India Exports: Value Up, Volume Down – What’s Hidden?

By ThePip Desk

India’s export value growth masks a concerning volume contraction, driven by petroleum surges while electronics and agriculture face structural challenges.

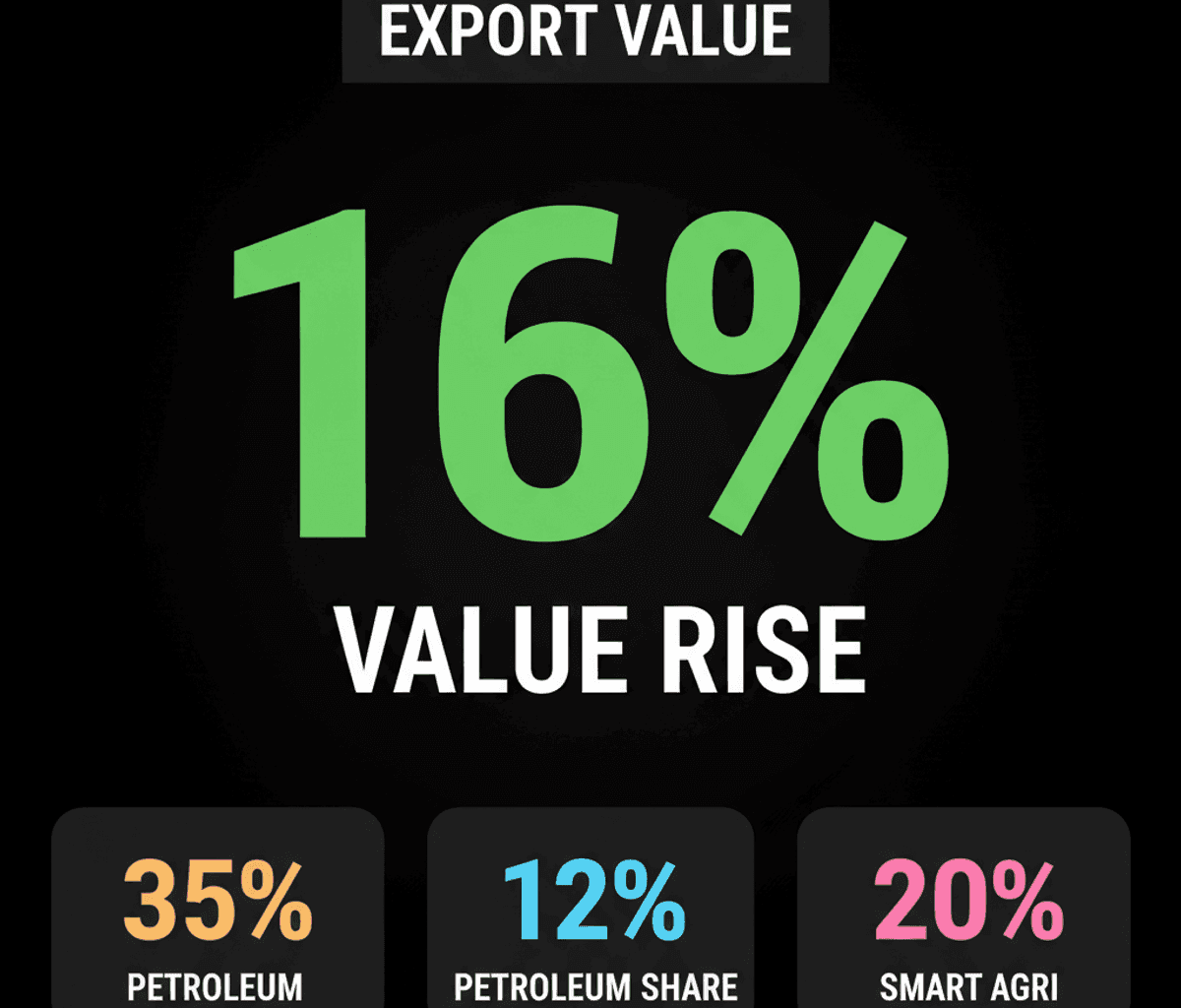

India’s export sector presents a fascinating study in economic optics: a 16% increase in export value during the first quarter of this fiscal year belies a more concerning underlying trend of volume contraction. This divergence is primarily driven by a significant 35% surge in petroleum product exports, which constitute approximately 12% of India’s total merchandise exports. The critical analytical point here is that this value growth is fundamentally susceptible to global crude oil price fluctuations, rather than reflecting a genuine increase in the volume of goods traded. As oil prices stabilize or decline, this transient driver is poised to recede, exposing the lack of organic volume expansion across other sectors.

The structural vulnerability becomes clearer when examining two crucial export categories: smartphones and agriculture, which together account for over 20% of India’s total export basket. Smartphones, despite becoming India’s leading export category aided by government production incentives, face an impending slowdown. This is due to ‘chipflation’—the rising cost of key components like memory chips—which translates into higher final device prices for consumers and, consequently, reduced global demand for electronic goods, a sector comprising about 11% of India’s merchandise exports.

Concurrently, the agricultural sector is navigating significant internal and external pressures. Domestic output faces uncertainty from adverse climate patterns, including a weak monsoon and the looming impact of El Niño conditions on crop yields. Major agricultural export items such as basmati rice, spices, and sugar have already reported a sluggish start to the current fiscal year. This dual pressure on electronics and agriculture signals a broader structural challenge to India’s national trade momentum.

Beyond these sector-specific issues, external macroeconomic factors are further compounding the challenges. Global economic growth forecasts have been downgraded, partly attributed to persistent supply chain disruptions exacerbated by geopolitical instability in West Asia. This global slowdown directly translates into decreased demand for Indian goods from key trading partners. Furthermore, Indian exporters contend with an evolving and often challenging trade policy landscape, exemplified by the European Commission’s adjustments to tariff-free steel import quotas and ongoing uncertainty regarding potential changes to United States trade tariffs. These policy shifts directly impact the cost-competitiveness of Indian products in international markets, adding another layer to the structural headwinds.

While the government’s pursuit of Free Trade Agreements (FTAs) with major global importers represents a long-term strategic response to improve market access and reduce tariffs, it remains to be seen how effectively these agreements can counteract the immediate structural slowdown in global demand. The fundamental challenge for exporters is to leverage these new opportunities to enhance their competitive position, even as the global economic environment and specific sector dynamics present significant obstacles to genuine volume growth.