India’s Ports: Containerization Drives Structural Growth

By Business Desk

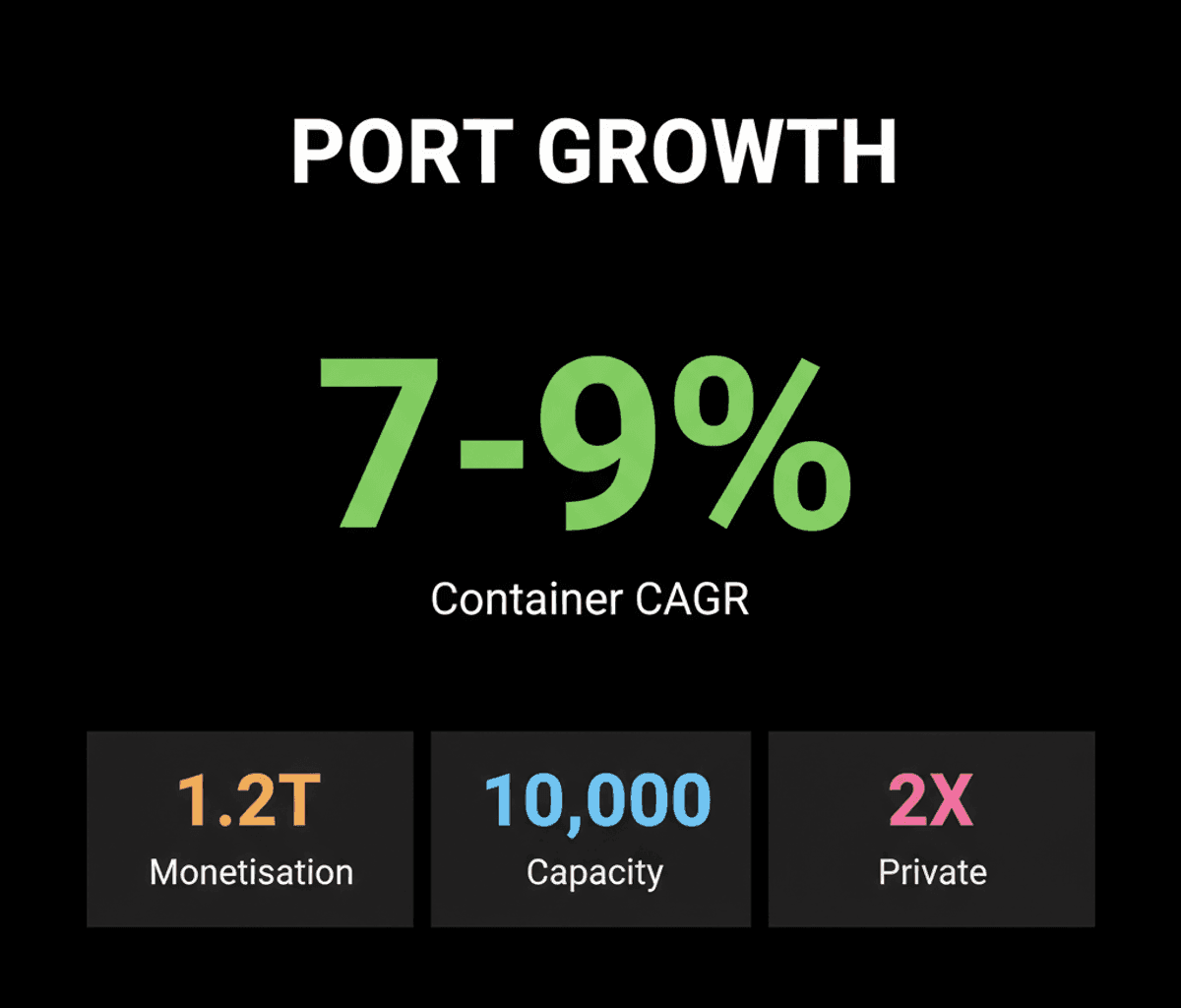

India’s port sector is experiencing a major structural shift, with container volumes becoming the primary growth driver, projected at 7-9% CAGR.

India’s port sector is entering a distinct growth phase, fundamentally reshaped by the increasing dominance of container volumes. This structural shift is projected to drive a robust 7-9% Compound Annual Growth Rate (CAGR) for container traffic between FY26 and FY28, according to a research report by Motilal Oswal Financial Services. The analysis underscores a pivot from traditional bulk cargo, positioning containerization as the central mechanism for the sector’s expansion.

This acceleration in container traffic is not merely a cyclical uptick; it represents a deeper structural trend. Favorable macroeconomic conditions, coupled with rising domestic consumption, are fueling greater adoption of containerization across various industries. This efficiency-driven shift in logistics underpins the sustained growth trajectory, as businesses increasingly leverage standardized shipping for cost and speed advantages.

The broader port industry is anticipated to grow at 4-5% over the medium term, but private sector players are positioned for disproportionate gains. Entities like Adani Ports (APSEZ) and JSW Infrastructure (JSWINFRA) are projected to achieve growth rates two to three times the industry average. This outperformance is supported by their ongoing organic and inorganic expansions, alongside the strategic integration of comprehensive logistics solutions, as highlighted by Motilal Oswal’s report.

Motilal Oswal forecasts Adani Ports’ revenue to grow at a 17% compounded annual rate, with EBITDA increasing by 18% and Profit After Tax (PAT) by 22% between FY26 and FY28. Similarly, JSW Infrastructure is projected for a 19% compounded annual volume growth, alongside revenue rising 39%, EBITDA 34%, and APAT 31% over the same period. These figures illustrate the significant operational leverage and expansion capacity within the private segment.

Crucially, policy support provides a significant tailwind to this structural transformation. Under the National Monetisation Pipeline 2.0 (NMP 2.0), the government has earmarked 44 brownfield port infrastructure projects for monetisation via Public-Private Partnership (PPP) models. This initiative aims to unlock INR 1.2 trillion during FY26-FY30, directly contributing to capacity expansion and modernization. The broader Maritime Amrit Kaal Vision 2047 targets an ambitious increase in India’s total port handling capacity from 2,800 MTPA to 10,000 MTPA by 2047, alongside developing six mega ports.

The commodity mix traversing Indian ports is also undergoing a significant rebalancing. Coal traffic is anticipated to decline at a compounding rate of 2-4% as domestic production increases and renewable energy adoption expands. Conversely, iron ore traffic is expected to recover with a 5-7% CAGR during FY26-FY28, driven by increased coastal movement. Petroleum, Oil, and Lubricants (POL) traffic is projected for a moderate 2-4% CAGR over the same period, influenced by stable fuel demand tempered by improving fuel efficiency.

A look at FY26 data reveals a divergence in performance between major and non-major ports. India’s major ports demonstrated robust growth, with cargo volumes increasing approximately 7% year-over-year to 915 MMT. This was powered by healthy expansion in both overseas traffic (+6.6% YoY) and coastal traffic (+8% YoY), with POL & crude leading at 16% YoY growth. In contrast, non-major ports reported more modest growth, with cargo volumes rising about 1.4% year-over-year to 753 MMT in FY26.

Despite these strong growth drivers and strategic positioning, the sector is not without its inherent risks. Geopolitical tensions, intensified competition from both private and regional ports, volatility in global trade flows, and potential uncertainties surrounding policy and regulation all present headwinds. These factors could impact the pace and trajectory of the projected expansion, requiring agile strategic responses from operators and policymakers alike.

India’s strategic location within the Indian Ocean, complemented by an extensive network of 20,275 km of national waterways across 24 states, fundamentally positions it to emerge as a preeminent global maritime player. This structural advantage, aligning with 80% of the global maritime oil trade, suggests a long-term trajectory towards becoming a significant hub. The ongoing transformation, led by containerization and strategic investments, solidifies the foundational elements for sustained maritime leadership.