Geopolitical Fragmentation Cuts Global GDP Growth

By ThePip Desk

WEF report: Geopolitical shifts and financial fragmentation are structurally reducing global GDP growth by billions and increasing inflation. Learn about the ‘Neutral’ nation impact.

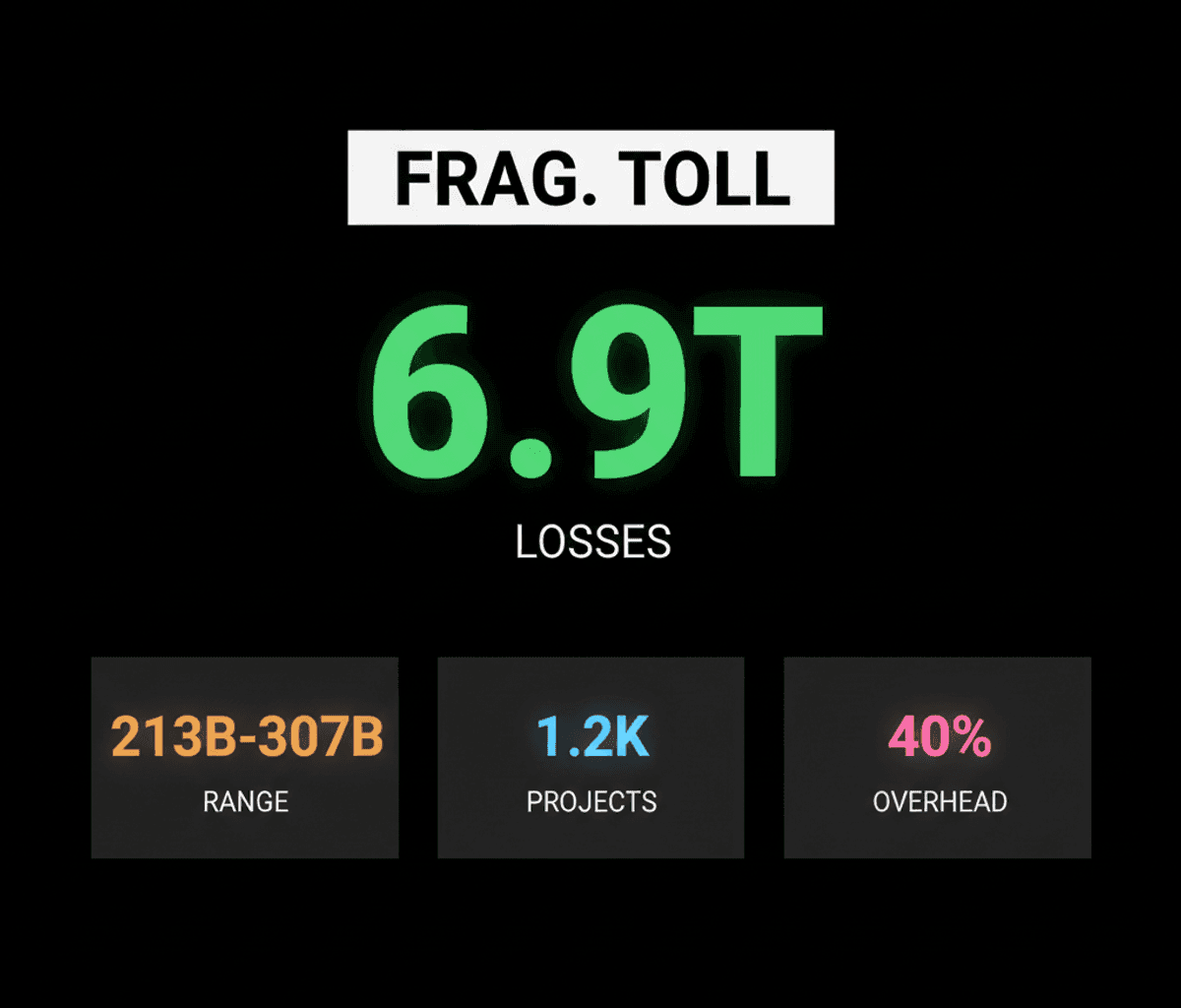

Financial fragmentation, exacerbated by persistent geopolitical turmoil, is currently extracting a significant toll on global economic output. A recent report from the World Economic Forum (WEF), developed in collaboration with Oliver Wyman, reveals that this structural shift is already diminishing global GDP growth by an estimated US$213 billion to US$307 billion. This economic drag is not merely a cyclical downturn; it represents a fundamental reordering of global trade and financial pathways, driven by what can be understood as an escalating era of economic statecraft.

Should the current trajectory of fragmentation intensify, the economic consequences could escalate dramatically. The report models a scenario where global economic output growth could face a 6.4% point reduction, leading to one-year losses potentially reaching US$6.9 trillion worldwide. This illustrates a critical framework: the costs associated with geopolitical friction are not linear but exponential, particularly as nations increasingly leverage economic tools to achieve strategic objectives.

A salient insight from the research is the disproportionate impact on countries categorized as ‘Neutral.’ Nations such as Brazil, India, Indonesia, Mexico, Taiwan, and Turkey are identified as particularly vulnerable. In a scenario where these countries are compelled to align with one of two fully fragmented blocs, they could collectively experience an aggregate hit of 10.7% points to their economic growth. This structural vulnerability arises because their diversified trade and financial relationships, once a source of resilience, become liabilities when global systems fracture, forcing difficult and costly re-alignments over approximately five years.

Beyond the direct impact on GDP, financial fragmentation is also a significant driver of inflationary pressures. The present level of fragmentation is estimated to contribute 0.2-0.3% points to global inflation. Under a more severe fragmentation scenario, this figure could surge by as much as 6.1% points, affecting all economic blocs. This inflationary mechanism is a direct consequence of increased trade barriers, supply chain rerouting, and reduced global economic efficiency, all of which impose higher costs on production and distribution.

The report underscores a critical shift in the global policy environment observed between 2025 and 2026, characterized by an unprecedented intertwining of finance, trade, and economic policies. Countries are increasingly implementing unanticipated barriers, elevating risks for businesses and nations. Historic examples cited include the US imposition of tariffs to reduce bilateral deficits, which triggered retaliatory measures from China, resulting in tariffs that at one point exceeded 100% between the two economic giants. China further demonstrated this trend through export controls on rare earths and tightened rules for its companies listing in the US.

To navigate these escalating risks, the WEF and Oliver Wyman report offers several strategic recommendations for policymakers. A key principle involves operationalizing guardrails to minimize the unintended consequences of economic statecraft, advocating for alignment on common principles through multilateral forums like the G20. Furthermore, maintaining the interoperability of underlying payment rails is deemed crucial. This includes promoting common standards such as ISO 20022, advancing the G20 Roadmap for Enhancing Cross-Border Payments, and establishing a global regulatory framework for digital assets. The analysis also acknowledges the continued dominance of the US dollar, alongside the growing influence of currencies like the renminbi and the complexities introduced by digital finance, including stablecoins, as features of this evolving financial landscape.

The durable takeaway from this analysis is that geopolitical fragmentation is not a temporary disruption but a structural force reshaping the global economic order. While firms will adapt through supply chain adjustments, the initial and ongoing costs are substantial, particularly for those nations seeking to maintain neutrality. Understanding these underlying mechanisms of economic statecraft and its ripple effects on trade, finance, and inflation is paramount for navigating the complexities of the years ahead.