China VCI Resin Market: Growth & Challenges Analysis

By ThePip Desk

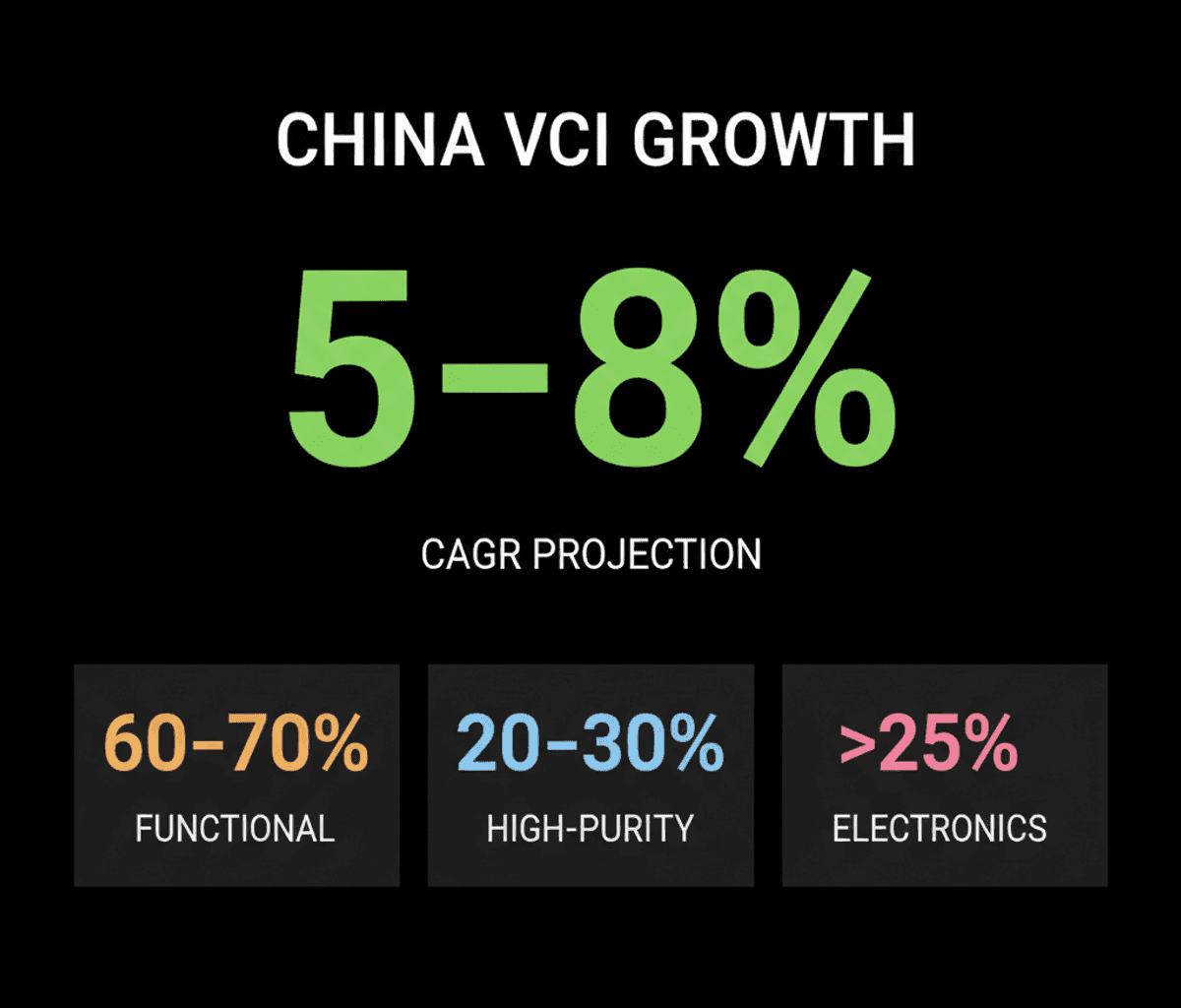

China’s VCI Resin market to grow 5-8% CAGR by 2035, driven by electronics. Analysis covers demand, structural shifts, and supply chain challenges.

The market for VCI Resin in China is poised for substantial expansion, with projections indicating a compound annual growth rate (CAGR) of 5–8% from 2026 to 2035, according to IndexBox data. This growth trajectory is fundamentally driven by two macro-level forces: the escalating demand for industrial packaging across diverse sectors and the sustained expansion of China’s electronics manufacturing base. VCI Resin, a critical intermediate for vapor-phase corrosion protection, finds China not only as a dominant global producer but also its most significant end-user.

Understanding the Market Mechanism

The demand for VCI Resin is concentrated within key industrial verticals, including electronics, automotive, precision engineering, metalworking, and general industrial packaging. A critical structural shift observed is the increasing emphasis on water-based and low-VOC (Volatile Organic Compound) formulations, a direct consequence of evolving regulatory pressures within China. Concurrently, electronics manufacturers are driving a demand for high-purity, chlorine-free grades, reflecting a broader trend towards specialized material requirements in advanced manufacturing. Suppliers are responding by offering value-added services, such as multi-layer film lamination and bespoke vapor-phase corrosion testing, enhancing the utility and application-specific performance of VCI solutions.

Despite this clear growth vector, the market contends with several structural impediments. Feedstock price volatility, particularly for key inputs like ethylene and vinyl acetate, presents a recurring challenge, causing year-over-year input cost swings of 15–30%. This directly compresses margins for producers of standard-grade VCI Resin. Furthermore, quality inconsistencies among smaller domestic producers pose a barrier to entry into highly regulated sectors such as medical devices and aerospace. The reliance on imports for high-purity and specialty VCI Resin also introduces supply chain vulnerabilities, manifest in long lead times that can disrupt production and inflate inventory costs for end-users.

Segmentation and Value Dynamics

The China VCI Resin market is distinctly segmented by functional characteristics, each commanding different unit economics. Functional grades represent the largest segment, accounting for 60–70% of total volume, with pricing typically ranging from $3–5 per kilogram. High-purity grades, while comprising 20–30% of volume, are the fastest-growing segment and command higher prices of $6–10 per kilogram. Specialty formulations, though only 10–20% of volume, achieve the highest unit values, often exceeding $12 per kilogram. Raw material costs constitute a significant portion of the production expense for standard grades, typically falling between 55% and 70%.

In terms of end-use, metalworking and parts packaging remains the largest application, absorbing 40–45% of the market. However, the electronics and precision equipment sector is projected to be the primary growth engine, with its share expected to rise from 20% to over 25% by 2035. This shift underscores the increasing sophistication of China’s industrial base and the expanding need for advanced corrosion protection in high-value components.

Supply Landscape and Strategic Opportunities

The supply side is moderately fragmented, characterized by 15–20 core domestic producers contributing 70–80% of total output, complemented by numerous smaller regional blenders. International players, including Japanese giants like Mitsubishi Chemical and Asahi Kasei, and German chemical leaders such as BASF and Chemetall, predominantly control the specialty and certified-grade segments. China acts as a net importer of these advanced VCI Resins, primarily from Japan, Germany, and the United States, while simultaneously exporting standard functional grades to Southeast Asia, India, and the Middle East.

Distribution channels are multifaceted, encompassing direct sales to large converters, specialized chemical distributors, and a growing presence of online B2B marketplaces. Regulatory compliance, notably China REACH and GB/T 19532-2015 standards, is a non-negotiable factor, with increasing pressure to reduce VOC emissions dictating product development. Strategic opportunities for growth lie in domestic substitution for imported high-purity grades, the development of ‘smart’ or tunable VCI Resin formulations, integration into circular economy packaging initiatives, and the continued expansion of Chinese standard grades into export markets. The market’s future, while moderately paced, is expected to be profitable, favoring suppliers who prioritize quality, innovation, and regulatory adherence.