HDFC Bank Deposits Soar 13% in Q1 FY27

By ThePip Desk

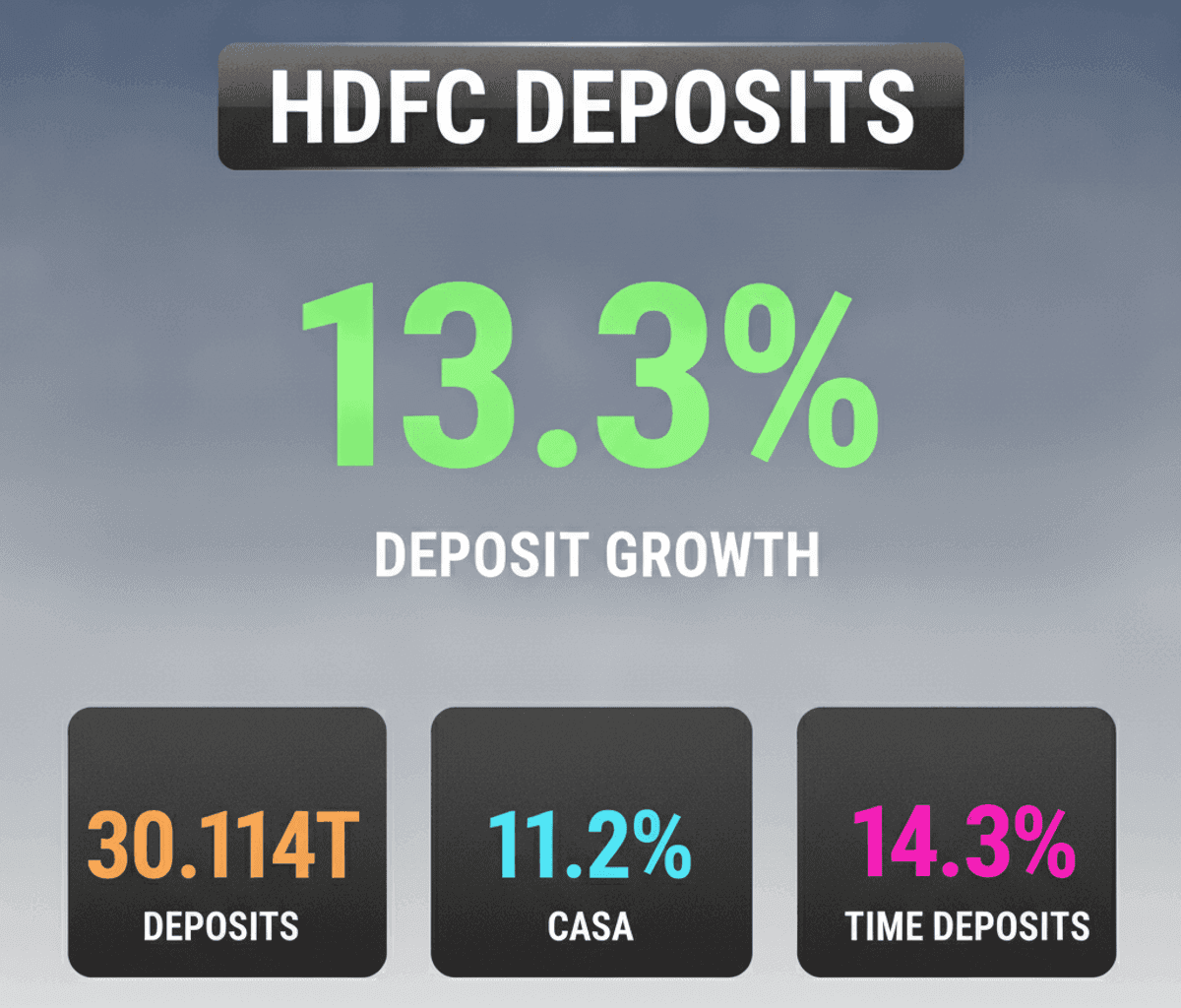

HDFC Bank reports a strong 13.3% YoY growth in average deposits to Rs 30,114 billion for Q1 FY27, signaling robust funding and lending capacity.

🔥 Main Takeaway

HDFC Bank’s average deposits surged over 13% year-on-year in the June 2026 quarter. This robust growth in its funding base signals a strong position for future lending and overall financial health.

📌 What Happened?

The bank reported average deposits reaching an impressive Rs 30,114 billion for the June 2026 quarter. This figure marks a substantial 13.3% increase compared to the Rs 26,576 billion recorded in the same period of 2025.

Both Current Account Savings Account (CASA) deposits and time deposits contributed significantly to this growth. Average CASA deposits climbed 11.2% to Rs 9,570 billion, up from Rs 8,604 billion a year prior. Meanwhile, average time deposits saw an even stronger rise of 14.3%, hitting Rs 20,544 billion from Rs 17,972 billion.

By the close of June 30, 2026, HDFC Bank’s period-end deposits stood at approximately Rs 31,705 billion. These numbers underline the bank’s consistent ability to attract and retain customer funds.

💰 Why It Matters

Strong deposit growth is crucial as it directly fuels the bank’s capacity to extend loans. This increased lending potential is a key driver for revenue generation and overall profitability. Furthermore, the healthy mix between CASA and time deposits demonstrates a diversified funding strategy, which reduces the bank’s reliance on potentially more expensive wholesale funding sources.

For investors, this performance highlights HDFC Bank’s continued market dominance and operational strength in securing customer capital. Consistent growth in deposits signals underlying economic stability and sustained consumer confidence in the institution, making it an attractive prospect for those tracking wealth-building trends.

👀 What to Watch Next

Investors should closely monitor how this impressive deposit accumulation translates into actual credit growth and the bank’s Net Interest Margin (NIM) in upcoming quarterly results. These metrics will offer deeper insights into the efficiency of capital deployment.

It will also be important to observe HDFC Bank’s ongoing deposit acquisition strategies, especially within an increasingly competitive interest rate environment. Continued strong performance in this area would further reinforce HDFC Bank’s reputation as a stable and reliable investment within the financial sector.