Lowest Gold Loan Rates India: Avoid Hidden Costs

By Sivam

Discover how to find the lowest gold loan interest rates in India. Learn about LTV, gold valuation, and hidden charges to secure the best deal.

When evaluating financial products, the interest rate frequently stands out as the primary metric for comparison. For gold loans in India, this initial focus is understandable, as a lower rate directly translates to reduced borrowing costs over the loan’s duration. However, securing the most advantageous gold loan interest rate in the Indian market demands a more nuanced approach than a simple online search. Interest rates are highly dynamic, varying significantly across different lenders, loan amounts, tenures, and repayment structures, meaning the advertised headline figure rarely aligns with the specific terms offered to an individual borrower. A comprehensive understanding of the underlying valuation methodologies, regulatory frameworks, and ancillary charges is paramount for making an informed decision in this competitive financial landscape.

Before diving into interest rate comparisons, prospective borrowers must first grasp how their gold collateral is assessed, as this valuation directly influences the maximum eligible loan amount and, consequently, the applicable interest rate tier. Lenders do not typically calculate the loan amount based on the live, real-time market price of gold, which is subject to daily volatility. Instead, institutions like Bajaj Finance employ a more conservative and regulated approach. They reference either the previous day’s closing price or the 30-day average closing price, as published by the India Bullion and Jewellers Association (IBJA) or a SEBI-regulated commodity exchange. This method is designed to mitigate risks associated with daily price fluctuations, ensuring that the loan is not based on potentially transient market highs. Consequently, the actual loan amount a borrower qualifies for might be marginally lower than what the immediate market price of their gold might suggest, a crucial detail for setting realistic financial expectations.

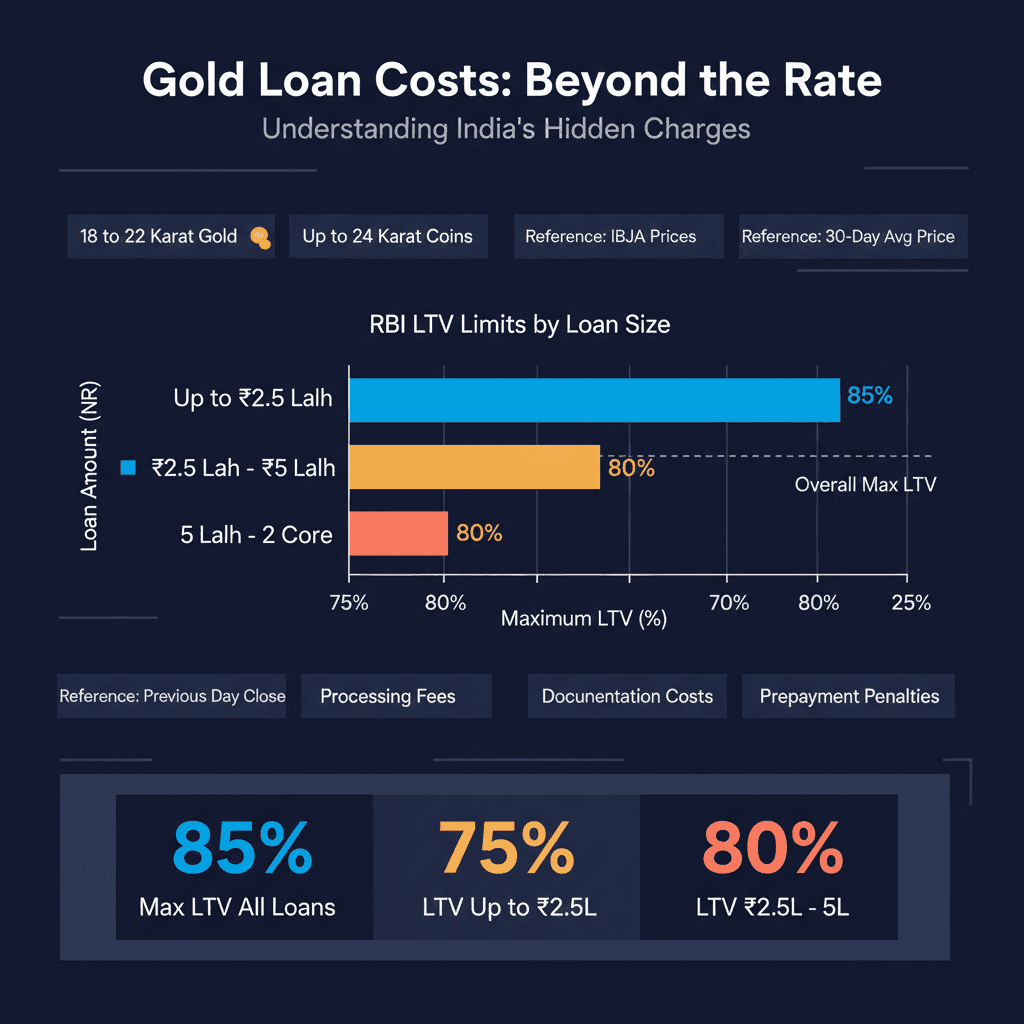

Understanding RBI’s Loan-to-Value (LTV) Regulations

The Reserve Bank of India (RBI), as the primary financial regulator, imposes stringent Loan-to-Value (LTV) limits on all regulated lenders offering gold loans. These limits dictate the maximum percentage of the gold’s assessed value that can be disbursed as a loan, varying based on the loan amount itself. For consumption loans up to Rs 2.5 lakh, the maximum LTV is capped at 75%. This percentage incrementally rises for larger loan sums, reaching 80% for loans ranging between Rs 2.5 lakh and Rs 5 lakh. For substantial loans exceeding Rs 5 lakh and extending up to Rs 2 crore, the LTV ceiling is set at 85%. Crucially, the overall maximum LTV across all gold loan products cannot exceed 85%, ensuring that no regulated financial institution can bypass this mandate, regardless of its marketing strategies. Furthermore, gold loans are typically extended against 18 to 22-karat gold jewellery and ornaments, and against gold coins of up to 24-karat purity, with the karat value directly influencing the assessed value and thus the applicable LTV tier. This tiered structure means that a lender appearing to offer a low interest rate for smaller loan amounts might not maintain that competitive edge as the loan size increases, underscoring the importance of understanding these regulatory nuances.

Leveraging Gold Loan Eligibility Calculators for Informed Decisions

A highly practical and recommended preliminary step for any potential borrower is to utilize an online gold loan eligibility calculator before engaging directly with lenders. Most prominent financial institutions, including Bajaj Finance, provide these tools on their official websites. By inputting the weight and karat of their gold, users can obtain an approximate eligible loan amount. This calculation is typically based on IBJA-referenced rates and incorporates the applicable LTV limits, providing a clear baseline figure. Armed with this information, borrowers can ascertain which LTV tier their loan falls into and, more importantly, request interest rates specific to that precise amount. This proactive approach significantly streamlines the comparison process, moving away from broad, generic quotes to a more focused and personalized discussion. Instead of beginning from scratch at each branch, borrowers arrive with a well-defined financial understanding, facilitating a more efficient and targeted negotiation for the most suitable interest rates.

Beyond Interest Rates: The True Cost of Gold Loans

While the interest rate is undeniably the largest component of borrowing cost, it is by no means the sole expense associated with a gold loan. A holistic evaluation must encompass all ancillary charges that contribute to the total cost of borrowing. These often include processing fees, valuation charges, documentation costs, and potential prepayment penalties. It is entirely conceivable that a lender offering an interest rate marginally higher than the absolute lowest found elsewhere could still present a more cost-effective solution overall, particularly if it features significantly lower ancillary charges or waives foreclosure penalties. For instance, Bajaj Finance distinguishes itself by not imposing any foreclosure or part prepayment fees on its gold loans. Therefore, a truly accurate comparison should always be predicated on the total cost of borrowing over the loan’s lifecycle, rather than an isolated focus on the headline interest rate alone. This comprehensive perspective is vital for avoiding unexpected financial burdens and ensuring optimal savings.

Strategic Approach to Securing Optimal Gold Loan Terms

Ultimately, the objective of securing the lowest gold loan interest rate is a commendable financial goal, yet it must be integrated into a broader strategy that considers all aspects of the lending agreement. Initiating the process with an online gold loan eligibility calculator provides an indispensable starting point, offering clarity on the approximate loan amount and the corresponding LTV tier. This preliminary insight then allows for a more informed assessment of how the chosen loan tenure influences the interest rates offered by various institutions. By carefully scrutinizing all applicable charges—including processing fees, valuation costs, and any potential penalties—borrowers can construct a full financial picture. This diligent approach, moving beyond superficial rate comparisons to a thorough analysis of total borrowing costs and regulatory frameworks, empowers individuals to make financially astute decisions, ensuring they secure the most favorable gold loan terms in the Indian market.