India’s Options Market Dominance: Reshaping Exchange Revenue

By ThePip Desk

India’s stock market sees equity options drive 70% of exchange revenue, shifting focus from price to volatility. Explore this structural transformation.

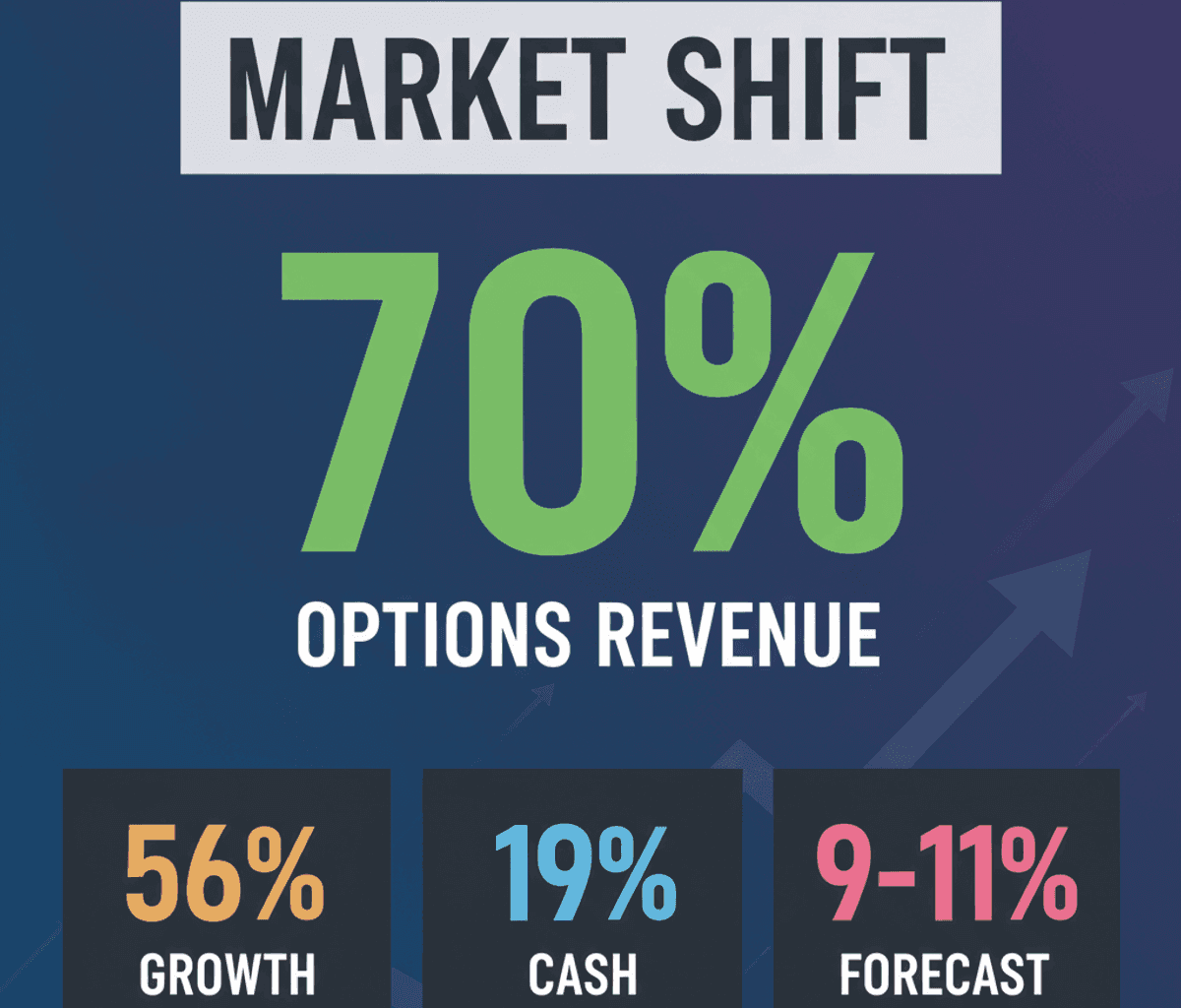

India’s stock market has undergone a fundamental structural transformation, moving from a cash-dominated arena to one heavily influenced by derivatives trading. A recent report by Jefferies highlights that equity options now constitute nearly 70% of Indian exchanges’ operating revenues, signifying a profound shift in how these financial institutions generate their earnings. This evolution means that market volatility, rather than the simple direction of stock prices, has become the primary determinant of exchange profitability.

The underlying mechanism driving this change is the exponential growth in derivatives activity. Between fiscal years 2020 and 2026, India’s equity options market experienced a remarkable 56% compound annual growth rate (CAGR). This figure starkly contrasts with the cash market’s 19% CAGR over the same period, illustrating the disproportionate expansion of options trading within the broader market ecosystem. This data underscores a critical insight: an exchange’s revenue model is now intrinsically linked to the frequency and intensity of trading in these complex instruments.

The National Stock Exchange (NSE) stands as the principal beneficiary of this structural pivot. It commands approximately 70% of all Indian exchange revenues and holds over 90% market share across most trading categories. Notably, equity options alone contributed 77% of NSE’s transaction revenues in FY26. While India trades a higher volume of option contracts than the United States, the overall value of premiums traded remains considerably smaller, primarily due to frequent expiry-day trading and smaller ticket sizes.

Further dissecting the market’s composition, the Jefferies report clarifies that retail investors with low annual option turnover contribute a minimal percentage to NSE’s total turnover. This suggests that the bulk of these significant trading volumes are driven by larger, more active institutional participants or sophisticated individual traders, reinforcing the structural, rather than purely retail-driven, nature of this market shift.

Looking ahead, while options trading will remain a crucial earnings driver, its explosive growth rate is projected to moderate. This anticipated deceleration stems from several regulatory interventions implemented by the Securities and Exchange Board of India (SEBI), including increased securities transaction tax (STT) on derivatives, restrictions on weekly index option expiries, larger lot sizes, and enhanced surveillance measures. The NSE’s Draft Red Herring Prospectus (DRHP) forecasts a more tempered 9-11% CAGR for equity options between FY26 and FY30, a rate slower than the projected growth for cash equities and commodity options.

This structural recalibration of India’s stock market profoundly impacts how one assesses the health and profitability of its exchanges. What many observers might overlook is that in this derivatives-dominated environment, the traditional focus on rising stock prices as a proxy for market success is incomplete. Instead, understanding the dynamics of volatility and the regulatory landscape governing derivatives becomes paramount for grasping the true underpinnings of exchange earnings and the broader financial architecture.