India’s Strong Finance Sector vs. Slowing Manufacturing

By ThePip Desk

India’s banking sector thrives with record-low NPAs & growth. However, manufacturing expansion moderates, revealing complex economic trends. RBI report insights.

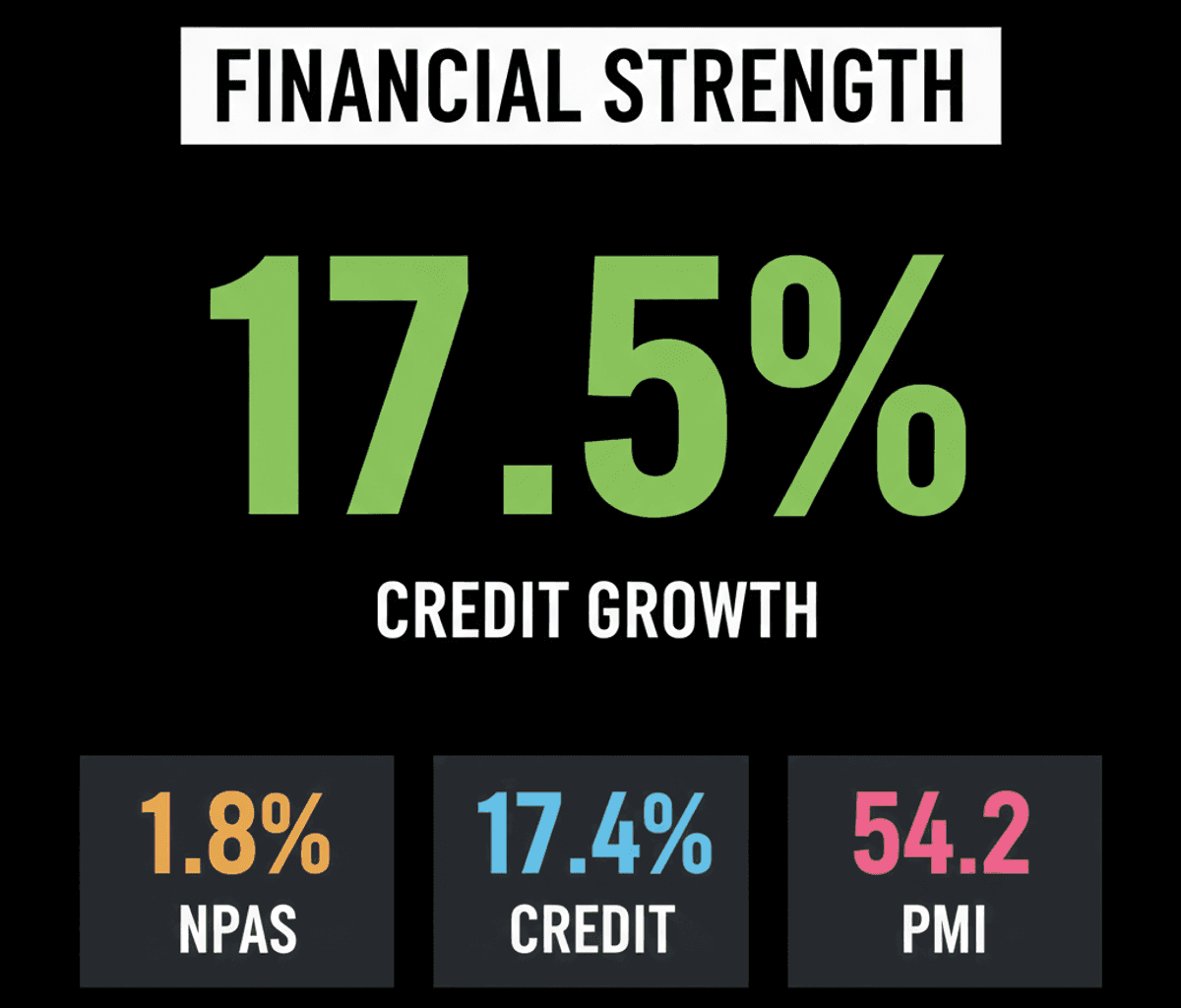

India’s financial system demonstrates robust resilience, a crucial bulwark against potential external shocks, according to the Reserve Bank of India’s (RBI) Financial Stability Report (FSR). This assessment is underpinned by strong balance sheets across both banking and non-banking sectors, with gross non-performing assets (NPAs) for banks reaching a multi-decadal low of 1.8% by the close of March 2026.

This structural strength provides a crucial buffer, as noted by the RBI, though potential exchange rate volatility stemming from rising oil prices remains a flagged risk if global normalisation is delayed. The country’s sound macroeconomic fundamentals are posited to offer greater resilience compared to past crisis episodes.

Understanding the Divergence: Credit Growth vs. Manufacturing Slowdown

While the financial sector exhibits an impressive degree of stability and growth, the real economy presents a more nuanced picture, marked by a divergence in performance across key sectors. This creates an interesting dynamic where financial strength coexists with sectoral moderation.

Bank credit to the industrial sector experienced a significant year-on-year growth of 17.5% by the end of May 2026, marking a sharp acceleration from 5.3% recorded in the corresponding period last year. This expansion was notably broad-based, encompassing significant advances to large industries and sustained healthy growth within the Micro, Small, and Medium Enterprises (MSE) sector.

This robust credit impulse extends beyond industry, with non-food bank credit accelerating to 17.4% year-on-year in the fortnight ending May 31, 2026. Furthermore, credit to agriculture and allied activities also strengthened considerably, growing 14.9% against 7.5% a year earlier, indicating widespread demand for capital across various economic segments.

However, this financial dynamism contrasts with a discernible slowdown in India’s manufacturing sector activity. The HSBC India Manufacturing Purchasing Managers’ Index (PMI) eased to 54.2 in June from 55.0 in May, indicating continued expansion but at a decelerated pace. This moderation was evident across key sub-components, including output, new orders, export orders, and employment.

Notably, international sales recorded their weakest increase since March 2023. This suggests a potential softening in global demand or increased competitive pressures impacting India’s manufacturing export capabilities, even as domestic credit availability remains strong.

Inflation Dynamics and External Vulnerabilities

Despite the manufacturing slowdown, the broader inflationary environment appears to be softening, offering a measure of relief. Both input and output price indices declined in June, suggesting that the pressures from geopolitical disruptions are beginning to recede. This easing of inflation, even as manufacturing moderates, points to a complex interplay between demand, supply-side factors, and global commodity prices.

The RBI’s report, while highlighting resilience, prudently flags potential vulnerabilities that could test this stability. A significant rise in global oil prices could trigger increased exchange rate volatility, challenging the current macroeconomic equilibrium. This serves as a critical reminder that domestic financial strength is always interwoven with, and susceptible to, external economic forces.

The Structural Takeaway: Resilience in the Face of Sectoral Shifts

The current economic landscape in India presents a compelling study in divergence: a deeply resilient financial system acting as a robust foundation, juxtaposed with sector-specific decelerations in the real economy. The acceleration in credit, particularly to industries and MSEs, suggests underlying confidence and investment appetite, which could eventually re-energize broader economic activity.

Yet, the manufacturing slowdown, particularly in exports, indicates that global headwinds or domestic structural adjustments are at play. Understanding this nuanced interplay—strong financial plumbing supporting a real economy undergoing recalibration—is crucial for assessing India’s current economic trajectory and anticipating future shifts in its growth drivers.