Australia’s Analytical Sensor Market: Growth & Import Reliance

By ThePip Desk

Explore Australia’s growing analytical sensor market, driven by B2B demand and structural import dependence. Insights into market value, CAGR, and key drivers.

Australia’s analytical sensor market, a critical yet specialized segment within the broader industrial technology landscape, is experiencing significant growth, even as its structure is defined by an overwhelming dependence on global imports. Valued between AUD 250 million and AUD 400 million as of 2026, this B2B domain, crucial for manufacturing, environmental monitoring, water treatment, and pharmaceutical production, has expanded at a compound annual growth rate (CAGR) of 4-6% over the past five years, with an acceleration noted since 2023, driven by investments in mineral processing and water infrastructure.

Understanding this market requires a first-principles approach to its operational mechanics. Analytical sensors, which precisely measure chemical or physical properties like pH, conductivity, and gas composition, are not discretionary components; they are foundational to process control and quality assurance across diverse industrial applications. Their function is to provide real-time data essential for operational efficiency, regulatory compliance, and product integrity. The inherent criticality of these instruments means that demand is largely inelastic, tied directly to capital expenditure cycles in core industries and the ongoing need for maintenance and replacement.

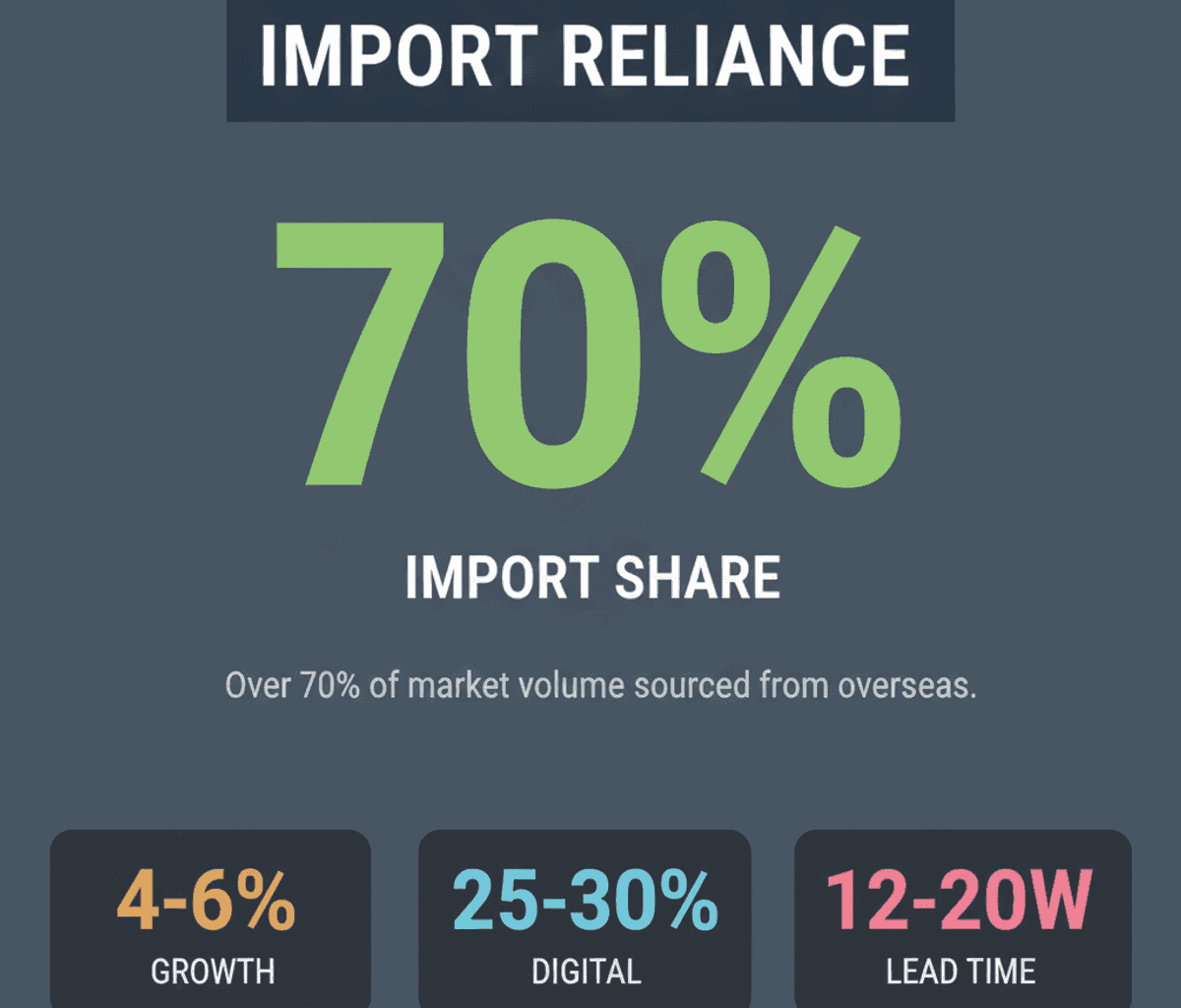

The Framework of Structural Import Dependence

The defining characteristic of the Australian analytical sensor market is its profound structural import dependence. Over 70% of the market’s volume is sourced from overseas, primarily from Europe, the United States, and the Asia-Pacific region. This reliance is not merely a preference but a structural reality, evidenced by Australian manufacturers holding less than a 5% market share. This framework of deep import reliance shapes virtually every aspect of market dynamics, from pricing and supply chain resilience to the nature of competitive advantage.

This structural reality introduces specific operational complexities and costs. Lead times for specialized components frequently extend from 12 to 20 weeks, creating planning challenges for end-users. Furthermore, additional procurement costs, ranging from 5-10%, are incurred due to stringent documentation and certification requirements for imported goods, alongside import logistics adding another 8-12% to the cost base. These factors, combined with currency fluctuations, contribute to the pricing variability, where standard units range from AUD 150-600, while premium sensors can command AUD 900-3,500 or more.

Demand Dynamics and Technological Evolution

The market’s growth is underpinned by robust B2B demand, with industrial automation and process control applications accounting for 55-60% of total demand. This segment is directly correlated with capital expenditure in vital sectors such as mining, water utilities, and food-and-beverage processing. Concurrently, replacement and lifecycle maintenance represent 40-45% of the annual market value, a consistent demand driver stemming from sensor fatigue and evolving compliance requirements, underscoring the non-discretionary nature of these components.

Technological trends are further shaping this landscape. The market is witnessing a notable shift towards digital, smart analytical sensors, which now constitute 25-30% of new installations. These advanced sensors integrate diagnostics and IoT connectivity, facilitating predictive maintenance and enhanced data analytics. End-users are increasingly consolidating their supplier lists, favoring vendors capable of offering comprehensive sensor-to-software solutions coupled with robust local technical support, reflecting a broader industry trend towards integrated systems and reduced vendor complexity.

Growth Drivers and Sectoral Disparities

The market’s forecasted growth of 4-6% CAGR in real value terms through 2035 is primarily driven by ongoing investments in water infrastructure, major resource projects, and the accelerating adoption of digital sensor networks. However, this growth is not uniform across sectors. Resources and energy account for a significant 35-40% of demand, reflecting Australia’s strong natural resources sector. Water and wastewater treatment shows a steady annual growth of 5-7%, while laboratory and research demand expands at 6-8% annually. Emerging adoption in non-traditional sectors like renewable energy hydrogen production and advanced environmental monitoring is also growing at a low-teens CAGR, signaling diversification.

In terms of sensor types, electrochemical sensors remain the most deployed, representing 40% of the market, essential for parameters like pH and dissolved oxygen. Optical sensors follow at 25%, crucial for advanced environmental monitoring and process control, with conductivity/resistivity sensors making up 15%.

The Competitive Landscape and Counter-Thesis

The competitive landscape is dominated by multinational companies such as Endress+Hauser, ABB, Honeywell, and Yokogawa, which primarily operate through established local distribution partners. This structure reinforces the import-dependent nature of the market, as these global players leverage their scale and technological prowess to serve Australian demand. While this might suggest a limited role for domestic entities, the counter-thesis is that this very structure creates significant opportunities for specialized local value creation.

The argument that local players are merely distributors overlooks their critical function in integration, after-sales service, and technical support. These domestic partners are indispensable for navigating the complexities of local regulations, providing timely calibration, and offering field-service expertise, particularly in Australia’s remote areas where a shortage of qualified technicians is a noted challenge. Their role shifts from manufacturing to the crucial last mile of value delivery, ensuring optimal performance and compliance for the end-user.

What Most People Overlook: The Shift in Value Creation

A common misconception in markets characterized by high import dependence is that domestic opportunities are inherently limited. However, in the Australian analytical sensor market, the value chain fundamentally shifts. Instead of competing on sensor manufacturing, the true leverage and growth opportunities lie in specialized services that complement the imported technology. This includes IIoT integration, which transforms raw sensor data into actionable intelligence, and sophisticated after-sales service and calibration, which are essential for maintaining accuracy and regulatory compliance over the sensors’ lifecycle.

Furthermore, the demand for high-sensitivity sensors, driven by increasingly stricter pollution regulations, presents a specific niche for local expertise in deployment and data interpretation. Collaboration with local research institutions also offers a pathway for domestic innovation, focusing on application-specific solutions that integrate global hardware with local environmental and industrial requirements. This redefines the competitive arena from product origination to intelligent deployment and ongoing support.

Implications for Market Participants: A Process-Level Perspective

For businesses engaged with or observing the Australian analytical sensor market, understanding these structural dynamics is paramount. It necessitates a strategic focus on value-added services, digital integration capabilities, and a robust approach to navigating complex global supply chains. Success in this market is less about developing proprietary sensor hardware and more about optimizing the delivery, integration, and lifecycle management of advanced analytical technologies. This involves investing in local technical expertise, developing comprehensive service offerings, and building strong partnerships with global manufacturers to bridge the import gap effectively.

The long-term perspective suggests that the market’s trajectory will remain intrinsically linked to Australia’s broader industrial and environmental investment cycles. Digital transformation, particularly through IIoT integration and smart sensor networks, offers a durable pathway for enhancing operational efficiency and driving growth. Even within a globally sourced framework, the demand for sophisticated local support and integration will continue to be a critical differentiator, ensuring that the market evolves towards greater intelligence and resilience.