CATL’s Android Moment: EV Platform Dominance Shifts Value

By ThePip Desk

CATL is becoming the Android of EVs, shifting value from carmakers to its dominant technology platform. Explore this major industry transformation.

The automotive industry, long dominated by established carmakers, is witnessing a profound structural shift, best understood through the lens of the “Android Moment.” Contemporary Amperex Technology Co. Limited (CATL), initially known as a battery supplier, is strategically repositioning itself as a foundational technology platform provider within the electric vehicle (EV) ecosystem. This transformation fundamentally alters where value accrues in the supply chain, drawing a direct parallel to how Google’s Android operating system became more powerful than individual smartphone brands.

CATL’s strategy transcends mere component supply, encompassing a vertical and horizontal integration across the entire EV value chain. Its comprehensive ecosystem now includes core power batteries, advanced energy storage systems, sophisticated battery management software, rapid-charging innovations, next-generation sodium-ion batteries, robust recycling initiatives, and an expansive battery swapping infrastructure. Beyond these, the company is actively investing in raw material acquisition and, crucially, developing foundational vehicle architecture and chassis platforms.

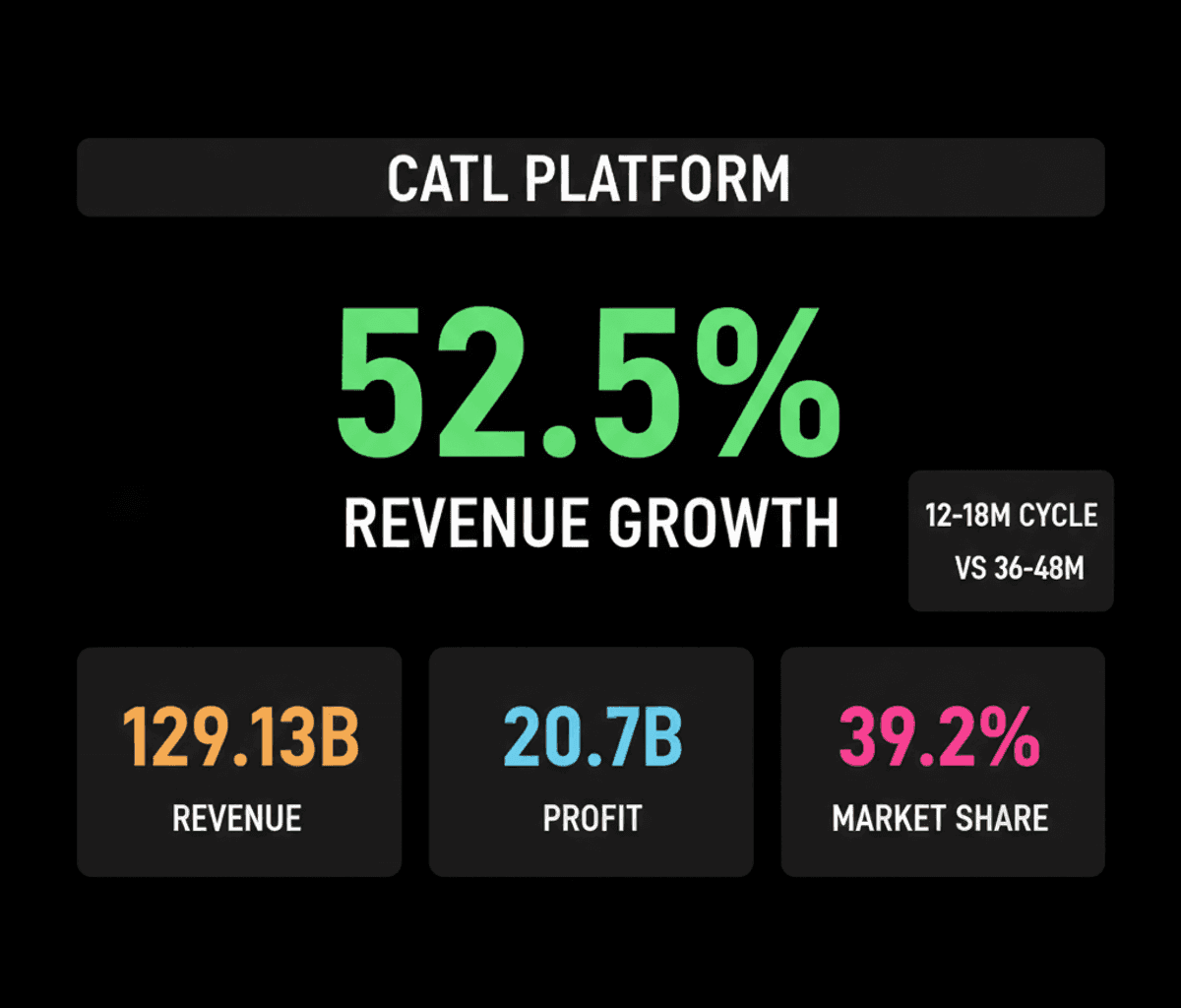

The financial indicators from the first quarter of 2026 underscore this shift in power dynamics. CATL reported a revenue of RMB 129.13 billion (US$17.9 billion), marking a substantial 52.5% year-on-year increase. Its net profit surged by an impressive 48.5% to RMB 20.7 billion (US$3.03 billion). Notably, CATL’s single-quarter net profit surpassed the combined profits of seven major Chinese automakers, a stark illustration that the locus of value creation is migrating towards core technology providers rather than solely residing with final vehicle assemblers.

The Platform Architecture Redefining Automotive Development

Central to CATL’s platform strategy is its automotive technology subsidiary, CAIT, which has introduced the CATL Integrated Intelligent Chassis (CIIC) platform. This offering includes distinct chassis concepts such as “Bedrock” and “Panshi.” These platforms provide automakers with a pre-engineered “lower vehicle half,” integrating structural battery components, suspension systems, crash safety features, thermal management, and sophisticated electrical architectures. By leveraging these foundational elements, carmakers can drastically reduce their development cycles from a traditional 36-48 months to a mere 12-18 months.

The strategic advantage of this platform approach is exemplified by the “Neta Lesson.” When a particular vehicle brand faced financial distress, the underlying CATL platform remained intrinsically valuable and licensable to other manufacturers. This mirrors the resilience of the Android platform, which continued to thrive and be adopted by new device makers even as individual smartphone brands faded. It highlights the enduring value of controlling the underlying technology architecture over the transient fortunes of specific product brands.

CATL’s commanding market position further solidifies its platform thesis. In 2025, the company held a dominant 39.2% global EV battery market share and a significant 30.4% share in the global energy storage battery market. During the same year, CATL sold an impressive 661 GWh of batteries, operating with a production capacity of 772 GWh. This scale not only confers significant cost advantages but also establishes a formidable barrier to entry for potential competitors, reinforcing its structural moat.

The company’s diversification into energy storage, lithium mining, and commercial vehicle electrification further contributes to its exceptional profitability. This multi-faceted approach allows CATL to maintain robust financial performance, even amidst intense price wars among EV manufacturers. By controlling critical inputs and expanding into adjacent high-growth sectors, CATL insulates itself from the commoditization pressures impacting vehicle assembly.

The core insight here is that the automotive industry is undergoing a fundamental re-architecture. Just as in the smartphone market, where the operating system and app ecosystem became the primary drivers of long-term value and competitive advantage, the EV sector is demonstrating a similar pattern. Future competitiveness will increasingly depend on controlling foundational technologies such as battery chemistry, advanced software, and integrated vehicle platforms, rather than simply excelling at vehicle production and branding.

This structural shift implies a future where the value proposition of a carmaker might increasingly be defined by its ability to integrate and differentiate on top of robust, standardized, and technologically advanced platforms. The entities that control these foundational layers, like CATL, are poised to capture a disproportionate share of the industry’s profits and exert significant influence over its strategic direction, fundamentally reshaping the competitive landscape of the global automotive sector.