Missed Home Loan EMI? Avoid Credit Damage & Stress

By Sivam

Missed a home loan EMI? Learn how to communicate with lenders and plan repayments to protect your credit score and manage financial stress effectively.

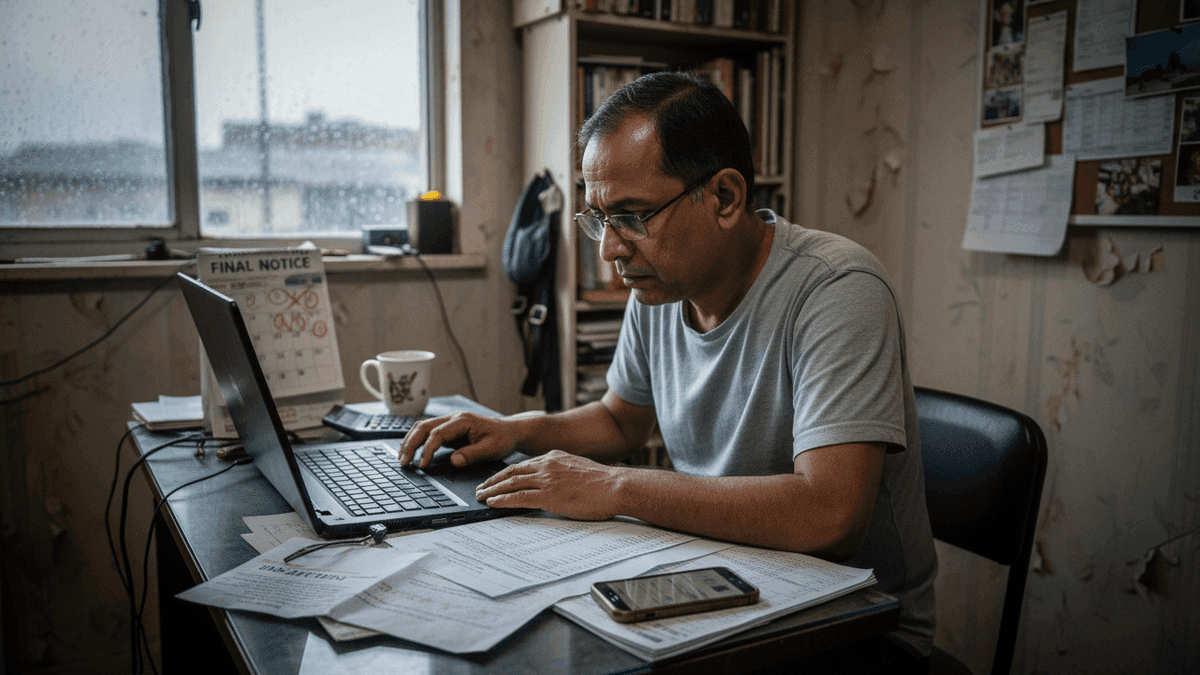

Missing a home loan EMI payment is a critical financial event that can initiate a cascade of negative consequences, significantly impacting an individual’s credit score and overall financial stability. The timely fulfillment of home loan obligations is paramount, not only for maintaining a healthy credit profile but also for ensuring long-term financial well-being. A single missed payment can trigger penalty charges, lower credit ratings, and complicate future borrowing endeavors, underscoring the necessity for a proactive and strategic approach when faced with such a challenge.

This situation demands immediate attention and a clear understanding of the repercussions, along with actionable steps to mitigate potential damage. Effective management involves a combination of transparent communication with lenders, meticulous repayment planning, and, where necessary, leveraging expert financial advice. Addressing a missed EMI is not merely about settling the overdue amount; it is about safeguarding one’s financial future and navigating periods of economic stress with informed decisions.

Understanding the Immediate Repercussions of a Missed Home Loan EMI

The moment a home loan EMI is missed, several critical financial mechanisms are set in motion, primarily affecting an individual’s credit score. Credit bureaus, such as CIBIL, Experian, and Equifax, record payment defaults, which can lead to a significant drop in one’s credit rating. This deterioration in the credit score is not merely a number; it represents a weakened financial standing that can jeopardize access to future credit facilities, including personal loans, credit cards, or even subsequent home loan applications, often resulting in higher interest rates or outright rejection.

Beyond the credit score impact, lenders impose late payment penalties and charges, which are typically added to the outstanding principal. These charges can accumulate rapidly, increasing the overall debt burden. Furthermore, a missed EMI signifies a breach of the loan agreement, potentially leading to the lender initiating a more aggressive recovery process if the default persists. Understanding these immediate repercussions is the first step towards formulating an effective damage control strategy and preventing a minor oversight from escalating into a major financial crisis.

The Critical Role of Proactive Communication with Financial Institutions

One of the most effective strategies for managing a missed home loan EMI is immediate and transparent communication with the lending institution. Many borrowers mistakenly avoid contact, fearing confrontation or negative outcomes. However, early engagement with the lender is crucial and often yields more favorable solutions. Financial institutions are typically open to discussing options with borrowers who proactively disclose their difficulties, especially if it is an isolated incident or due to unforeseen circumstances.

Initiating contact allows borrowers to explain their situation and explore potential remedies before the default becomes a more severe issue. Lenders may offer various solutions, such as a temporary grace period, a revised payment schedule, or even a short-term moratorium on EMIs. This proactive approach demonstrates accountability and a commitment to resolving the issue, which can significantly influence the lender’s willingness to provide support and prevent the situation from negatively impacting the borrower’s credit history.

Strategic Approaches to Loan Repayment and Restructuring

When faced with a missed EMI, a well-thought-out repayment plan is essential. Beyond merely paying the overdue amount, borrowers should explore strategic options that provide long-term relief and prevent future defaults. One common approach is to request an EMI deferment, where the lender allows a temporary pause in payments, often with the understanding that the outstanding amount will be adjusted over the remaining loan tenure or paid at the end of the deferment period. This can provide much-needed breathing room during temporary financial strain.

Another viable option is loan restructuring, which involves modifying the original loan terms. This could include extending the loan tenure to reduce the monthly EMI amount, adjusting interest rates, or consolidating multiple debts into a single, more manageable payment. While restructuring might increase the total interest paid over the loan’s lifetime, it can significantly alleviate immediate financial pressure and help borrowers regain control of their finances. Partial payments, even if not a full EMI, can also be a sign of good faith and help reduce the outstanding balance, demonstrating commitment to repayment.

Leveraging Expert Financial Advice for Crisis Management

Navigating the complexities of a missed home loan EMI and its potential impact on credit and financial stability can be challenging for individuals. This is where expert financial advice becomes invaluable. A qualified financial advisor can assess the borrower’s complete financial situation, identify the root causes of the missed payment, and develop a tailored recovery plan. These professionals can offer objective insights into available options, including debt consolidation, exploring alternative income sources, or negotiating more effectively with lenders.

Financial advisors can also help in understanding the intricate details of loan agreements, penalty clauses, and the long-term implications of various repayment strategies. Their expertise can provide clarity, reduce stress, and guide borrowers towards sustainable solutions that protect their assets and credit health. Engaging with a professional ensures that decisions are made based on sound financial principles rather than impulsive reactions to a stressful situation.

Building Long-Term Financial Resilience Against Future Shocks

Beyond addressing the immediate crisis of a missed EMI, it is imperative for borrowers to implement long-term strategies aimed at building financial resilience. A cornerstone of this approach is the establishment of a robust emergency fund. Ideally, this fund should cover at least three to six months of essential living expenses, including EMI payments. Such a fund acts as a critical buffer during unexpected financial setbacks, such as job loss, medical emergencies, or unforeseen expenses, preventing defaults.

Regularly reviewing insurance policies, particularly life and critical illness insurance, is also vital to ensure adequate coverage for loan liabilities in adverse circumstances. Furthermore, disciplined financial management, including meticulous budgeting, tracking expenses, and avoiding unnecessary debt, contributes significantly to overall financial stability. By proactively building these safeguards, individuals can minimize the risk of future EMI defaults and maintain a strong, healthy financial profile, ensuring peace of mind regarding their home loan commitments.