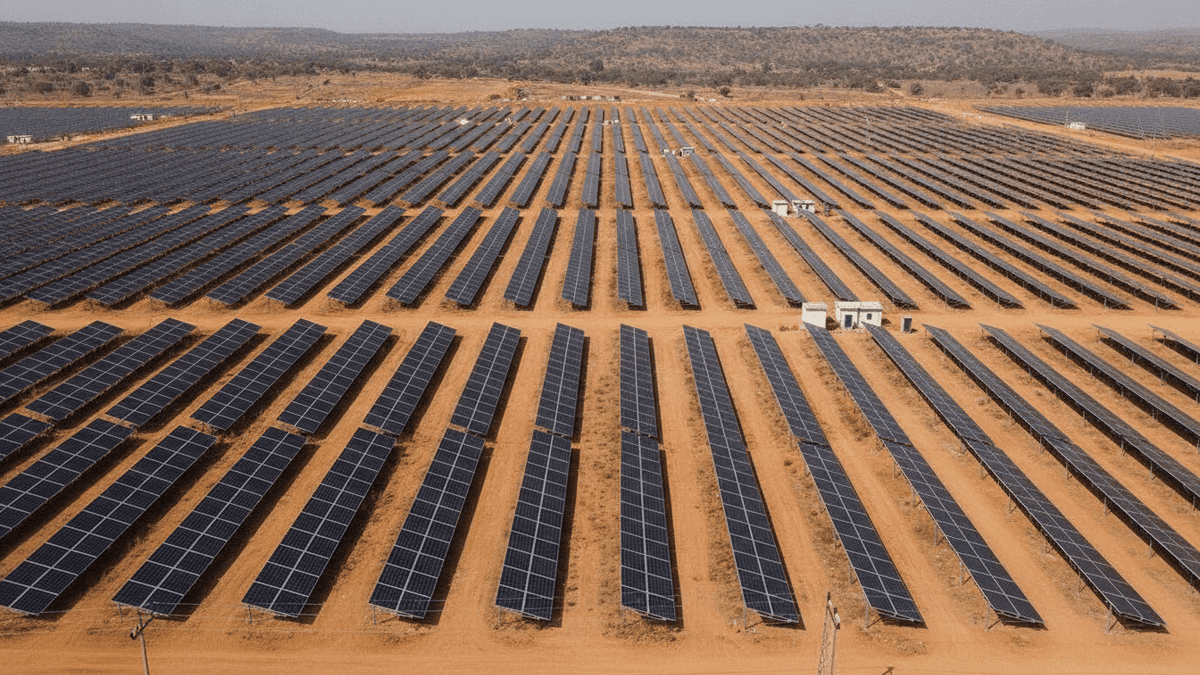

India’s power sector sees major capex, driven by renewables & storage. Equirus report forecasts increased private sector leverage until FY30, stabilizing post-commissioning.

India’s power sector is undergoing a profound multi-year transformation, marked by an aggressive capital expenditure (capex) cycle that prioritizes renewable energy, advanced storage solutions, and strategic thermal capacity additions. This substantial investment, detailed in a recent Equirus report, signals a structural shift. The report projects that private sector participants will experience increased balance sheet leverage until fiscal year 2030, a temporary condition expected to stabilize as these newly developed assets become fully operational and begin generating revenue.

This dynamic illustrates a classic capital cycle in infrastructure development. Companies commit significant upfront capital to build large-scale projects, which inherently increases their debt-to-equity ratios during the construction phase. The leverage is not necessarily a sign of distress but rather a predictable outcome of funding long-gestation assets. As these projects transition from development to operation, cash flows improve, allowing for debt reduction and balance sheet de-risking.

Key private players are leading this expansion with ambitious targets. Torrent Power, for instance, aims to achieve a renewable capacity of 10 gigawatts (GW) by FY30, alongside an 8.4 GW pumped storage pipeline. This strategic move is poised to more than double its current operational footprint, fundamentally reshaping its generation mix. Similarly, JSW Energy is pursuing a comprehensive “Strategy 3.0” roadmap, targeting a 30 GW generation capacity and 40 GWh of storage. These expansions are projected to drive up the gross block per megawatt (MW) to approximately Rs 63 million/MW, reflecting the intensity of capital deployment.

Concurrently, state-owned NTPC is maintaining a focused approach on regulated equity, with plans to expand its capacity to 67 GW by FY30. NTPC’s strategy is designed to keep its leverage comfortably within the 3.5-4.0x Net Debt/EBITDA range, leveraging the stability offered by regulated assets. This dual-track approach—aggressive private expansion and steady public sector growth—underscores the comprehensive nature of India’s power sector evolution.

The period between 2026 and 2030 is identified as critical for the timely execution and commissioning of these projects. These milestones are not merely operational checkpoints; they are vital earnings catalysts that will drive the sector’s journey towards enhanced profitability. The successful transition from high-capex, high-leverage development to revenue-generating operations will define the long-term structural gains for the Indian power landscape.