Indian FMCG Acquisitions: The Nutraceutical Buy Strategy

By ThePip Desk

Indian FMCG giants are strategically acquiring nutraceutical brands, leveraging distribution to rapidly scale in a booming market. Learn why ‘buy’ beats ‘build’.

A significant strategic pivot is underway within India’s Fast-Moving Consumer Goods (FMCG) sector, as major players increasingly opt for outright acquisitions in the nutraceutical space rather than attempting organic brand development. This shift represents a fundamental “build versus buy” decision, where the imperative for rapid market penetration and instant credibility in a dynamic category is decisively favouring the acquisition model.

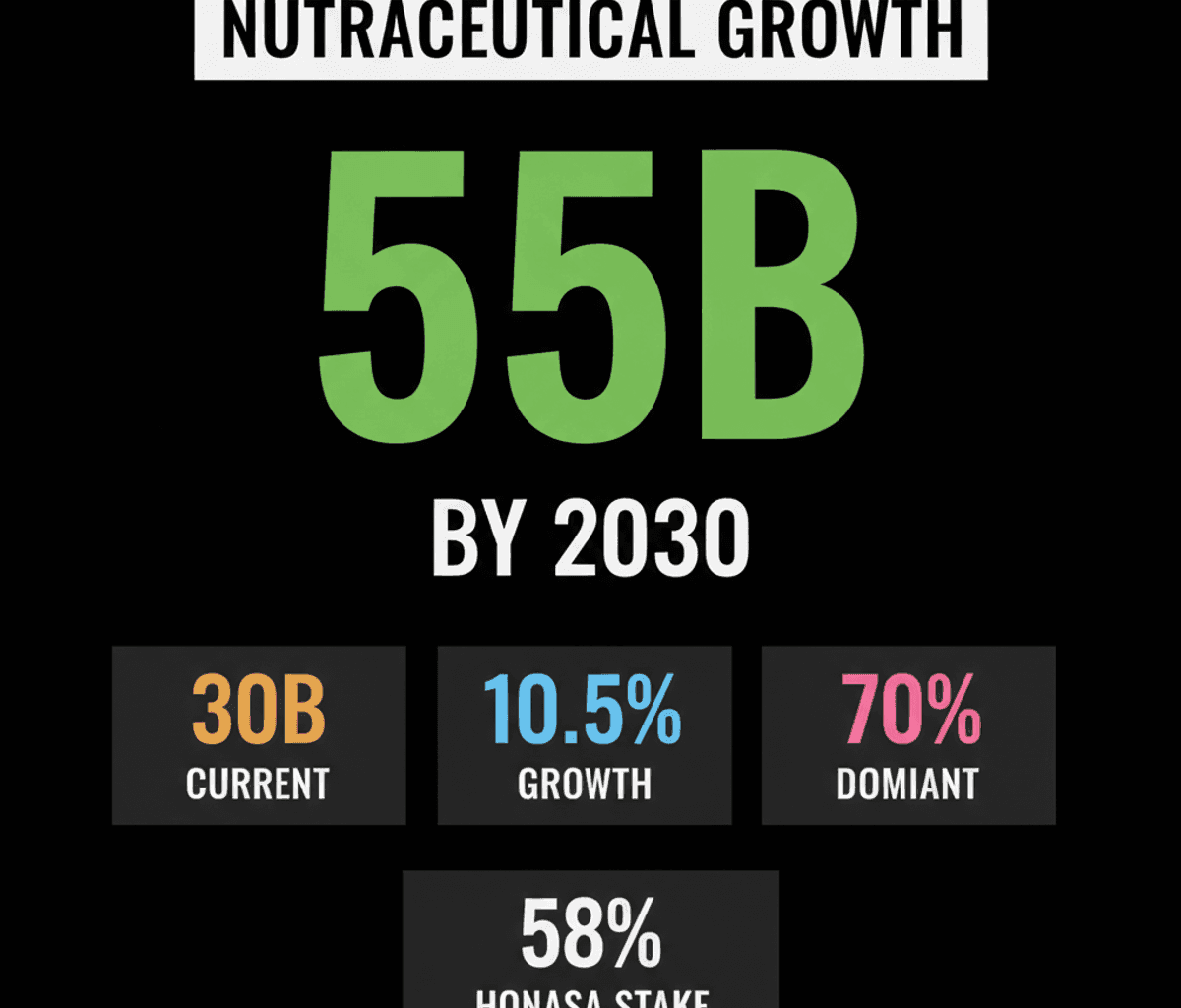

Recent high-profile transactions underscore this calculated strategy. Honasa Consumer, for instance, secured a 58% stake in Fluence Pharma. Hindustan Unilever (HUL) moved to fully acquire OZiva, while Marico invested in a majority stake in Cosmix. Beyond these, USV Pharma has backed Wellbeing Nutrition, and L’Oréal is reportedly in discussions to acquire Innovist, signalling a broad industry consensus on this approach.

The underlying driver for this acquisition spree is the substantial and accelerating growth of India’s nutraceutical market. Currently valued at approximately $30 billion, projections indicate it will surpass $55 billion by 2030, exhibiting a robust annual growth rate of about 10.5%. Within this expansion, functional foods and beverages, particularly protein-based products, dominate, constituting nearly 70% of the market. This surge is directly attributable to escalating consumer awareness regarding preventive healthcare and holistic wellness.

For large FMCG incumbents, the “buy” strategy offers an invaluable accelerant. Their internal product development cycles are often too slow and risk-averse to effectively compete in a market segment characterised by rapid maturation and a strong Direct-to-Consumer (D2C) ethos. Acquisitions allow these giants to immediately gain access to established products and, crucially, consumer trust, bypassing the protracted and capital-intensive initial phase of category creation and brand building.

Once acquired, FMCG firms deploy their unparalleled distribution muscle. Their extensive networks, encompassing traditional offline retail, modern trade channels, and the burgeoning quick-commerce ecosystem, are leveraged to scale these typically digital-first nutrition brands nationally. This mechanism effectively transforms niche D2C successes into mainstream offerings, a scaling capability that startups inherently lack. In contrast, traditional pharmaceutical companies have largely remained on the sidelines, deterred by the distinct manufacturing, branding, and regulatory requirements that diverge significantly from their core operations.

While the strategy has shown early promise, with OZiva’s revenue reportedly increasing post-HUL’s investment and Marico’s digital-first portfolio demonstrating strong growth, a critical challenge looms. Scaling an acquired brand without diluting its original value proposition and hard-won credibility is complex. Consider Fluence Pharma, whose success is deeply rooted in dermatologist recommendations. An aggressive, mass-market expansion could inadvertently erode its premium, medically-backed positioning, a key element of its original appeal.

This structural pattern highlights a clear division of labour: agile startups are adept at discovering and validating new consumer categories, while large incumbents possess the formidable resources to scale them. The ultimate success of these nutraceutical acquisitions will therefore hinge on a nuanced balance – preserving the acquired brand’s inherent trust and unique selling points while simultaneously extending its market reach. This trend reflects a broader, fundamental consumer shift towards health and nutrition products where efficacy and specific benefits increasingly outweigh traditional branding or legacy claims, forcing incumbents to adapt their growth models.