Austria Calibrator Market: Import Reliance, Growth & Challenges

By ThePip Desk

Austria’s process calibrators market, 80-95% import-dependent, forecasts 3-6% CAGR (2026-2035) driven by automation, pharma, and energy sectors, despite headwinds.

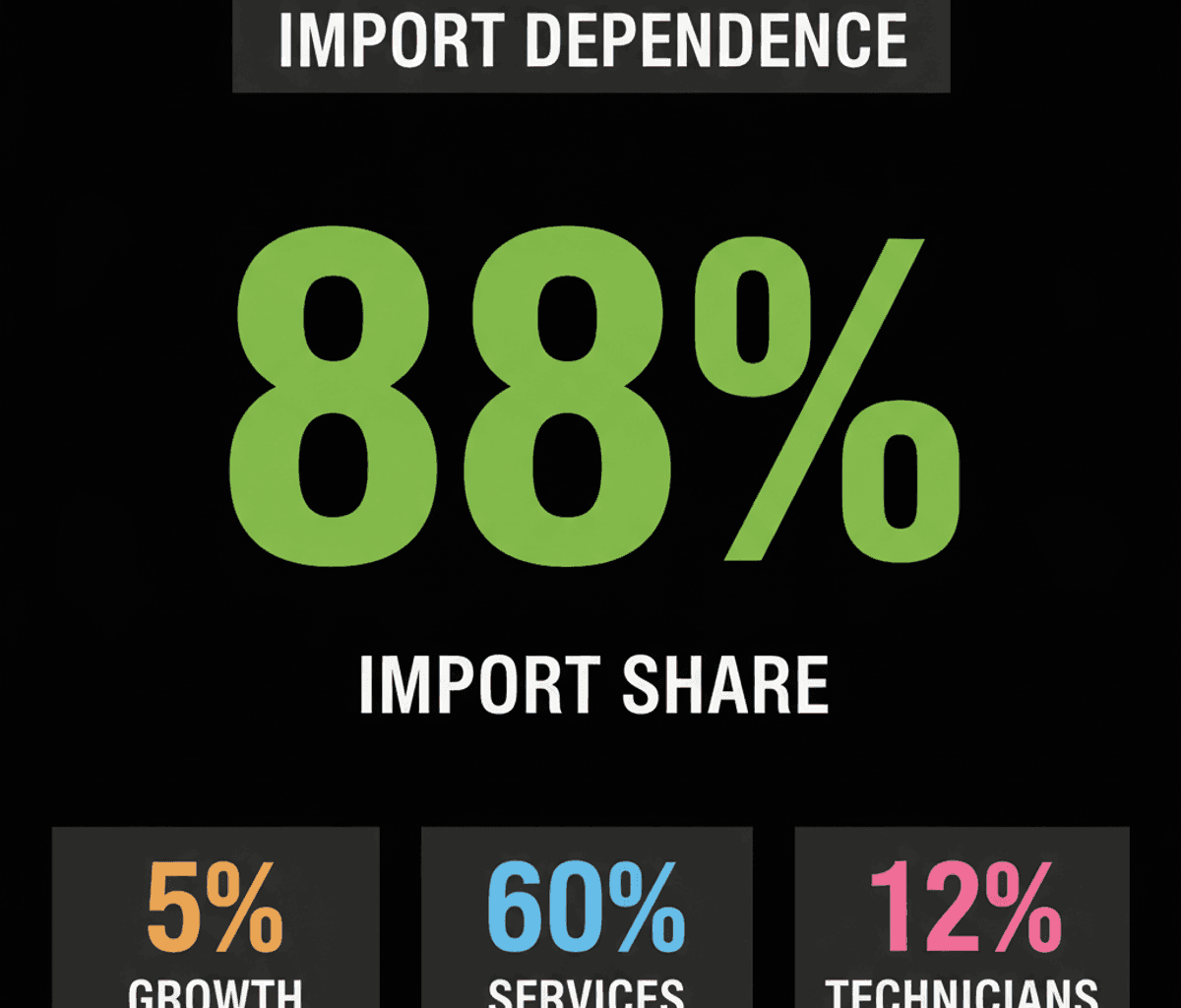

Austria’s process calibrators market fundamentally operates as a demand-driven ecosystem, uniquely characterized by its heavy reliance on external supply. An estimated 80-95% of the equipment, crucial for industrial instrumentation, is sourced from international manufacturers, primarily in Germany, Switzerland, the United States, and the United Kingdom, according to IndexBox data. Domestic activities within Austria are largely confined to calibration services and distribution, with minimal local manufacturing presence.

This market structure sets the stage for a projected compound annual growth rate (CAGR) of 3-6% in nominal euro terms between 2026 and 2035. The expansion is underpinned by persistent replacement cycles in process automation, stringent quality compliance demands from the pharmaceutical sector, and ongoing instrumentation upgrades within the energy industry. Annual end-user expenditure on calibration hardware, accredited services, and aftermarket support is substantial, ranging from €22 million to €38 million, with services alone constituting a significant 55-65% of this total spend.

Evolving Market Dynamics and Adoption Trends

Several key trends are reshaping this import-dependent landscape. There is an accelerated adoption of multifunctional documenting calibrators, which incorporate advanced communication protocols like HART, Foundation Fieldbus, and wireless connectivity. This shift is particularly pronounced in Austrian pharmaceutical and chemical plants, indicating a broader move towards integrated and efficient process management. Concurrently, a growing preference for third-party accredited calibration services over in-house options has emerged, with service contracts now accounting for approximately half of annual calibration-related expenses. Furthermore, the distribution paradigm is evolving through the increased use of digital procurement platforms and vendor-managed calibration programs, streamlining the supply chain.

The market is segmented by product type, application, and end-use sector, illustrating distinct demand patterns. Single-function pressure and temperature calibrators represent 30-40% of the unit volume, while the more advanced multifunction documenting calibrators contribute 25-35% and are experiencing robust growth at 5-8% annually. From an application perspective, industrial automation and instrumentation command the largest share of demand at 40-50%, followed by the pharmaceutical and life sciences sector at 20-30%, and the energy sector at 15-20%.

Structural Challenges and Cost Pressures

Despite the projected growth, the Austrian process calibrators market faces inherent structural challenges that pressure distributor margins and operational efficiency. Input cost volatility for precision components, coupled with exposure to euro exchange rate fluctuations, creates a complex environment for pricing and profitability. The stringent qualification and documentation requirements, particularly for equipment used in GMP-regulated pharmaceutical and medical-device production, lead to extended and intricate procurement cycles, adding to operational overheads.

A critical long-term challenge is the escalating shortage of skilled calibration technicians within Austria. IndexBox estimates a 10-15% decline in accredited metrology specialists over the past decade, directly contributing to increased service costs and longer lead times. This labor constraint, alongside the inherent import dependency, creates a bottleneck that could temper the efficiency gains from technological adoption. Pricing for calibrators varies significantly, from €1,800-€4,500 for standard handheld units to over €6,000-€14,000 for premium multifunction instruments, with costs driven by precision components, currency effects, and certification. Global manufacturers such as Fluke (including Beamex), Wika, Endress+Hauser, and Siemens dominate the competitive landscape, primarily differentiating on specification and service capability.

The Long-Term View on Industrial Instrumentation

The Austrian process calibrators market serves as a compelling case study in how a specialized industrial sector, despite robust demand drivers and technological advancements, can be profoundly shaped by structural dependencies and internal labor market dynamics. The persistent reliance on imports means that global supply chain stability and currency movements are not merely external factors, but fundamental determinants of local market health. While the shift towards advanced, multifunctional calibrators and outsourced services indicates a maturation in operational strategy, the increasing scarcity of skilled technicians represents a significant counter-force, potentially creating a long-term drag on service capacity and cost efficiency. Understanding this interplay between demand, technology, and structural constraints is crucial for anticipating the future trajectory of such specialized industrial instrumentation markets.