Nomura Bullish on Ather Energy: 22.5% Upside Seen

By ThePip Desk

Nomura reiterates ‘Buy’ on Ather Energy, raising target to ₹1,470 (22.5% upside). A top EV pick in India’s booming electric two-wheeler market.

🔥 Main Takeaway

Nomura sees Ather Energy as a top EV play, hiking its target price by 22.5% to ₹1,470 as India’s electric two-wheeler market gears up for massive growth.

📌 What Happened?

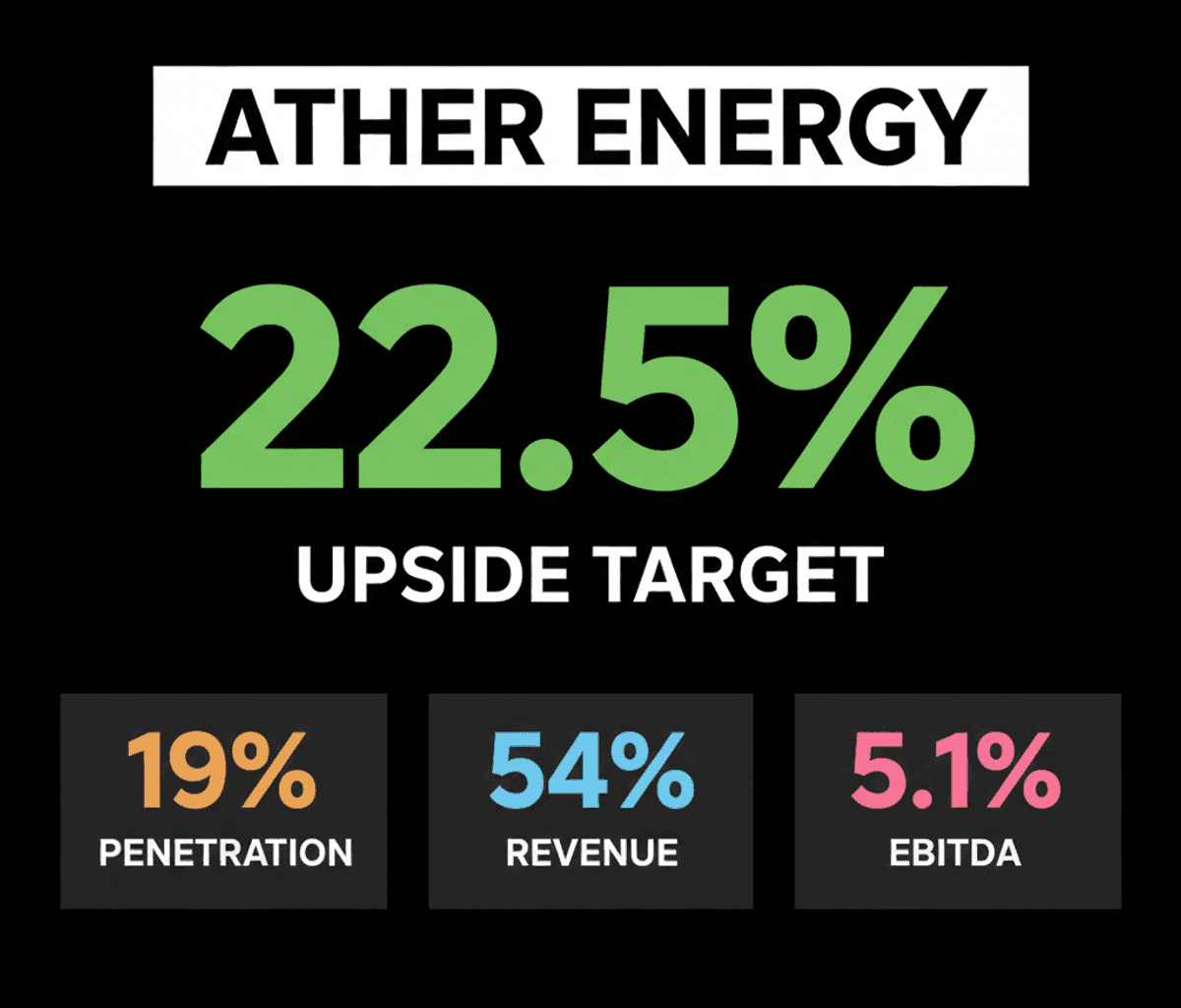

Nomura reiterated a ‘Buy’ rating on Ather Energy, boosting its target price from ₹1,120 to ₹1,470. This new target implies a significant 22.5% upside from Ather’s previous closing price of ₹1,200 on the NSE.

The brokerage highlights Ather’s strong position as a pure-play electric two-wheeler manufacturer. India’s electric two-wheeler penetration is projected to jump from approximately 6.5% in FY26 to nearly 19% by FY30.

Ather maintained an 18% market share in FY26, even amidst reported supply constraints. This demonstrates its resilience and brand strength in a competitive landscape.

💰 Why It Matters

For investors, this signals high growth potential in a rapidly expanding market. Ather is positioned as a key beneficiary of the accelerating shift towards electric mobility in India.

Ather plans to launch an affordable scooter, based on the EL platform, in Q3 FY27. This product targets the massive ₹1 lakh-₹1.25 lakh segment, which constitutes about 45% of the total industry, potentially boosting volumes significantly.

Nomura forecasts impressive revenue growth: 54% in FY27, 57% in FY28, and 36% in FY29. This growth is driven by increasing unit volumes and slight average selling price hikes, offsetting commodity costs.

Profitability is on the horizon for Ather, with EBITDA margins expected to improve from negative 6% in FY27 to 5.1% in FY29. The company anticipates reaching PAT breakeven by FY29.

👀 What to Watch Next

Keep a close watch on the Q3 FY27 launch of Ather’s affordable scooter; its market reception will be crucial for hitting future volume targets and expanding market share.

The introduction of a new motorcycle platform could further elevate growth estimates beyond current projections. This represents an additional upside catalyst not fully factored in.

Monitor global fuel prices; sustained high costs could accelerate EV adoption, while easing prices might temper demand slightly. Ather’s valuation at around 4 times FY28 EV/sales is considered attractive, but market sentiment remains dynamic.