India’s ₹1 Lakh Credit Card Debt Trap: How It Spirals

By Sivam

Discover how high credit limits and minimum payments trap Indian borrowers, turning a ₹1 lakh credit card bill into a financial crisis. Learn to avoid the debt spiral.

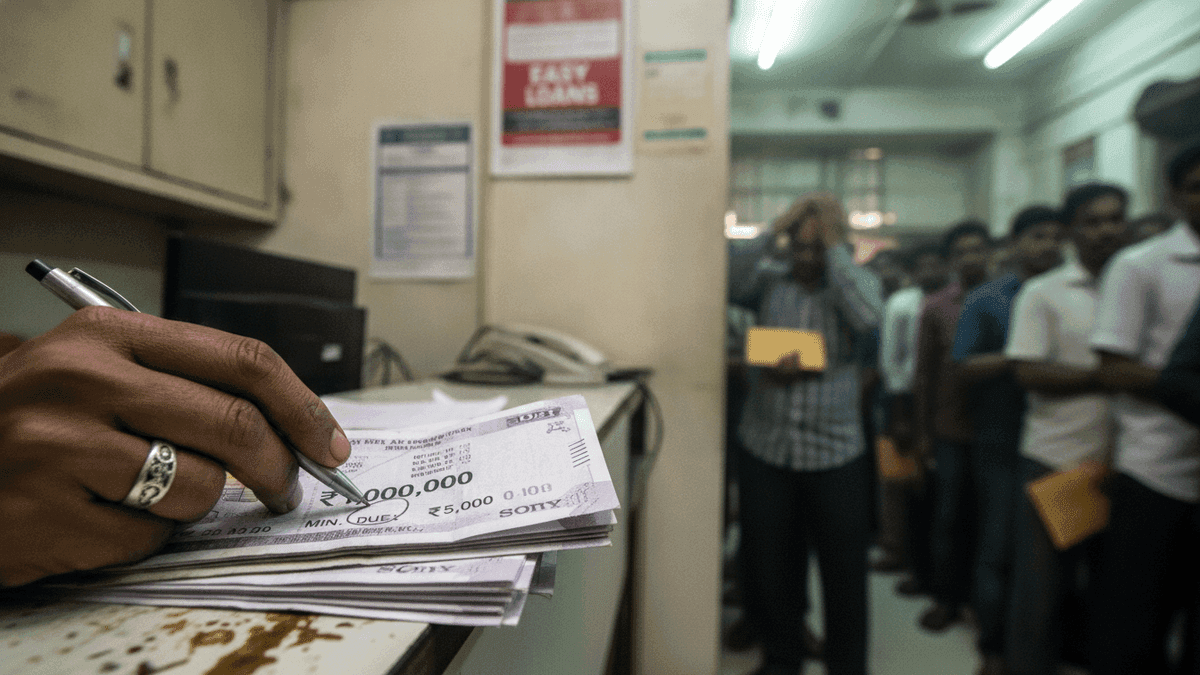

Credit card debt is emerging as a significant financial challenge for consumers in India, where the combination of high credit limits and the option of minimum due payments is fostering a perilous environment. Financial experts are increasingly highlighting how this debt trap initiates, warning that even an initial ₹1 lakh bill can rapidly escalate into an unmanageable burden. This situation underscores a growing and critical issue within the nation’s personal finance landscape, impacting a broad spectrum of individuals.

The Mechanics of Debt Accumulation

At the heart of the problem lies the often-misunderstood interplay between generous credit limits extended by banks and the seemingly convenient option of paying only the minimum amount due. While offering immediate purchasing power and financial flexibility, this approach frequently conceals the true, escalating cost of borrowing. Outstanding balances accumulate interest at exceptionally high annual percentage rates, a factor many borrowers overlook.

This compounding interest mechanism allows a relatively modest initial debt to grow exponentially, making the prospect of full repayment increasingly daunting. For numerous borrowers, the ability to consistently make only minimum payments provides a deceptive sense of control over their finances, effectively postponing a more significant financial reckoning. This deferred payment strategy, especially when coupled with continued reliance on credit for new purchases, inevitably leads to a persistent cycle of debt accumulation. Consequently, an initial ₹1 lakh bill can quickly balloon into a much larger, overwhelming sum due to these relentless interest charges.

Expert Warnings and Borrower Vulnerability

Financial experts across India are issuing stark warnings regarding the widespread prevalence and insidious nature of this credit card debt spiral. They emphasize that the trap often begins subtly, with consumers utilizing a significant portion of their credit limits or making substantial purchases without a robust, predefined plan for timely and complete repayment. The relative ease of access to credit, often bolstered by aggressive marketing campaigns from various financial institutions, significantly contributes to this heightened vulnerability among borrowers.

These specialists further highlight that a critical lack of comprehensive financial literacy, particularly concerning complex interest calculations and the long-term financial implications of consistently making only minimum payments, severely exacerbates the problem. Many borrowers frequently underestimate the true cumulative cost of their credit card purchases when interest is applied and compounded over extended periods. A fundamental understanding of this genuine interest burden is absolutely essential for individuals seeking to effectively break free from the cycle of mounting debt.

Strategies to Avoid the Spiral

To effectively navigate away from the looming credit card debt trap, financial experts strongly advise borrowers to prioritize paying substantially more than just the minimum due whenever their financial situation allows. Even marginal increases in payment amounts can lead to significant reductions in the principal balance and, critically, the total interest paid over the lifespan of the debt. Cultivating a disciplined and proactive repayment strategy is therefore paramount for ensuring long-term financial stability and health.

Another pivotal recommendation involves exercising extreme judiciousness with allocated credit limits. Borrowers are cautioned against routinely maxing out their credit cards, regardless of how high the approved limit may be. Instead, credit should be utilized responsibly, ideally for carefully planned expenses or genuine emergencies. Consistently monitoring credit card statements, meticulously tracking expenditures, and maintaining a clear understanding of the specific interest rates applied are fundamental, proactive steps for individuals to retain firm control over their personal finances and prevent any debt from spiraling irrevocably out of control.