Indian Bonds Volatile: Oil Surge & Index Inclusion Fears

By ThePip Desk

Indian government bonds saw significant weekly yield increases, driven by soaring oil prices and uncertainty over potential index inclusion. Market sentiment cautious.

Indian government bonds registered a notable tumble on Friday, culminating in the benchmark yield’s most substantial weekly increase in eight weeks. This market movement was primarily driven by a sharp escalation in global oil prices and persistent uncertainty surrounding a potential index inclusion announcement, compelling traders to reduce their risk exposure ahead of the weekend.

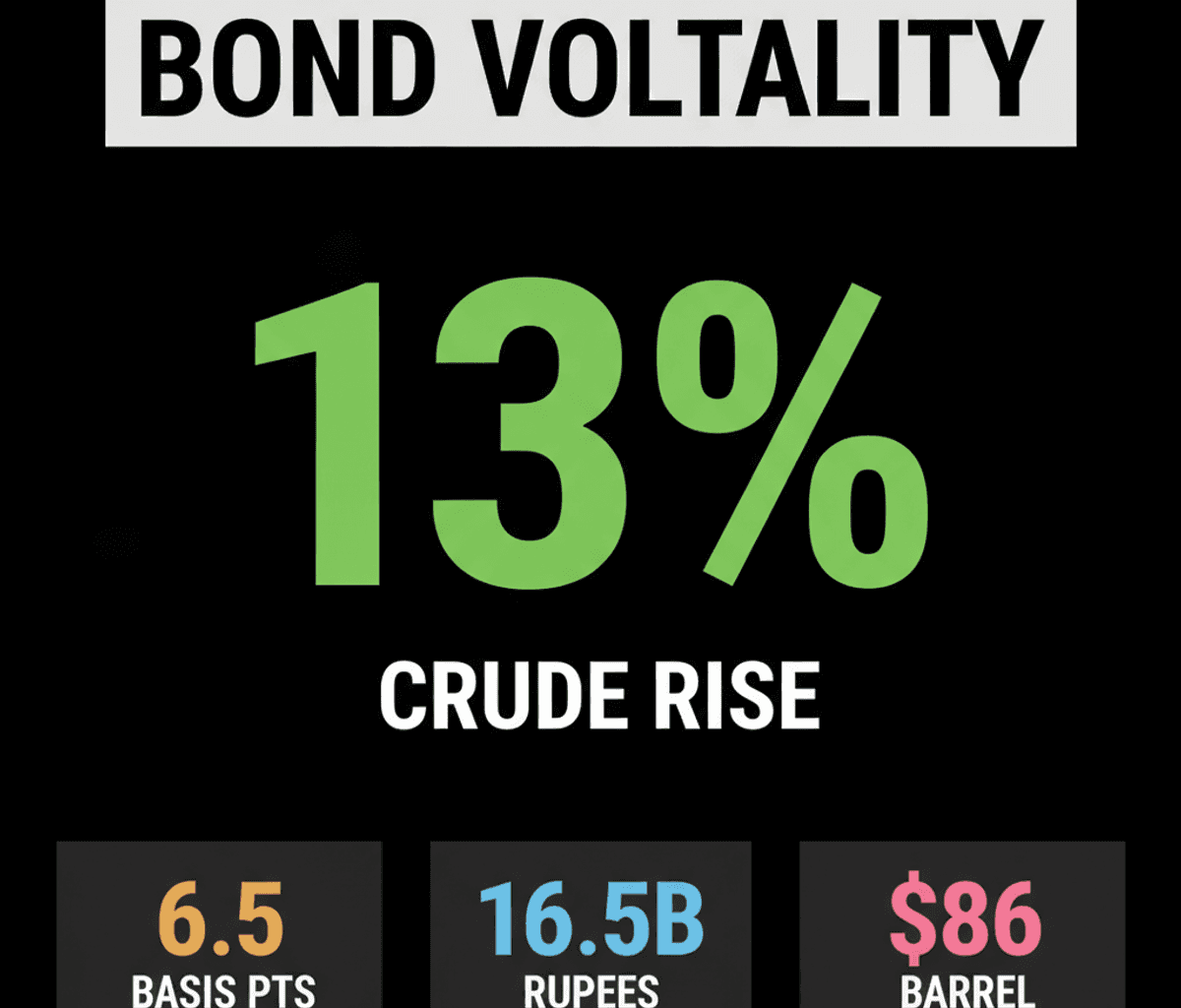

The benchmark 6.94% 2036 bond yield closed at 6.7799%, marking an increase from Thursday’s 6.7478%. Over the course of the week, this yield rose by 6.5 basis points, reflecting the intensified selling pressure. The core mechanism behind this pressure stems from Brent crude futures, which surged nearly 2% to $86 per barrel, achieving an approximate 13% weekly rise. This spike was largely attributed to heightened tensions and disruptions to oil traffic through the Strait of Hormuz, linked to intensified fighting between the U.S. and Iran.

For India, a nation heavily reliant on oil imports, higher crude prices introduce a clear set of structural risks. These include a potential depreciation of the rupee, a widening of the national import bill, and increased strain on government finances. Historically, such external commodity shocks have a direct, adverse impact on domestic bond markets as inflation expectations rise and fiscal stability concerns mount.

While earlier in the period, softer U.S. inflation and Producer Price Index (PPI) data had scaled back expectations for further U.S. rate hikes—a factor that typically supports emerging-market bonds—the immediate concerns over oil and index inclusion superseded this positive signal. Foreign demand for Indian bonds had remained robust, with overseas investors net buying approximately 16.5 billion rupees of bonds under the fully accessible route, largely anticipating a potential inclusion in Bloomberg’s index. However, the absence of this anticipated news, coupled with rising crude prices, triggered a risk-off selling pattern among traders.

This dynamic suggests that market participants are prioritizing immediate, tangible risks over broader, more gradual shifts in global monetary policy. The collective decision by traders to pare risk, evidenced by the increase in India’s overnight index swap rates, indicates a prevailing sentiment that could lead to continued selling in the subsequent trading week, underscoring the market’s sensitivity to both geopolitical commodity shocks and the definitive resolution of index-related speculation.