ICICI Bank Q1 Profit Surges 16% on Strong Loan Growth

By Business Desk

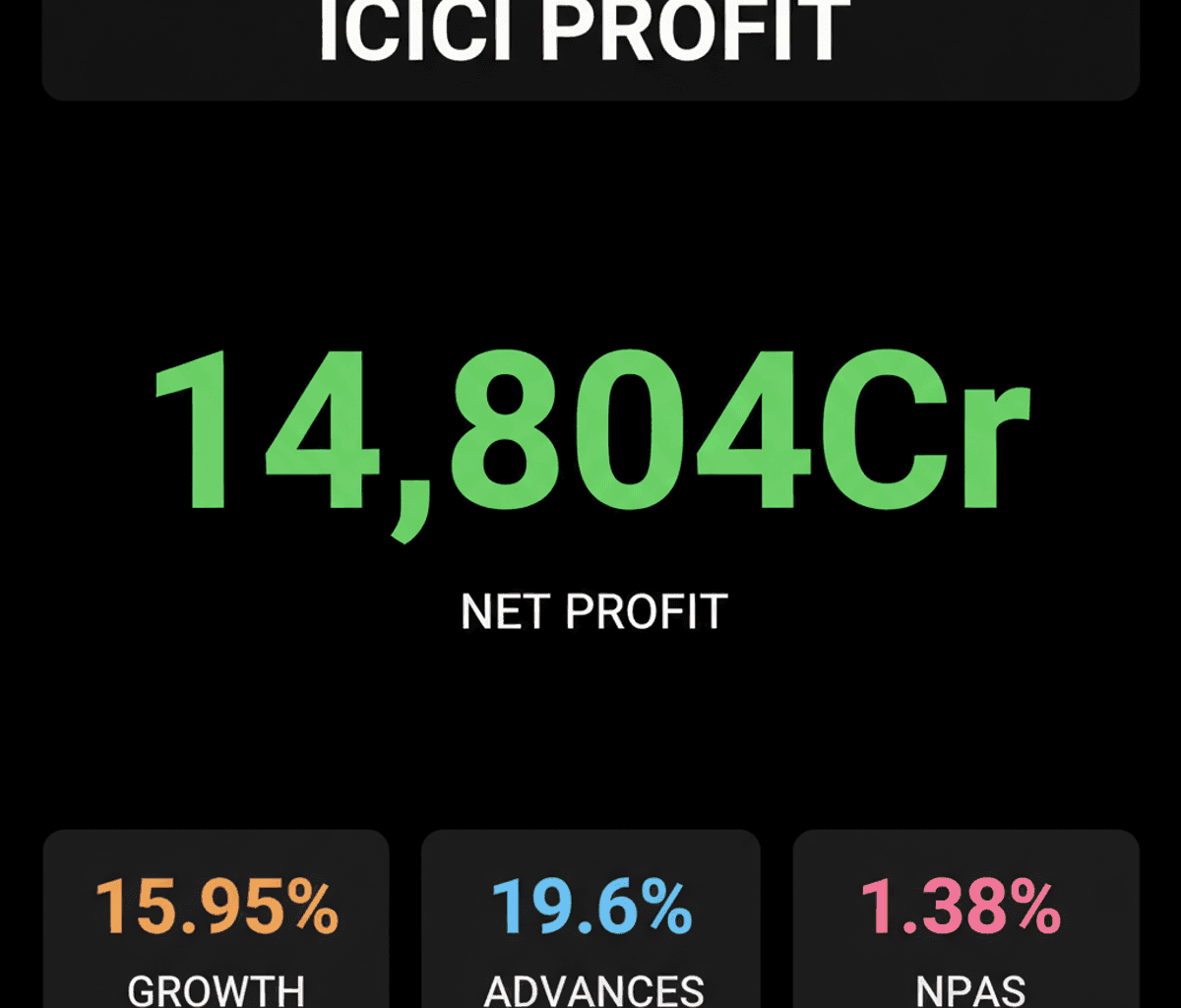

ICICI Bank’s Q1 FY27 net profit soared 16% to Rs 14,804.50 crore, driven by robust loan growth and improved asset quality. Discover key financial highlights.

🔥 Main Takeaway

ICICI Bank crushed its Q1 FY27 earnings, with standalone net profit jumping nearly 16% thanks to impressive loan growth and significantly improved asset quality.

📌 What Happened?

Standalone net profit for Q1 FY27 surged to Rs 14,804.50 crore, marking a solid 15.95% increase compared to Rs 12,768.21 crore in Q1 FY26.

Net Interest Income (NII) climbed 12.7% year-on-year, reaching Rs 24,384 crore, while the Net Interest Margin (NIM) slightly improved to 4.36% from 4.34% in the prior year.

The bank’s total advances soared 19.6% year-on-year to Rs 16,31,260 crore, complemented by a 14% growth in its deposit base to Rs 18,33,586 crore as of June 30, 2026.

Asset quality showed considerable improvement, with gross non-performing assets (NPAs) reducing to 1.38% from 1.67%, and net NPAs declining to 0.35% from 0.41%.

Provisions, excluding tax, decreased by a significant 30.58% to Rs 1,260 crore, signaling a healthier financial position.

💰 Why It Matters

ICICI Bank’s robust profit growth highlights its operational strength and ability to perform well, making it a strong contender for investors seeking stable financial sector plays.

The sharp reduction in NPAs and provisions means lower risk for the bank, which often translates to increased investor confidence and a more secure balance sheet.

Strong growth in both advances and deposits indicates healthy demand for credit and effective customer engagement, pointing to a positive outlook for the broader banking sector.

Retail loans now form 49.2% of the total portfolio and contributed approximately 72% of fee income, underscoring a successful consumer-focused strategy that drives consistent revenue streams.

👀 What to Watch Next

Keep an eye on how ICICI Bank maintains its Net Interest Margins amidst evolving interest rate cycles and market competition.

Monitor the continued expansion of its retail loan book and its potential impact on future asset quality metrics.

Watch for further growth in the bank’s deposit base, which is crucial for funding future lending activities and sustaining its impressive growth trajectory.