Indian Banking: Growth Amidst Margin Pressures (Q1 FY27)

By Business Desk

Explore the structural shift in Indian banking: robust balance sheets, credit expansion, and margin pressures in Q1 FY27 results. IDBI Bank’s performance highlights key trends.

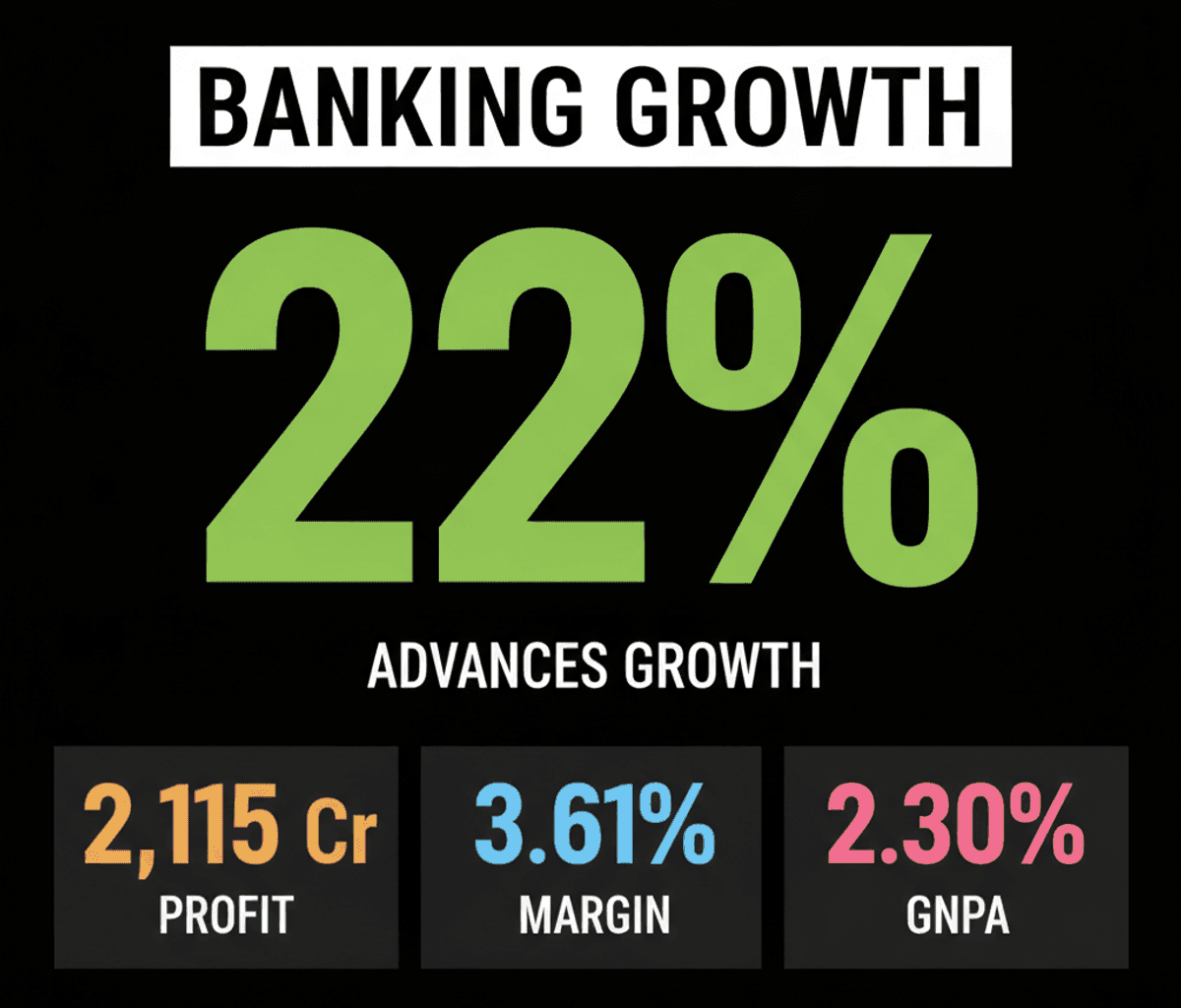

The recent financial disclosures from institutions like IDBI Bank offer a lens into the underlying structural dynamics currently shaping the Indian banking sector. For the first quarter of fiscal year 2027, IDBI Bank announced a 5% year-on-year increase in its net profit, reaching ₹2,115 crore. This growth was not an isolated event but rather a manifestation of broader, system-wide trends: a double-digit surge in net interest income and robust credit expansion.

A core mechanism driving profitability in banking is Net Interest Income (NII), which for IDBI Bank, grew by a significant 10% to ₹3,486 crore. This NII expansion is directly linked to the bank’s formidable 22% growth in net advances, which climbed to ₹2,58,968 crore. Such credit growth is a critical indicator of economic activity and underscores the banking sector’s capacity to fuel investment and consumption across the economy.

However, this robust growth narrative also reveals a nuanced challenge: the slight decrease in the Net Interest Margin (NIM) to 3.61%. While NII expanded, the compression in NIM suggests underlying competitive pressures or shifts in funding costs that require careful analysis. This dynamic highlights a structural balancing act where banks must aggressively pursue credit expansion while navigating a potentially tighter margin environment.

Crucially, the sustainability of this growth rests on a fortified balance sheet. IDBI Bank’s asset quality continued its impressive trajectory, with Gross Non-Performing Assets (GNPA) improving to 2.30% and Net Non-Performing Assets (NNPA) at a mere 0.16%. This improvement, coupled with a high Provision Coverage Ratio (PCR) of 99.31% and a Capital Adequacy Ratio (CRAR) strengthening to 26.92%, illustrates a sector that has significantly de-risked and built substantial capital buffers. These metrics are foundational, indicating a banking system better equipped to absorb shocks and support sustained lending.

What this means for the broader financial ecosystem is a clear signal of structural resilience. The data points from IDBI Bank exemplify a pattern where Indian banks are not merely growing their loan books but are doing so from a position of strength, characterized by healthy asset quality and robust capital. Understanding this interplay between credit expansion, margin dynamics, and balance sheet health is key to appreciating the current phase of the Indian banking sector’s evolution.

The Enduring Significance of Balance Sheet Strength

The consistent improvement in asset quality and capital adequacy ratios across the sector signifies a fundamental shift from previous cycles. This enhanced stability allows banks to pursue growth initiatives with greater confidence, transforming what might otherwise be cyclical upturns into more durable, structural improvements. Even with the nuanced pressure on NIM, the underlying strength provides a critical bedrock for future expansion and profitability, shaping how capital is allocated and risks are managed in the long term.