India Inc. Q1 FY27: Price-Led Growth Masks Margin Pressures

By ThePip Desk

India Inc. saw 11-11.5% revenue growth in Q1 FY27, driven by price hikes, not volume. Discover the underlying margin pressures and challenges for sustainable expansion.

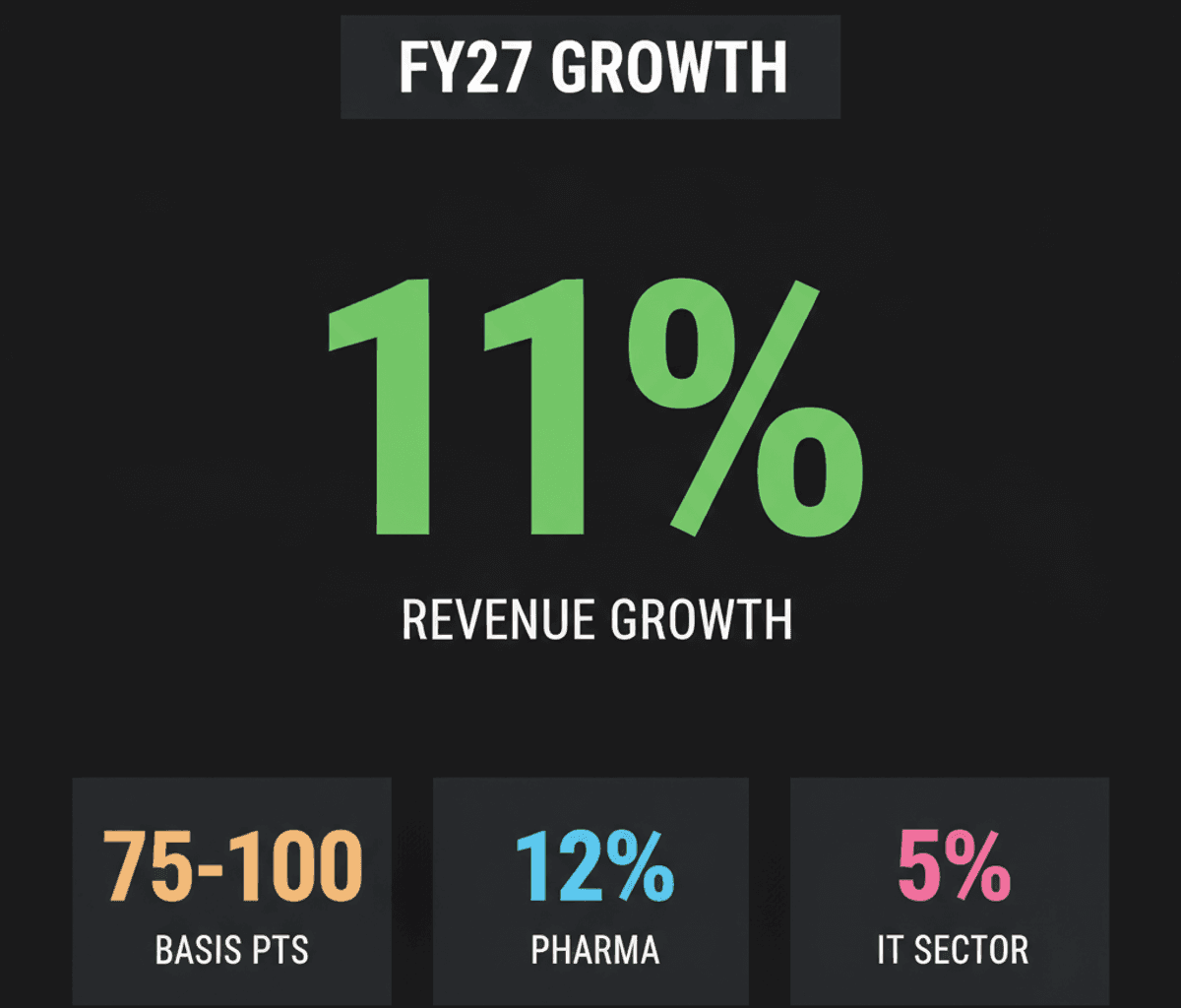

Indian corporations registered an 11% to 11.5% revenue growth in the first quarter of fiscal year 2027, a figure primarily propelled by price increases rather than a genuine surge in sales volumes, as estimated by CRISIL. This structural pattern indicates a challenging environment where companies struggle to achieve volume-led expansion, instead relying on their pricing power to offset rising expenses.

The underlying mechanism for this trend is clear: elevated input costs, significantly exacerbated by persistent geopolitical tensions impacting global freight and raw material prices. While revenue numbers appear robust, the reliance on price hikes suggests a broader market dynamic where demand elasticity is being tested, and sustainable, organic growth remains elusive for many sectors.

Consequently, overall operating profit margins are projected to contract by 75 to 100 basis points compared to the previous year. This margin compression highlights the difficult balancing act companies face: passing costs to consumers risks demand erosion, while absorbing them directly impacts profitability. The market’s ability to sustain this price-led growth without a corresponding volume pickup is a critical analytical point.

Sectoral Divergence and Underlying Mechanisms

Sectoral performance during Q1 FY27 presented a varied picture, illustrating how different market structures respond to these macro pressures. Consumer-facing businesses, including the automotive, white goods, and telecom sectors, maintained relative stability, bolstered by steady domestic consumption and a strategic shift towards higher-value products within telecom.

Heavy industries such as steel and cement manufacturers also navigated cost pressures through strategic price hikes. Conversely, the construction sector experienced limited growth, estimated at a modest 1% to 3%, primarily due to project execution delays despite robust order books. This divergence underscores the importance of project pipeline conversion in addition to demand.

Export-oriented sectors like textiles and pharmaceuticals faced distinct headwinds, grappling with increased shipping costs and extended transit times. Although pharmaceutical companies achieved approximately 12% revenue growth driven by domestic launches, their overall profitability was constrained by logistical challenges and intense competition within the U.S. market.

The services sector also showed mixed results. The IT sector recorded a modest 5% revenue increase, largely attributable to favorable currency fluctuations rather than strong client demand, indicating a structural slowdown in new project acquisition. Meanwhile, the airline industry continued to struggle, witnessing declining profit margins due to high aviation turbine fuel costs and reduced passenger traffic.

In contrast, Non-Banking Financial Companies (NBFCs) demonstrated resilience, reporting improvements in both margins and asset quality. This suggests a more robust underlying financial structure in this segment. The sustainability of future corporate earnings across the board will hinge significantly on external factors, including the monsoon’s influence on rural demand and potential food inflation, along with the ability of companies to stimulate volume growth during the upcoming festive season.