Interbank Call Rates Surge to 5% Amidst Tight Liquidity

By Sivam

Interbank call rates hit 5.00% due to tight liquidity and high demand from banks during a key reporting cycle. Analysis of market dynamics.

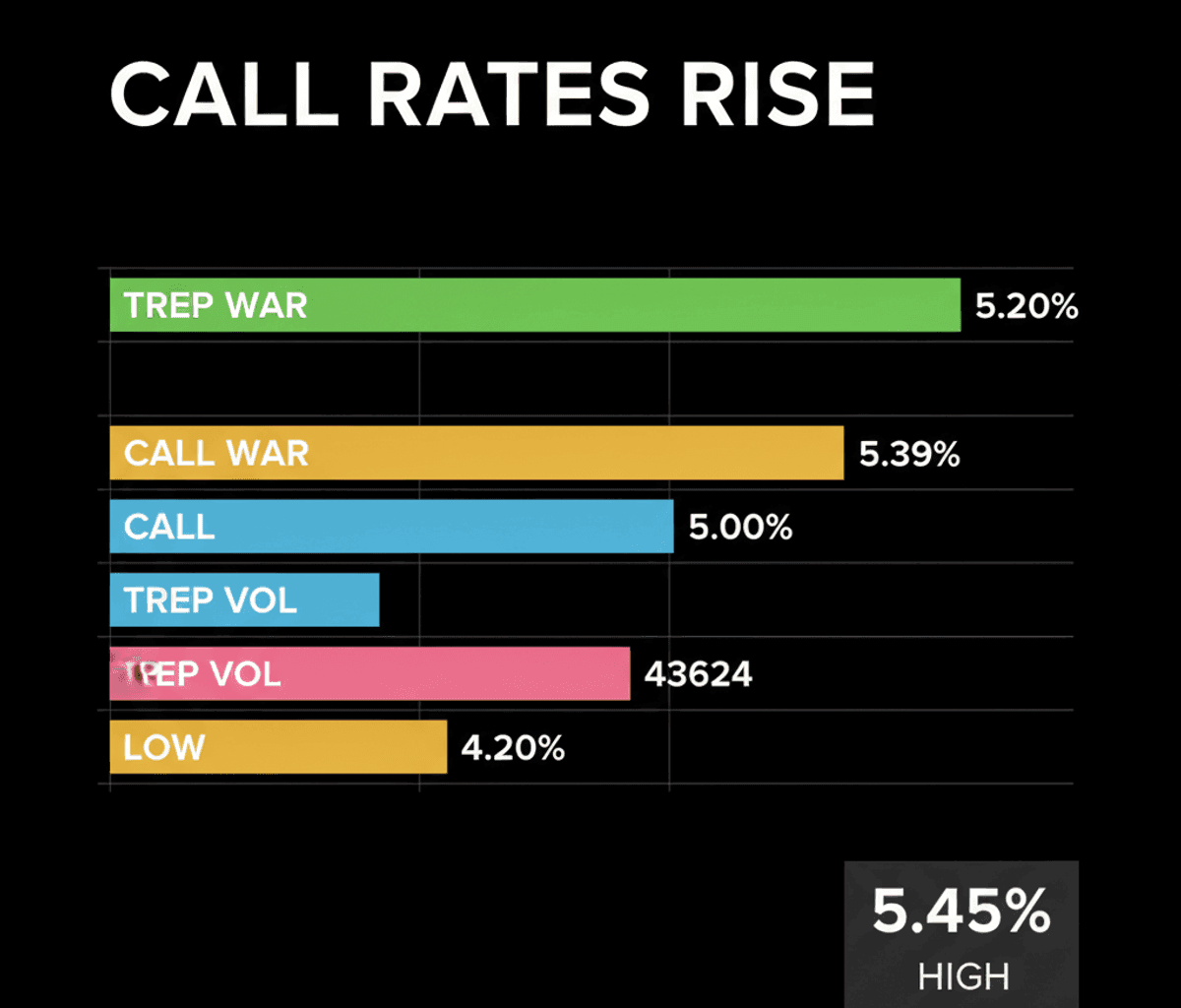

Interbank call rates, the critical benchmark for short-term borrowing between financial institutions, experienced a notable uptick on Wednesday, reaching 5.00%. This increase, observed in the initial week of the reporting cycle, is a direct consequence of pronounced demand from borrowing banks amid a prevailing environment of tight liquidity within the broader banking system, according to Accord-news.

Understanding Interbank Liquidity Dynamics

At its core, the call money market operates on fundamental supply and demand principles for overnight funds. Banks with surplus liquidity lend to those facing shortfalls, a mechanism vital for daily operational solvency. The shift from Tuesday’s 4.85% to Wednesday’s 5.00% signals a clear tightening of this crucial interbank funding tap, driven by an immediate need for funds.

This movement gains additional context when examining the Weighted Average Rate (WAR) in the call money market, which edged up marginally to 5.39% on Wednesday from 5.38% the previous day. Such incremental shifts in the WAR often precede or confirm broader liquidity trends, illustrating the collective pressure on short-term funding costs.

The Mechanism of Tight Liquidity

The increase in call rates is not an isolated event but a predictable outcome when system-wide liquidity tightens. When the aggregate pool of lendable funds shrinks relative to the borrowing needs of banks, the price of those funds—the call rate—naturally rises. This dynamic is particularly acute during the first week of a reporting cycle, as banks often adjust their reserve positions and manage immediate payment obligations.

Further evidence of this systemic pressure is found in the Triparty Repo (TREP) market, another key segment for short-term borrowing. The WAR in the TREP market registered 5.20% on Wednesday, with a substantial total volume of Rs 43624. This parallel movement across different short-term instruments underscores the pervasive nature of the liquidity constraint, as banks seek funding through various avenues. Overnight borrowing rates, ranging from a low of 4.20% to a high of 5.45%, further illustrate the volatility and elevated cost of securing funds during this period.

Implications for the Financial System

From a first-principles perspective, elevated short-term interbank rates signal higher funding costs for banks. While these are overnight rates, a sustained trend can ripple through the financial system, potentially impacting the cost of credit for businesses and consumers further down the line. It serves as an early indicator of the banking sector’s comfort level regarding its own funding stability.

This structural pattern highlights the constant interplay between market demand, available liquidity, and the implicit role of the central bank in managing these dynamics. When market forces push rates up due to liquidity tightness, it often prompts scrutiny of the central bank’s liquidity operations and overall monetary stance, even if no direct intervention is reported.

A Structural Pattern in Money Markets

The current rise in call rates, therefore, should be viewed not as an isolated incident but as an illustration of a recurring structural pattern within money markets: periods of heightened demand coinciding with constrained liquidity invariably lead to an increase in the cost of short-term capital. Understanding this mechanism is key to interpreting broader financial market signals, rather than merely observing rate changes in isolation. When market participants observe such shifts, the analytical imperative is to distinguish whether the movement signals an idiosyncratic event or a deeper, structural liquidity pattern impacting the entire financial system.