HDFC Bank Q1 Profit Surges 5% on Strong Consumer Lending

By Business Desk

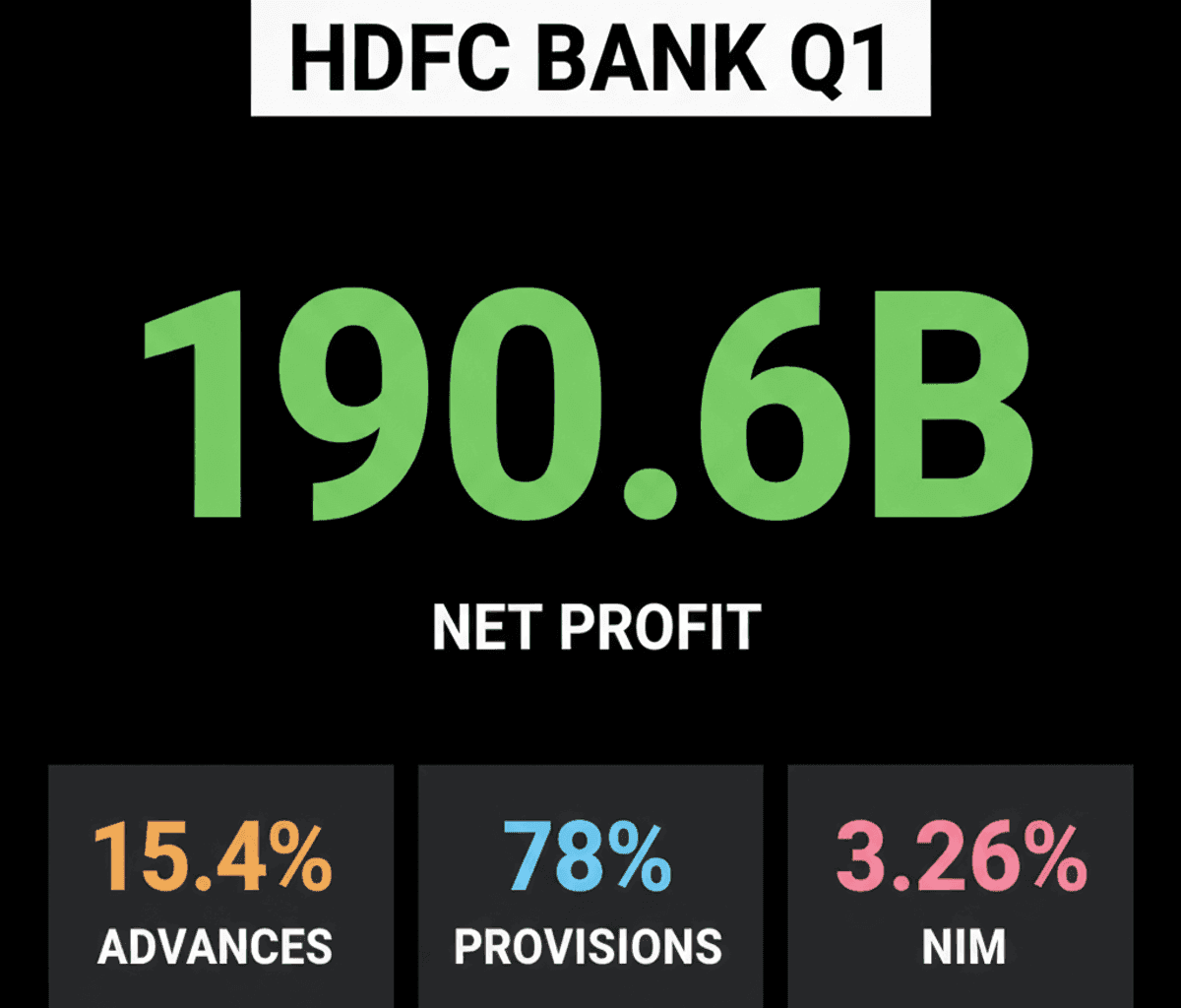

HDFC Bank’s Q1 profit rose 5% to ₹190.60 billion, driven by robust consumer lending and reduced bad loan provisions, showcasing resilience in the Indian banking sector.

🔥 Main Takeaway

India’s banking giant HDFC Bank just crushed Q1 estimates, posting a 5% profit jump thanks to booming consumer loans and fewer bad debts.

📌 What Happened?

HDFC Bank reported a standalone net profit of 190.60 billion Indian rupees ($1.98 billion) for the quarter ending June 30, a 5% increase year-on-year.

This performance met analyst expectations, primarily fueled by a significant pick-up in consumer lending and a sharp reduction in provisions for bad loans.

Advances saw a 15.4% rise, driven mostly by retail loans like mortgages and personal debt, while total deposits grew by 13.3%.

Net interest income, a core profitability metric, increased by 6.7% to 335.3 billion rupees, and provisions for contingencies plummeted 78% year-on-year to 30.6 billion rupees.

However, other income, derived from treasury operations and fee income, dropped 41% quarter-on-quarter to 128.21 billion rupees, impacted by rising bond yields and central bank forex restrictions.

💰 Why It Matters

HDFC Bank’s strong Q1 results signal a robust consumer lending environment in India, indicating healthy economic activity and consumer confidence.

The substantial decrease in bad loan provisions suggests improved asset quality and efficient risk management, which boosts investor confidence in the bank’s stability.

Despite ‘other income’ facing headwinds, the consistent growth in core lending and deposits underscores the bank’s fundamental strength and leading market position.

Maintaining a net interest margin (NIM) at 3.26% is crucial, even if it remains below pre-merger levels, showing disciplined financial management in a dynamic market.

👀 What to Watch Next

Keep an eye on HDFC Bank’s strategy to expand its net interest margin, aiming to return closer to the 4% levels seen before its 2023 merger.

Monitor how rising bond yields and the Indian central bank’s forex restrictions continue to influence the bank’s ‘other income’ in upcoming quarters.

Also, watch for news regarding the reappointment of CEO Sashidhar Jagdishan and the new chairman Rajiv Kumar, as leadership continuity often signals future strategic direction.