Cooperative Insurance for Rural India: Financial Inclusion Focus

By ThePip Desk

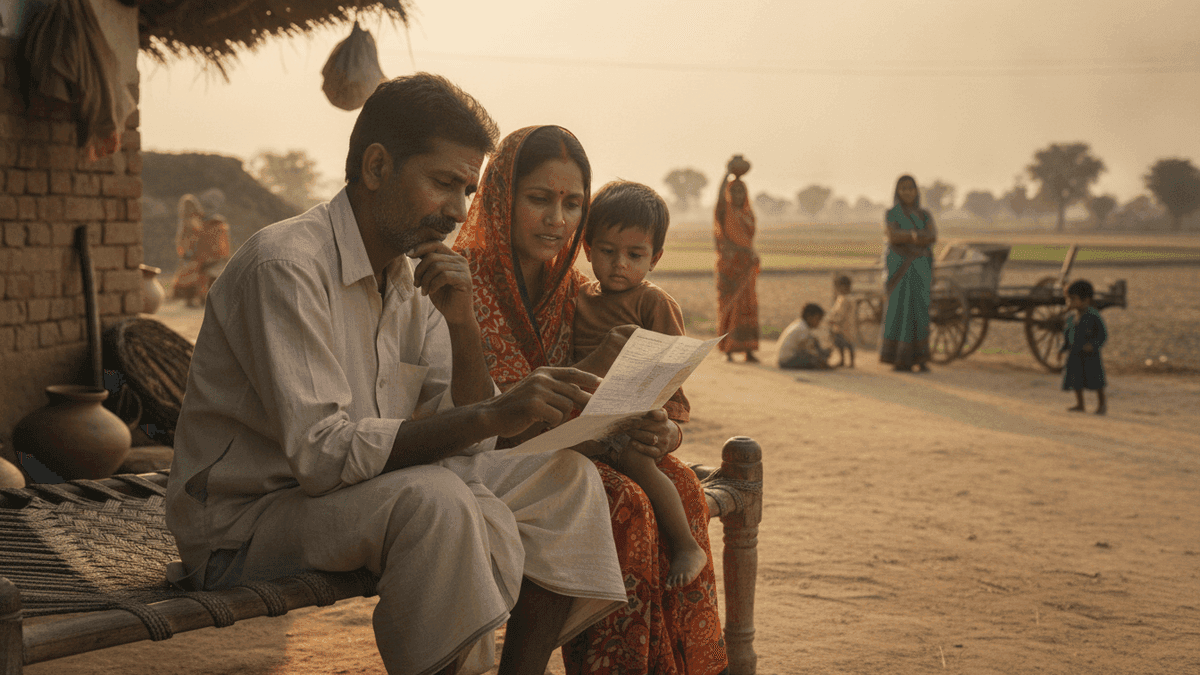

Amit Shah’s new cooperative life insurance aims to boost rural financial inclusion, reviving the 1904 movement’s spirit of mutual support for underserved communities.

The recent announcement by Union Home Minister Amit Shah regarding the establishment of a life insurance company within India’s cooperative sector has immediately prompted a significant call for structural intent. A collective comprising former senior bankers, educators, and economic officers, all alumni of SCD Government College, has appealed to the Central government, advocating for the proposed entity to be specifically designed to benefit the nation’s rural population first and foremost.

This initiative represents a critical juncture for the cooperative movement, which traces its foundational principles back to the Co-operative Credit Societies Act of 1904. As Brij Bhushan Goyal, a retired banker, noted, this historical legislation was initially conceived to empower farmers through mutual support and shared ownership models, primarily focusing on rural credit. The cooperative structure, in essence, was a mechanism for collective financial resilience in underserved communities.

The proposed Cooperative Life Insurance Company, therefore, signifies a pivotal evolution of this established model. Goyal highlights its potential to expand beyond the traditional domain of rural credit, introducing a vital financial product — life insurance — into a sector historically characterised by limited access to such services. This expansion implies a structural broadening of the cooperative’s role from basic credit provision to comprehensive financial security, directly addressing a gap in the rural financial ecosystem.

To ensure this structural benefit translates into tangible impact at the ground level, KB Singh, a former Deputy General Manager and senior economic officer, has put forth a crucial operational safeguard: the implementation of a cap on premiums. This measure is not merely a pricing suggestion; it is a mechanism designed to uphold the core cooperative principle of accessibility. By limiting premium costs, the scheme would remain genuinely affordable for individuals at the ‘last mile’ – those in remote and underserved areas who stand to gain the most from insurance coverage but are often excluded by market-driven pricing.

This development underscores a broader analytical point regarding the adaptability and enduring relevance of the cooperative model. When designed with deliberate structural parameters, such as targeted beneficiaries and premium affordability, the cooperative framework can evolve to address contemporary financial inclusion challenges. The appeals from the SCD Government College alumni group articulate a clear imperative: to ensure that this new cooperative insurance venture does not merely exist, but actively fulfils its potential as a catalyst for deeper financial security across rural India, mirroring the original ethos of collective empowerment.