India’s AI Edge: Powering Global Data Centers, Not Models

By ThePip Desk

A Shriram Mutual Fund report highlights India’s AI potential in powering global data centers, identifying electricity as the critical bottleneck for AI infrastructure growth.

India’s most significant contribution to the global artificial intelligence revolution may not stem from developing advanced AI models, but rather from supplying the foundational electricity and physical infrastructure required to power the world’s burgeoning AI data centers. This structural insight comes from a recent report by Shriram Mutual Fund, titled “The AI Bubble Debate: A Unit-Economics Lens,” which reframes the AI investment cycle as fundamentally a “power-demand story.”

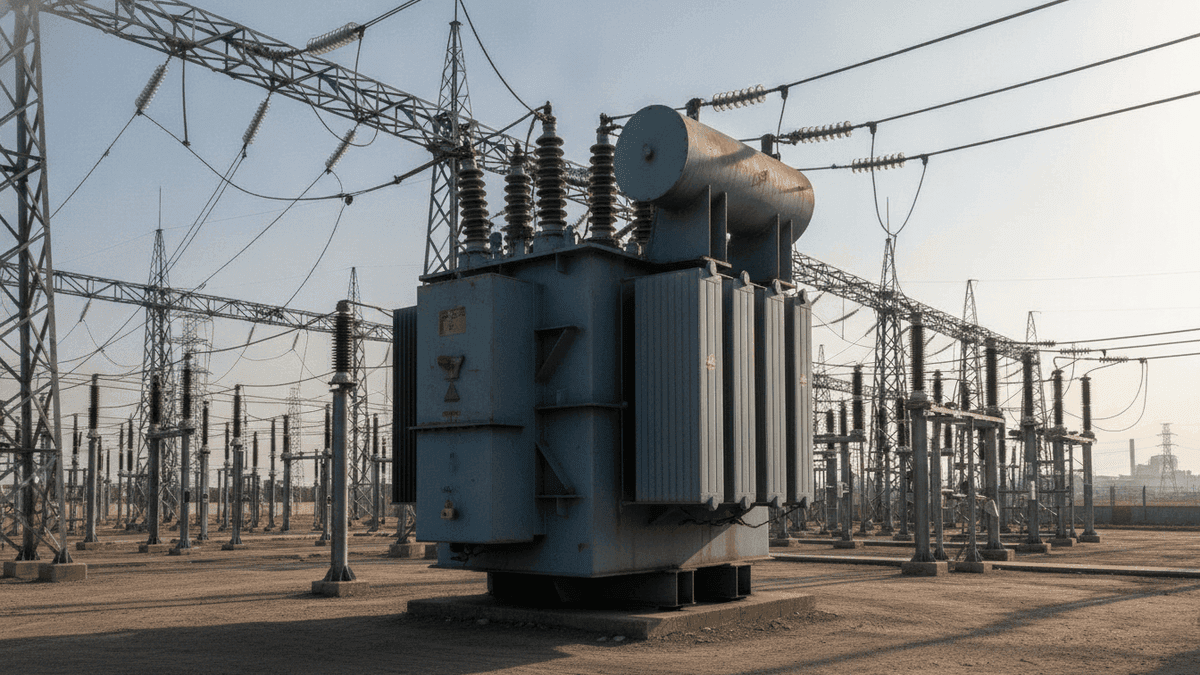

The report underscores a critical first-principles challenge: electricity has emerged as the foremost bottleneck in the expansive growth of global AI infrastructure. While billions are being channeled into sophisticated AI chips and data centers, the persistent and immense demand for electrical power is often overlooked. To put this into perspective, a single AI-grade gigawatt facility requires as much power as approximately 750,000 homes, illustrating the sheer scale of energy consumption inherent in advanced AI operations.

This dynamic positions India strategically within the global AI landscape, allowing it to leverage a classic “picks and shovels” framework. Rather than competing directly in the highly specialized and capital-intensive frontier of AI model development, where India currently lacks a listed frontier AI laboratory or hyperscale cloud company, the nation can become an indispensable supplier of the underlying utility. This includes essential components such as switchgear, transformers, robust grid infrastructure, advanced cooling systems, and specialized cables, all of which are non-negotiable for any large-scale AI data center.

In alignment with this analytical position, Shriram Mutual Fund has declared an overweight stance on India’s power sector. This encompasses a broad spectrum of companies involved across the value chain, including those in power generation, transmission, engineering, procurement, and construction (EPC), as well as associated financing entities and manufacturing firms producing power-related equipment.

Addressing the pervasive concerns about an “AI investment bubble,” the report shifts the analytical lens from mere investment size to unit economics and return on capital. It argues that the critical question is not the volume of investment, but whether AI companies can generate sufficient revenue from their deployed infrastructure before technological advancements render it obsolete. Unlike previous tech booms that often relied on speculative external funding, current AI spending is largely self-funded by highly profitable technology companies, transforming the debate into one of capital efficiency rather than solvency risk.

Ultimately, India’s opportunity in AI is less about pioneering the next ChatGPT and more about enabling the global computational backbone. By focusing on the structural demand for reliable, scalable power and the physical components that constitute the digital grid, India can secure a pivotal and durable role in the ongoing AI revolution, capitalizing on an indispensable input rather than the volatile output of AI innovation itself.