India’s FY27 Growth: Tailwinds, Headwinds & Deloitte’s Forecast

By ThePip Desk

Deloitte forecasts India’s FY27 GDP growth at 6.5-6.8%, navigating global tensions, domestic inflation, and monetary policy. Discover key economic drivers.

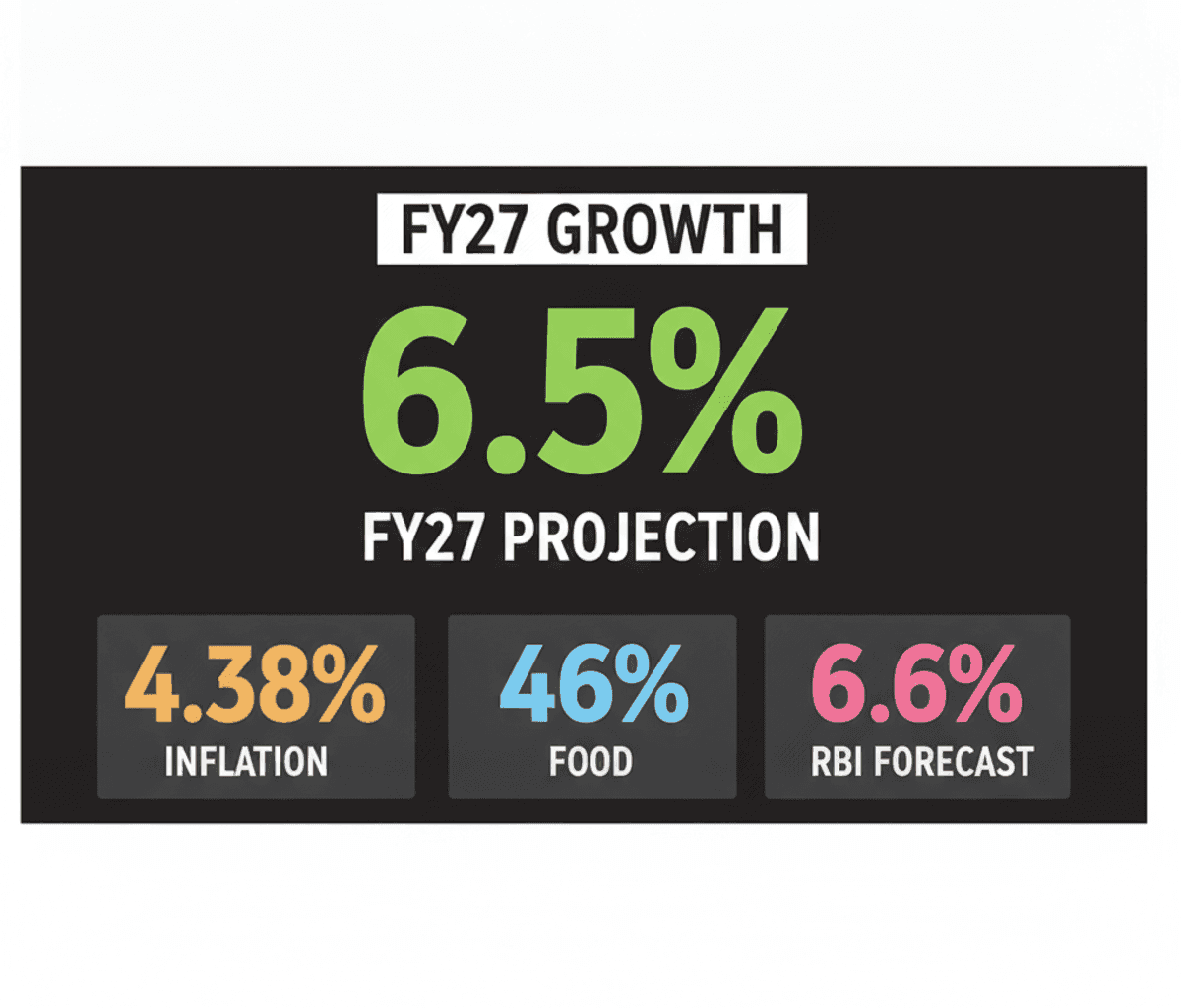

Deloitte India projects the nation’s Gross Domestic Product (GDP) growth will settle between 6.5% and 6.8% for the fiscal year 2026-27, a forecast predicated on a significant acceleration of economic activity in the latter half of the period. This anticipated momentum stems from a confluence of factors, including robust festive demand, potential shifts in monetary policy, and a broader stabilization of global economic conditions. This structural outlook suggests a carefully balanced trajectory for one of the world’s fastest-growing major economies.

The Interplay of Global Tensions and Domestic Economy

Global geopolitical conflicts, particularly the ongoing tensions in the Middle East, introduce a layer of external complexity. These disruptions extend beyond immediate regional impacts, causing significant volatility in commodity prices and undermining international investor confidence. For an import-dependent economy like India, this translates directly into a widening trade deficit and capital outflows, contributing to a weakening Indian rupee against the US dollar. The structural implication is higher import costs, which can fuel domestic inflationary pressures.

Inflationary Dynamics: The Food and Monsoon Nexus

The domestic inflation landscape presents another critical challenge. Retail inflation reached an 18-month peak of 4.38% in June, primarily driven by increases in food and fuel costs. The structural vulnerability here lies in India’s consumption basket: food items constitute nearly 46% of the Consumer Price Index (CPI). This high weighting means that agricultural output disruptions, such as those potentially caused by an El Nino event impacting monsoon patterns, directly threaten household budgets and consumption, thereby limiting the central bank’s room for monetary policy maneuver.

Navigating Growth Amidst Policy Constraints

The Reserve Bank of India (RBI) has already adjusted its growth forecast for the current fiscal year downward to 6.6% from an earlier 6.9%, following a strong 7.7% growth in FY 2025-26. Policymakers face the intricate task of managing persistent inflation without resorting to subsidies that could strain government finances. This represents a classic policy trade-off, where short-term relief measures risk long-term fiscal health. The structural challenge is to achieve price stability while fostering sustainable growth, a balance that requires continuous vigilance over inflation data and monsoon reports, as these metrics will directly influence economic activity and corporate earnings.

Understanding these interwoven structural patterns — global supply chain vulnerabilities, domestic consumption dynamics, and the central bank’s policy balancing act — is crucial for anticipating India’s economic trajectory. The path to 6.5-6.8% growth in FY27 is not merely a numerical projection but a complex interplay of these fundamental forces, requiring investors and policymakers alike to look beyond headline figures into the underlying mechanisms driving the economy.