HDFC Bank’s ₹10 Lakh Crore Real Estate Exposure: Risks & Analysis

By ThePip Desk

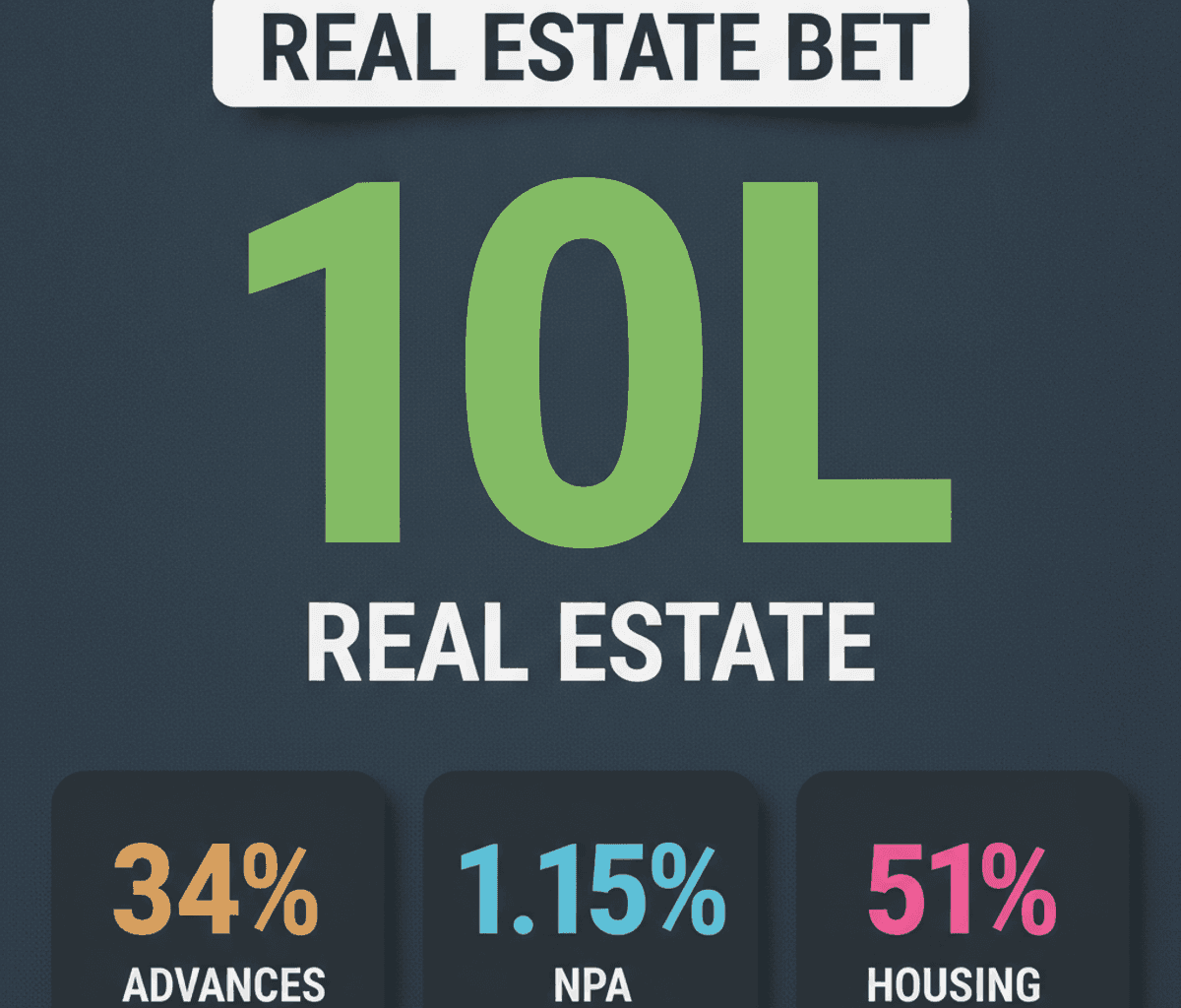

HDFC Bank’s real estate advances hit ₹10 lakh crore (34% of total). Explore the risks and implications of this sectoral concentration amidst low NPAs.

HDFC Bank’s real estate portfolio expanded to over ₹10 lakh crore in fiscal year 2026, constituting a significant 34% of its total advances book. This substantial concentration, particularly following its merger with HDFC Ltd in July 2023, positions real estate as the bank’s largest single sectoral exposure, prompting an analysis of its underlying risk management framework.

The bank’s real estate commitment is predominantly in residential mortgages, accounting for ₹7.39 lakh crore. Commercial real estate exposure stands at ₹2.12 lakh crore, with an additional ₹50,843.77 crore in indirect exposure via the National Housing Bank and other housing finance companies. This growth trajectory saw the total real estate exposure increase by ₹77,479 crore in FY26 compared to FY25. Priority sector housing loans within the mortgage segment surged by 51% year-on-year, while commercial real estate lending rose by 12.4% over the same period.

This level of sectoral concentration, particularly in a cyclical industry like real estate, typically raises questions about systemic risk. However, HDFC Bank reported a gross Non-Performing Asset (NPA) ratio of just 1.15% in FY26, marking a multi-decadal low. The quality of its mortgage credit has also remained stable, suggesting that robust underwriting and monitoring mechanisms are currently mitigating the inherent risks associated with such a large portfolio.

The bank’s strong asset quality in real estate is buttressed by prevailing market conditions. Property prices have demonstrated resilience, and demand in key commercial real estate segments, notably office spaces and warehousing, has remained consistent. These external factors provide a favorable backdrop, supporting the performance of the bank’s substantial real estate loan book.

Interestingly, the bank’s Managing Director and CEO, in their letter, did not flag real estate concentration as a significant risk. This perspective underscores a broader structural pattern in Indian banking, where leading institutions, equipped with sophisticated risk assessment models and benefitting from a relatively stable macro-economic environment, are increasingly confident in deploying capital into growth sectors. While high concentration always warrants scrutiny, the reported figures suggest a calculated strategy rather than an unmanaged gamble.

The HDFC Bank case offers a crucial lens into how large financial institutions manage significant sectoral bets. It highlights the interplay between strategic mergers, robust internal controls, and supportive market dynamics in shaping a bank’s risk profile. For the financial ecosystem, understanding this balance between concentrated exposure and meticulously managed asset quality is key to assessing the resilience of the broader banking sector.