Central Bank of India Q1 Profit Surges 13.26% on Strong Core Income

By ThePip Desk

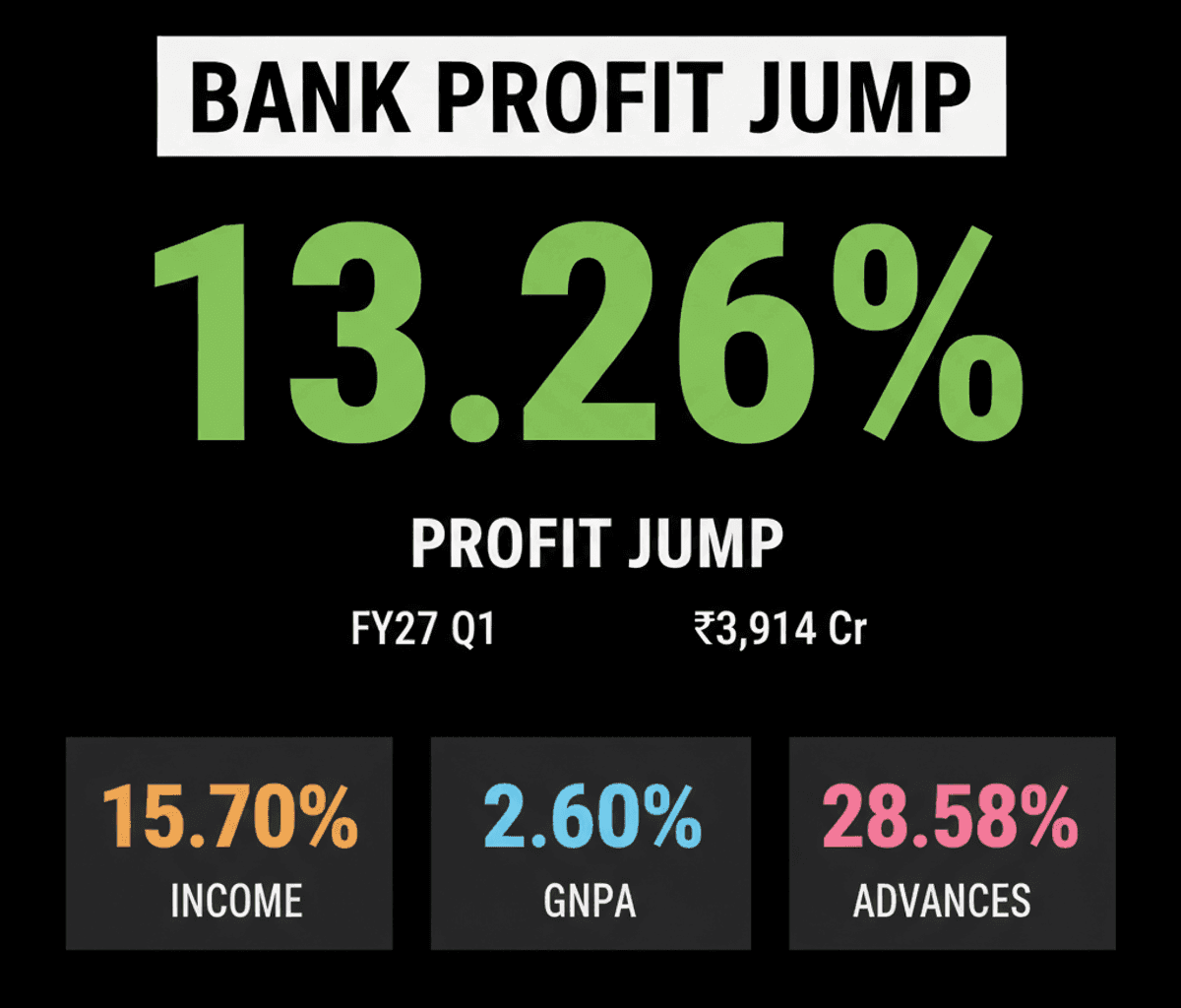

Central Bank of India’s Q1 FY27 net profit soared 13.26% to ₹1,324 crore, driven by robust core income growth and reduced provisions, despite a dip in other income.

🔥 Main Takeaway

Central Bank of India just dropped its Q1 FY27 numbers, revealing a solid 13.26% jump in net profit, fueled by stronger core income and fewer bad loan provisions, even as other income dipped.

📌 What Happened?

Net profit for Central Bank of India surged 13.26% year-on-year to ₹1,324 crore in the first quarter of FY27.

This significant boost came from a 15.70% rise in Net Interest Income (NII), reaching ₹3,914 crore, alongside a notable 24.05% drop in provisions.

However, the Net Interest Margin (NIM) slightly decreased to 3.06% because lending yields fell more sharply than the cost of funds.

Other income, particularly from treasury operations, saw a substantial 44.27% dive to ₹987 crore, contributing to a 5.12% decline in operating profit.

Despite an increase in absolute Gross Non-Performing Assets (GNPA), the GNPA ratio improved to 2.60%.

💰 Why It Matters

A 13.26% profit jump signals robust underlying health for Central Bank of India, especially with core income driving growth and lower provisions freeing up capital.

The improved GNPA ratio to 2.60% is a green flag for investors, indicating better asset quality management and reduced future risk.

Robust global advances growth of 28.58%, primarily from corporate credit, suggests increasing business activity and demand for loans, serving as a positive economic indicator.

The bank’s active target to mobilize $400 million in FCNR(B) deposits showcases a strategic move to diversify funding and potentially lower long-term funding costs.

👀 What to Watch Next

Keep an eye on how Central Bank of India strategically manages its Net Interest Margin, especially as lending yields and funding costs continue to fluctuate in the market.

Future reports will clarify the impact of their FCNR(B) deposit mobilization strategy on overall funding structure and sustained profitability.

Monitor whether the strong growth in advances can be maintained and if asset quality continues its improvement trajectory, particularly if corporate credit momentum persists.