Flagship Killer Smartphone Market Squeeze

By ThePip Desk

Explore the structural challenges facing ‘flagship killer’ smartphone brands like OnePlus in mature markets, as rising costs erode their value proposition.

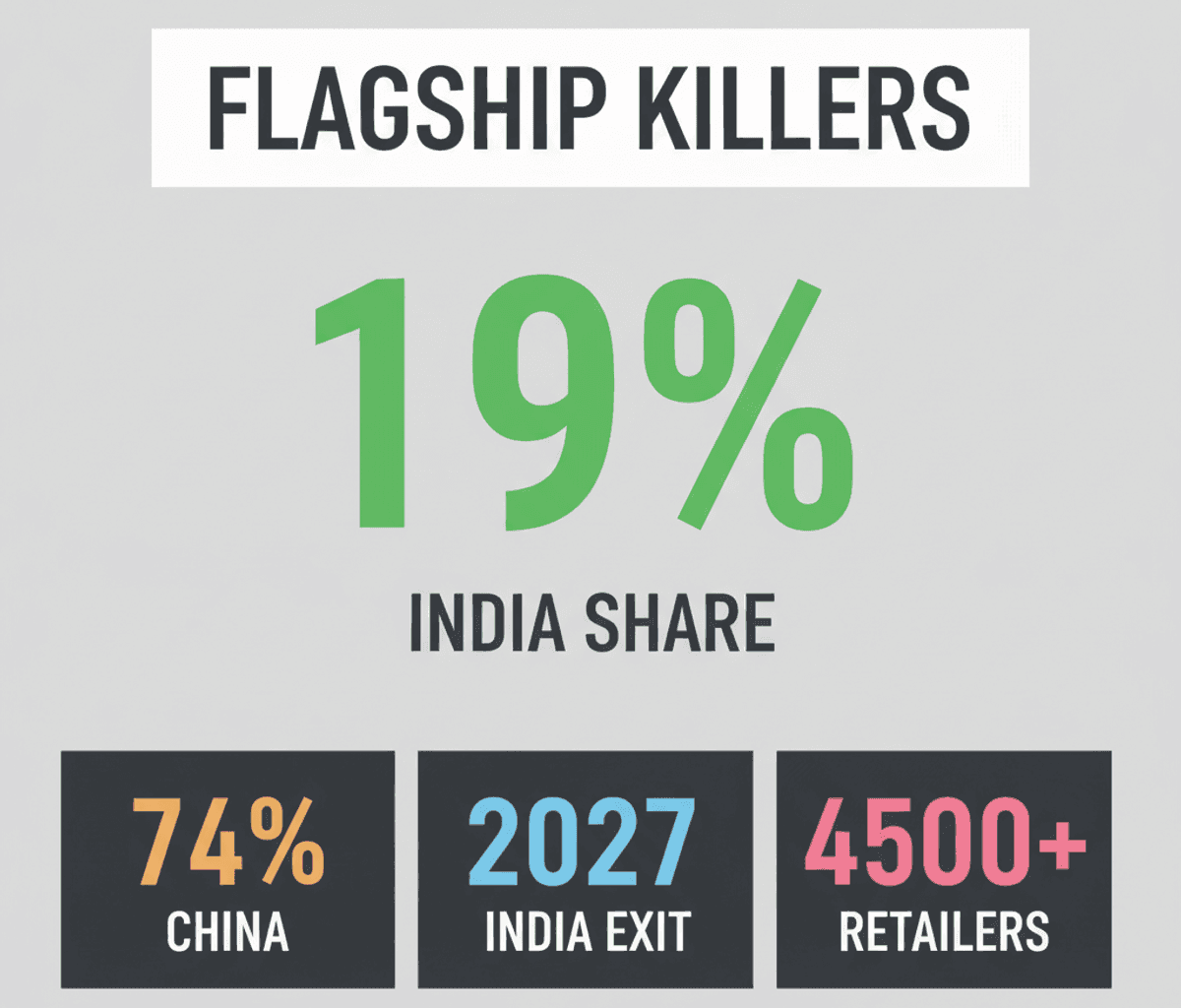

The recent rumors surrounding OnePlus, a Chinese smartphone manufacturer, contemplating an exit from European and US markets, alongside potential withdrawal from India by 2027, underscore a critical structural challenge for brands that once thrived on disrupting the premium segment. While its parent company, Oppo, conducts a global restructuring, and OnePlus itself denies these speculations, the underlying data reveals a pattern of market consolidation and value proposition erosion that merits deeper analysis.

At its core, the smartphone market has matured significantly, shifting from an innovation-driven growth phase to a margin-sensitive, intensely competitive landscape. Brands that initially carved out niches by offering high-end specifications at accessible prices, often termed ‘flagship killers,’ now face immense pressure from escalating component costs. This dynamic makes their original value proposition increasingly difficult to sustain, forcing strategic recalibrations that often involve geographic consolidation and a re-evaluation of product differentiation.

The Framework of Erosion: Cost, Competition, and Concentration

OnePlus’s current predicament illustrates a clear framework of value proposition erosion, driven by both external market forces and internal strategic shifts. The company’s global business has become overwhelmingly reliant on its home market, China, which accounted for a dominant 74% of its global smartphone shipments in the first quarter of 2026, according to industry analysts. This marks a stark contrast to its previous global spread, with India’s share plummeting from 30% to 19% and the US market effectively disappearing during the same period.

This shift isn’t merely a preference but a response to structural economic realities. Tarun Pathak of Counterpoint Research notes that the ‘flagship killer’ era for brands like OnePlus is effectively over, primarily due to a sharp increase in memory chip prices. This external cost pressure directly impacts the ability to deliver premium hardware at competitive prices, eroding the core differentiator. Furthermore, within the broader Oppo ecosystem, creating unique innovation becomes challenging, as Faisal Kawoosa of TechARC points out, leading to internal competition that can dilute a brand’s distinct identity.

The impact of internal strategy is also evident. OnePlus’s 2021 merger of its OxygenOS with Oppo’s ColorOS, intended for synergy, instead led to significant user complaints regarding software bugs and performance. This eroded trust in a brand that once prided itself on a clean, high-performance Android experience. Furthermore, in 2024, over 4,500 mobile retailers in South and West India reportedly ceased selling OnePlus phones, citing low profit margins and inadequate after-sales support – a clear indication of channel friction and a deteriorating partner ecosystem.

The Path Forward: Re-establishing Differentiated Value

While OnePlus maintains its operations are normal, and indeed, a company’s denial of exit rumors is a common initial response, the analytical consensus points to a challenging road. Prabhu Ram of CyberMedia Research observed that the company’s pivot to the Nord series, an attempt to capture volume in the mid-range, did not achieve expected scale, further highlighting the difficulty in adapting to a mature market without a clear, sustainable competitive advantage.

What many observers might misinterpret is that these challenges are not solely about product features or marketing spend. They reflect deeper structural patterns in the technology sector: the lifecycle of disruptive brands, the relentless pressure of component economics, and the complexities of managing multiple brands within a single corporate umbrella in a consolidating market. Simply put, sustained differentiation in a mature sector requires more than just aggressive pricing; it demands a resilient value proposition that can withstand cost fluctuations and intense competition.

For the reader, this situation underscores a vital principle: the success of a technology brand is rarely static. It is a continuous negotiation between innovation, cost structure, market demand, and strategic execution. Understanding these underlying mechanisms allows for a more nuanced interpretation of market shifts, moving beyond mere event tracking to grasp the structural forces that shape industry outcomes. The long-term perspective suggests that only brands capable of consistently re-inventing their core value proposition or establishing defensible moats — be they technological, brand-based, or ecosystem-driven — will thrive in an increasingly crowded and cost-sensitive global smartphone market.