ICICI Bank Q1 FY27: Record Low NPAs & Strong Profit Growth

By Business Desk

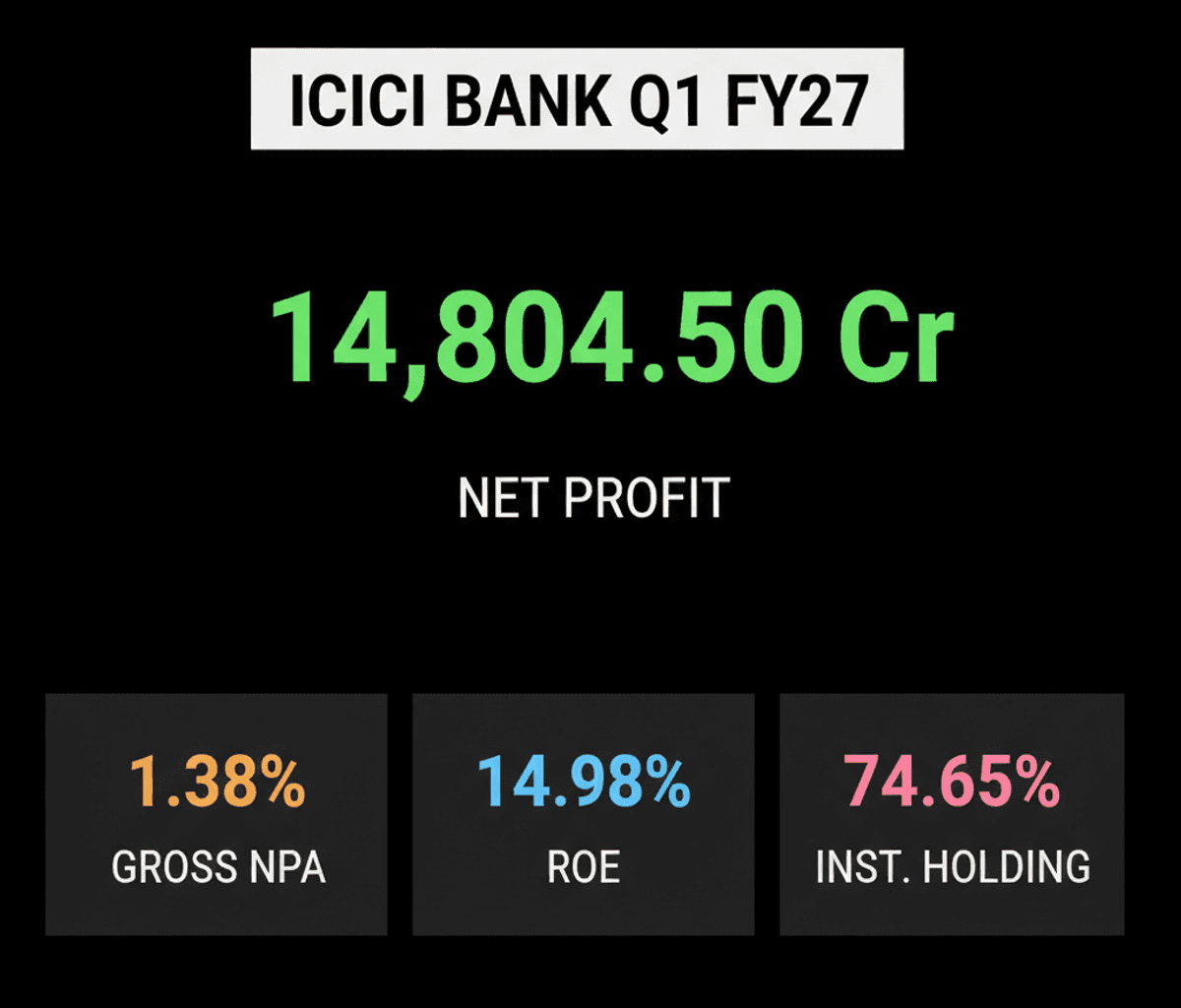

ICICI Bank’s Q1 FY2027 results reveal record-low gross NPAs at 1.38% and significant profit growth, highlighting strong asset quality and investor confidence.

🔥 Main Takeaway

ICICI Bank just dropped killer Q1 FY2027 results, flexing record-low bad loans and solid profit growth, signaling a strong play for investors.

📌 What Happened?

ICICI Bank’s net profit surged to ₹14,804.50 crores in Q1 FY2027, jumping 8.05% quarter-on-quarter and 15.95% year-on-year.

The bank hit a new low for gross non-performing assets (NPA) at 1.38%, a slight dip from 1.40% last quarter, with net NPA holding steady at 0.35%.

Total income reached ₹54,246.84 crores, a 7.24% quarter-on-quarter increase, driven by record interest earned of ₹45,670.78 crores.

Net Interest Income (NII) grew 6.12% quarter-on-quarter and 12.71% year-on-year, reaching ₹24,384.35 crores.

Return on Equity (ROE) stood strong at 14.98%, outperforming peers, while Capital Adequacy Ratio (CAR) remained robust at 16.84%.

💰 Why It Matters

This performance showcases ICICI Bank’s superior asset quality and operational efficiency, making it a reliable pick in the Indian banking sector.

The impressive ROE of 14.98% suggests the bank is effectively using capital to boost shareholder returns, a key metric for savvy investors.

Institutional investors still hold a massive 74.65% stake, indicating high confidence despite recent Foreign Institutional Investor (FII) and Mutual Fund adjustments.

The stock has consistently beaten the Sensex, with a 5-year return of 118.39% versus Sensex’s 47.07%, highlighting its long-term growth potential.

MarketsMojo upgraded its valuation to “Fair” from “Expensive” and issued a “BUY” rating with a target price of ₹1,580, suggesting a 9.58% upside from the current market price.

👀 What to Watch Next

Keep an eye on future NPA trends; maintaining this low level will reinforce ICICI Bank’s strong financial health.

Monitor Net Interest Income (NII) growth for continued evidence of strong pricing power and effective liability management.

Watch for any shifts in institutional investor sentiment, though current holdings suggest strong long-term conviction in the bank.

Check if the stock hits the ₹1,580 fair value target, confirming the MarketsMojo “BUY” signal and potential for further gains.